by Daniel Lesser

NEW YORK CITY—To the surprise of many, the US lodging industry closed out 2016 with operating metrics still at record setting levels; however, its growth trajectory was notably lower when compared to years past. In general, occupancy levels have peaked and any short term RevPAR growth will be driven by increases to ADR. New supply of hotel rooms will continue to occur primarily in the Upper Midscale and Upscale chain scales. Of the nation’s top 25 markets, New York, Seattle, and Denver are experiencing double digit increases of new rooms under construction while eight other markets are currently slated for increases of five to eight percent of existing room supply.

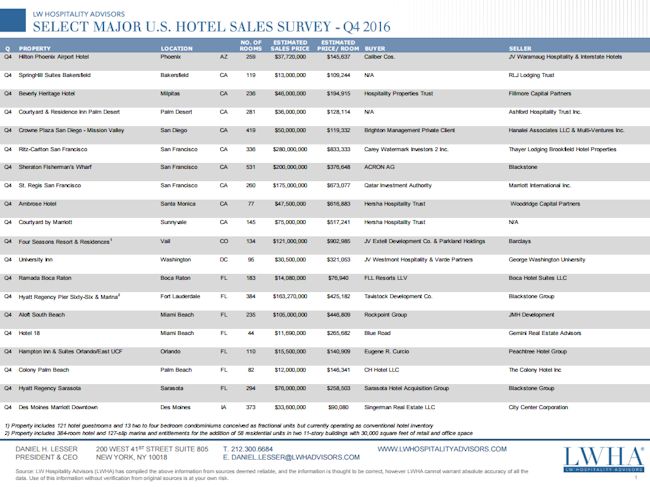

The LW Hospitality Advisors (LWHA) 2016 Major US Hotel Sales Survey includes 173 single asset sale transactions over $10 million, none of which are part of a portfolio. These transactions totaled roughly $12.7 billion, and included approximately 42,400 hotel rooms with an average sale price per room of $300,000. By comparison, the LWHA 2015 Major US Hotel Sales Survey identified 200 transactions totaling roughly $14.0 billion including 53,000 hotel rooms with an average sale price per room of nearly $265,000. Comparing 2016 with 2015, the number of trades decreased by 14 percent while total dollar volume declined roughly 9 percent and sales price per room increased by 13 percent.

Interesting observations from the LWHA 2016 Major US Hotel Sales Survey include:

- 30 major sales occurred in the State of Florida followed by 26 in California, and 23 in New York;

- Within major US metropolitan areas, New York had the most major hotel sales with 23, followed by 12 in Washington DC, 9 in Seattle, 8 in Miami, 7 in San Francisco, and 6 each Chicago, Los Angeles, and Phoenix;

- 37 single asset trades greater than $100 million occurred during 2016 and of those 6 were greater than $300 million;

- The sheer size of the largest single asset trade of 2016, namely $780 million paid for the 1,230 room Hyatt Regency Waikiki Beach Resort & Spa in Honolulu, HI is noteworthy;

- Four single asset trades greater than one million dollars per room transacted during 2016;

- The $65 million sale of the 49 room Capella Hotel in Washington DC has by far set a new price per room record of roughly $1.3 million per key in the nation’s capital.

- Additional new high water mark per room sale prices were set with the following respective trades: $697,000 per key for the 462 room LondonHouse in Chicago, $945,000 per room for the Mandarin Oriental in Boston, and $695,000 per room for the Hotel 1000 in Seattle, WA.

To the surprise of many, but in line with expectations of many more (at least from an electoral college perspective) it seems the theme that put President Obama into the White House in 2008 is now pinned onto President Trump and a Republican majority in the House and Senate. The idea of change from gridlock and the prospect of direction for what have been listless and wandering investment markets are now expected to come forth under the new administration. The change factor comes from a single party controlling two branches of government, thus creating the possibility that the interminable gridlock may finally be coming to a close.

After much anticipation, during mid December the US central bank finally increased its federal funds rate by 25 bps. This event represents the second rate hike in more than a decade coming amid near full employment, rising inflation expectations, and strong economic growth. At the beginning of 2016, the Federal Reserve’s plans for “normalization” of interest rates fell off track due to meager US economic growth combined with fears of financial turbulence in China. Furthermore, Britain’s shock vote to exit the European Union in June dissuaded the Fed from raising rates. During the second half of this year, increasingly positive US economic metrics has helped sway reluctant policymakers towards raising rates. Concerns that a rate increase would interrupt a fledgling recovery amid directionless inflation and slack labor markets were overcome. President Trump has proffered an economic policy which will include a major tax cut for businesses, an infrastructure spending program, and deregulation all of which contributes to the recent specter of near term accelerating inflation coupled with additional increases in the fed interest rate.

Given current US economic expectations, many, particularly foreign investors believe the coming year will be a terrific time to deploy capital into transient lodging real estate assets that mark rents (average room rates) to market more often than buildings encumbered with long term credit worthy tenancies. During the late 1970s and early 80s when the US was experiencing double digit annual inflation growth, hotel assets were much better positioned to adjust rents compared with a 100 percent occupied office building with 10 to 20 year tenancies of government agencies. Clearly hotel operating expenses will rise during any inflationary environment; however, continuous repricing of room nights should allow for revenues to, at a minimum, keep pace and in many situations, exceed such increases.

Negative pressures on the lodging sector include a strong US dollar which makes it expensive for foreigners to visit America. Furthermore even with a late year rally, availability of CMBS hotel financing was well off the pace of 2015. The good news is that alternative sources of debt financing have been available from banks, life companies, and private debt funds. At this juncture many lodging markets across the country have reached peak occupancy levels during 2015 and 2016, and should now be poised for operators to aggressively increase average daily rates. Barring a black swan event, a controlled landing for the industry is more likely than a crash.

Daniel H. Lesser is president and CEO of LW Hospitality Advisors LLC. The views expressed here are the author’s own.

_______________

This article originally appeared on GlobeSt.com and is reprinted with permission of the author.