By Lana Yoshii

There are 80 proposed hotels and 5 expansions totaling roughly 12,000 rooms planned for development in the greater Silicon Valley area. Worse case, with 31,000 hotel rooms today, there could conceivably be a 39% increase in supply. Is it time to hit the panic button?

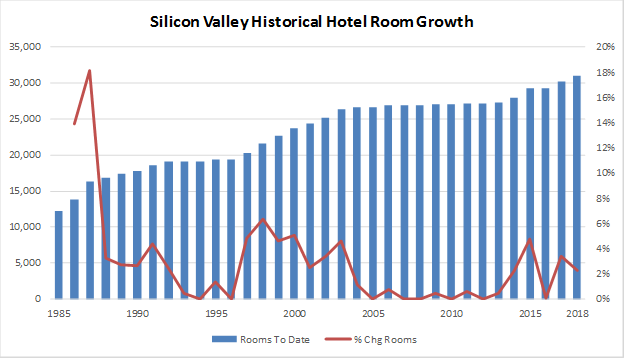

Since 2000, the two largest surges of new supply occurred in 2003 (4.6% growth) and 2015 (4.8% growth). However, from 2004 to 2014, Silicon Valley’s new hotel rooms supply was very mild – maxing out at a 2.3% annual growth in 2014, and averaging at a compound annual growth rate of 0.5%. In recent history, annual new supply exceeded 1,000 new rooms in 2015 and 2017. In 2018, 4 hotels (697 rooms) opened. The chart below illustrates the historical growth of hotel rooms in Silicon Valley (based on rooms available on December 31 of each year).

Source: STR, Pinnacle Advisory Group

The wildest ride was demand-driven: in 1985, demand grew by 15%, fell off to 13% in 1986, and then spiked again in 1987, growing by nearly 19%. The wild swings in demand were to the activity in the semi-conductor industry.

But the Silicon Valley isn’t selling chips any more, or any other tangible product. It is selling an ingredient that is critical to virtually every manufactured product, the process that produces it, or the marketing of it. The past 10 years are the most relevant.

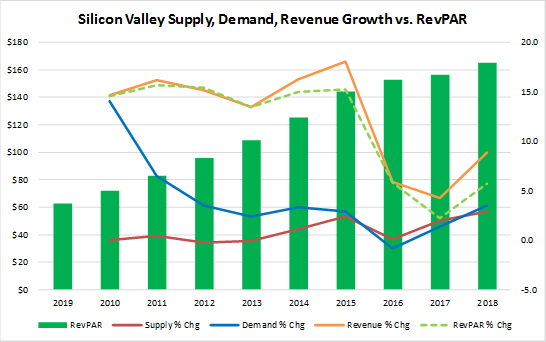

Between 2009 and 2018, demand growth had exceeded supply growth for 8 of the 10 years. After slipping in 2016 and 2017, demand growth steamed ahead again, quite possibly because the city engineering offices can’t issue building permits in a timely manner. Regardless, RevPAR growth has not fallen below 2.2%.

Source: STR

Silicon Valley’s employment has shown signs of maturing, but not declining. Office space continues to be absorbed at a healthy pace. Silicon Valley’s unemployment rate remains lower than the national average. The fundamentals are excellent. Recent new supply has been growing at a similar rate as demand growth, which has bled off some of the market’s ADR compression. Only a portion of the proposed hotels will get financed. Increasing construction costs are causing many of the projects to stall out. Although projected new supply may increase at a faster pace, this market is likely to remain relatively healthy for the next few years. ADRs are expected to grow moderately – at single digit rates – rather than the double digit growth rates when midweek demand met up with capacity constraints in Silicon Valley.

Details on the Current Pipeline

Of the proposed 12,000 new hotels rooms in various stages of development, there are 20 hotel projects with 3,300 rooms currently under construction. When the last of these opens over the next 2 to 2.5 years, Silicon Valley’s hotel rooms supply will have increased by a cumulative 11%.

Currently, there are approximately 3,800 rooms entitled for development. Should these entitled rooms also open, hotel rooms supply will increase by a cumulative 23%. However, with so much competing office and residential development, contractors and sub-contractors are scarce. Assuming financing were in place, the delays in pulling permits, inspections and sub-contractor scheduling inefficiencies would push the first opening dates of these rooms into 2022.

If the balance of all of the rooms under construction and entitled rooms come to fruition by the end of 2022, those 7,000 rooms would result in a 5.3% compound annual growth rate from 2018 to 2022. If all rooms under construction, entitled rooms and unentitled rooms open by 2025, these 12,000 new rooms would result in a 4.8% compound annual growth rate.

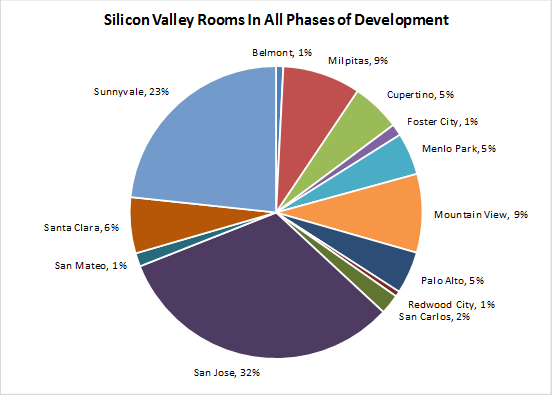

Market imbalances are a local issue. So where will these 12,000 rooms be located? San Jose leads the pack with 32% of the proposed hotel rooms in all phases of Silicon Valley development (e.g., under construction, final planning, preliminary planning, speculative). Sunnyvale follows with 23%, then Mountain View and Milpitas with 9% each. The following chart illustrates the distribution of Silicon Valley rooms in all phases of development.

Source: STR, Pinnacle Advisory Group

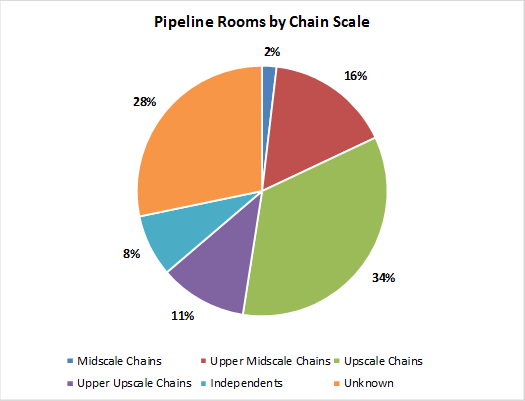

Although there are numerous projects that have yet to be affiliated with a brand, the vast majority of rooms in the pipeline are in the STR-defined Upscale Chain, which includes brands such as Courtyard, Hilton Garden Inn, Hyatt House, Residence Inn, Cambria, Hyatt Place, Homewood Suites and AC Hotels by Marriott. At this time, any luxury-positioned hotels in development are slated to be independent hotels, or have not yet obtained franchise approval.

Source: STR, Pinnacle Advisory Group

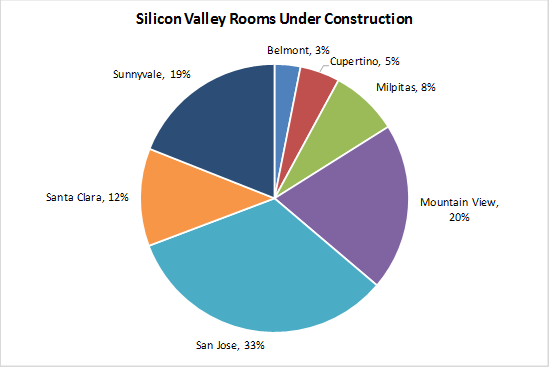

The process of getting entitlements and financing can result in proposed projects never coming to fruition. Therefore, we identified the 20 projects current under construction, by city. San Jose has the most rooms under construction (33%), followed by Mountain View (20%) and Sunnyvale (19%). Interestingly, Santa Clara has 6% of the rooms in all phases of development, but 12% of the rooms currently under construction.

Source: STR, Pinnacle Advisory Group

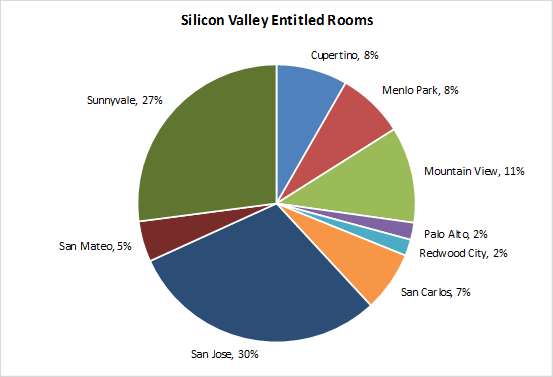

We also confirmed that 26 of the planned projects (new hotels and room additions) totaling 3,779 rooms have obtained entitlements; however, may not have secured financing. The largest blocks of entitled rooms are in San Jose with 1,136 entitled rooms (30%), Sunnyvale with 1,023 entitled rooms (27%), and Mountain View with 423 entitled rooms (11%).

Source: STR, Pinnacle Advisory Group