By Lorenzo Gullotta, Giammarco Pignocchi, Ezio Poinelli

The resurgence of travel activity in Venice following the years afflicted by the COVID-19 pandemic has not only been a sign of recovery but also an indicator of evolving trends within the city’s tourism sector. In line with what was observed in other Italian cities, Venice’s hotel market experienced an unprecedented surge in the post-pandemic era. While overall occupancy rates remain below pre-pandemic levels, the upper upscale and luxury market segments appear to have fully rebounded. This recovery, along with a significant increase in average rates, has resulted in a notably positive impact on Revenue Per Available Room (RevPAR).

Meanwhile, the vacation homes market, which was already gaining momentum before 2020, has accelerated further in the aftermath of the pandemic a trend driven by a combination of shifting traveller preferences and the rising prices of hotels, making them less accessible to certain traveller demographics.

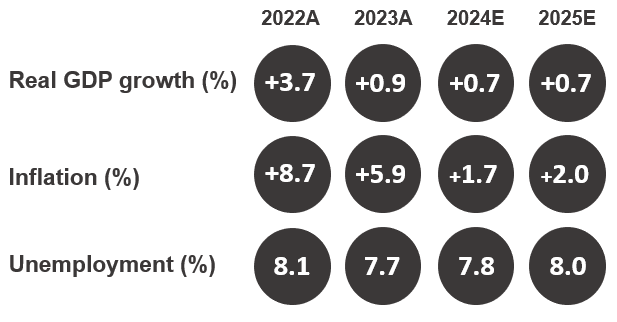

Economic Indicators – Italy

Source: International Monetary Fund, April 2024

Airport Statistics

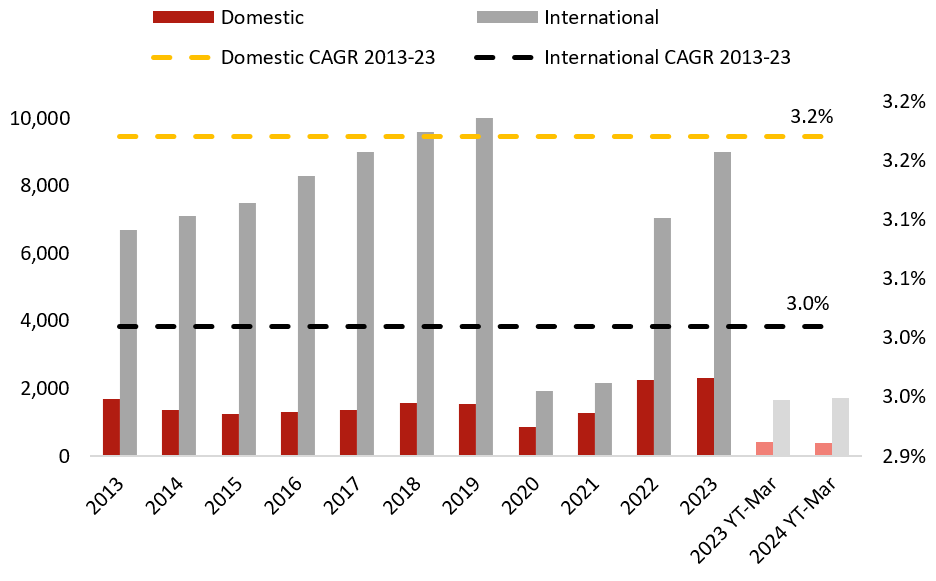

Passenger movement at Venice Marco Polo Airport reached 11.3 million in 2023, down by 2.1% compared to 2019. International passengers were 10% lower than pre-pandemic volumes, while domestic passengers increased by nearly 50% from 2019 figures. During the first quarter of 2024, there was a 2.8% uptick in overall volumes, with the international segment experiencing a 4.2% year-on-year growth and the domestic segment witnessing a 3.1% decline. Meanwhile, Treviso Airport Antonio Canova in 2023 was still 6.7% lower in passenger volumes compared to 2019. Despite a notable increase of 30.9% in the international segment, the domestic segment dropped by 80.7%. The beginning of 2024 was marked by a closure between February 25 and March 16.

Nevertheless, total passenger volumes in Q1 2024 aligned with the previous year, with international passengers increasing by 15%, while domestic passengers dropped by 90.5%.

Source: Assaeroporti

Tourism Demand

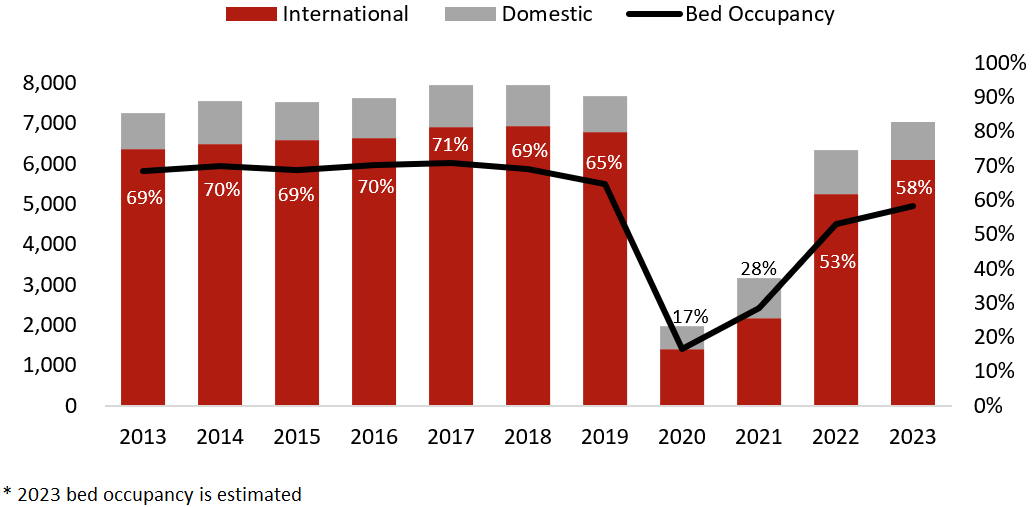

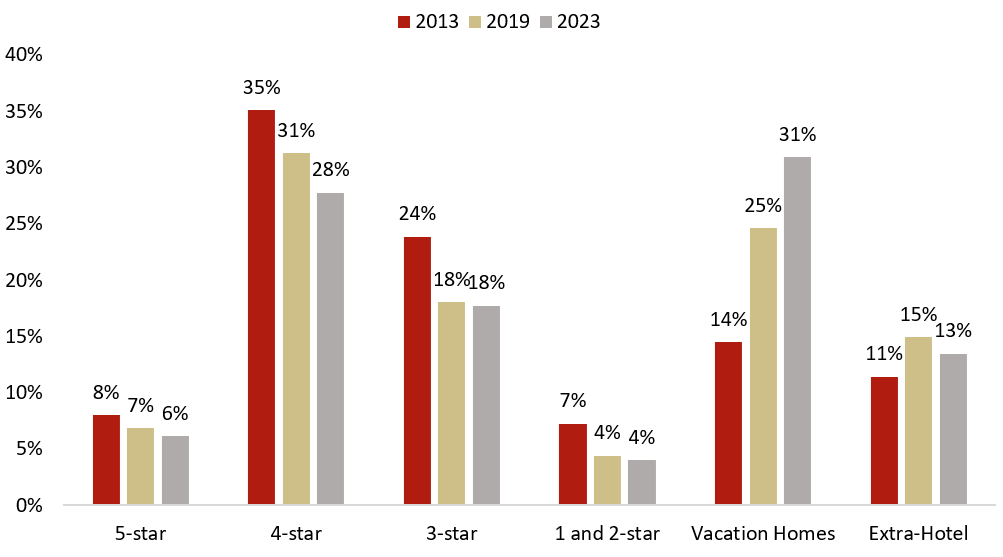

In 2023, accommodated bednights in the Venice market nearly caught up to 2019 figures (-2.5%). However, the hotel sector remains evidently impacted by the aftermath of the COVID-19 pandemic, as it still lags by 10.3% compared to 2019. Conversely, extra-hotel accommodations, including B&Bs, guesthouses, vacation homes, and hostels, have experienced a tremendous surge in demand in the wake of the pandemic. By the end of 2023, bednights in these categories had increased by 9.5% compared to 2019, with vacation homes emerging as the primary driver of this trend. Over the past decade, in fact, Venice has witnessed a significant increase in short-term rental accommodations, with vacation homes showcasing double-digit CAGR from 2013 to 2023 (+11%). Consequently, their market share rose from 14% in 2013 to 25% in 2019 and further to 31% in 2023, indicating an acceleration of this trend.

In terms of geographical distribution, the Centre/Lagoon area remains the most sought-after, capturing approximately 72% of all accommodated bednights, followed by Mestre/Inland with 25%, and Lido with 3%. While the Centre/Lagoon area has successfully recovered to 2019 bednights volumes (+3.1%), Mestre/Inland and Lido di Venezia continue to lag significantly, standing at -14.1% and -17.2% respectively. Notably, Lido seems to have experienced a substantial decline in demand across all categories, with accommodated bednights decreasing by over 30% over the past decade. This negative trend, therefore, started well before the pandemic.

Accommodated Hotel Bednights and Gross Bed Occupancy (000s)

Source: HVS elaboration of Regione Veneto and ISTAT data

Share of Bednights by Type of Accommodation

Source: HVS elaboration of Regione Veneto and ISTAT data

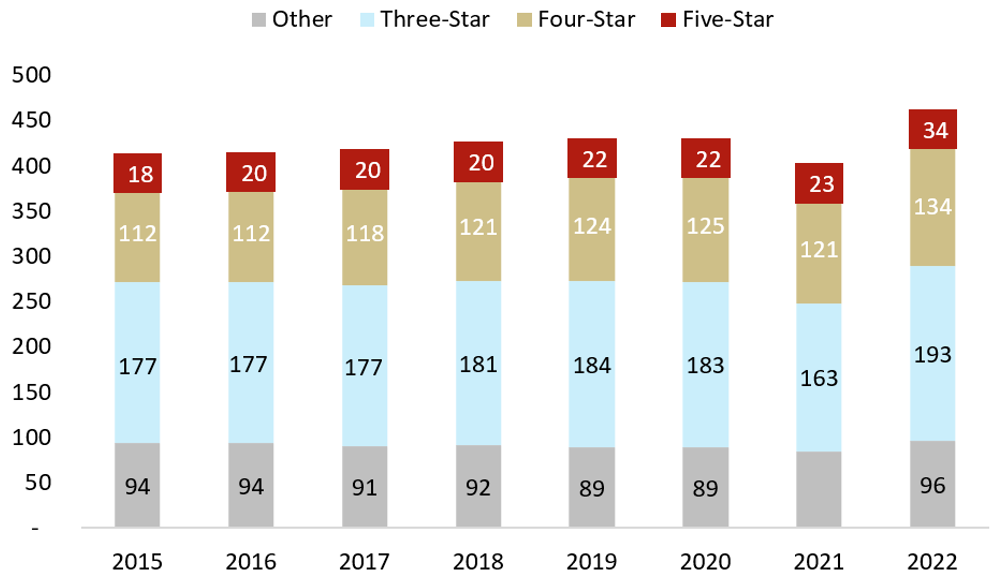

Hotel Supply and Pipeline

Between 2015 and 2022, the number of hotels increased from 401 to 457, accompanied by a rise in rooms from 15,808 to 16,988. It’s worth noting that the methodology for counting establishments in the Veneto region changed in 2022, contributing to the substantial growth observed that year. During the period from 2015 to 2019, the five-star hotel segment experienced the most rapid expansion in terms of the number of hotels, with a Compound Annual Growth Rate (CAGR) of +5.1%, while the three-star segment saw the fastest growth in terms of rooms, with a CAGR of +3.1%. Conversely, the “other” hotel segment witnessed a decline in both the number of establishments and rooms. Five-star hotels boasted the largest average room count, with 74 rooms in 2022, compared to 58 rooms for four-star hotels, 26 rooms for three-star hotels, and 16 rooms for other establishments.

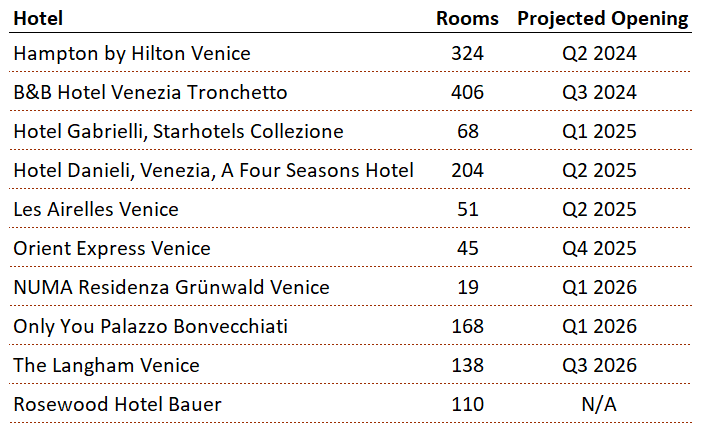

We identified an interesting pipeline primarily concentrated in the Venice Centre/Lagoon area, comprising approximately 1,500 rooms, representing around 9% of the existing supply. This pipeline comprises only hotels in the five-star (7 hotels, 784 rooms) and in the three-star (3 hotels, 749 rooms) segments. The Hampton by Hilton and the B&B Hotel are both greenfield constructions being developed in the Tronchetto area, while the other projects stem from the renovation and/or conversion of existing assets. More in detail, the Hotel Gabrielli will be managed by Starhotels after renovation, the historical Hotel Danieli is expected to fly the Four Seasons flag and Palazzo Donà Giovanelli is being transformed into Orient Express Venice (Accor). Les Airelles should result from the renovation of the ex-Bauer assets in Giudecca (Hotel Palladio and Villa F). Similarly, the NUMA Residenza Grunwald Venice should take shape through the renovation of the old Bauer Casanova, adjacent to the Bauer Hotel.

Only You Bonvecchiati, a brand under the Palladium Hotel Group, is anticipated to emerge from the fusion and refurbishment of the Hotel Bonvecchiati and the Palace Bonvecchiati. Hong Kong-based Langham Hospitality Group instead is in the process of converting an ex-glass factory on the island of Murano into an ultra-luxury hotel. Lastly, the Hotel Bauer Palazzo was slated to operate under the Rosewood brand after extensive renovation work. Following the crisis involving Signa, the former owner of the asset, the project appears to be on hold as the new owner has yet to be determined.

Hotel Operating Performance

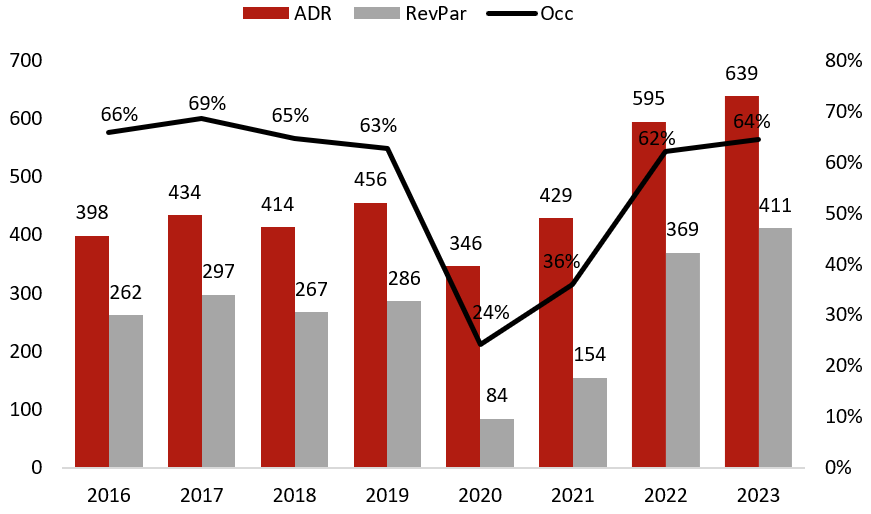

We conducted an analysis of approximately 2,300 rooms spanning the period 2016-23, all positioned within the upper-upscale and luxury segments and located in the Centre/Lagoon area. The data indicate that occupancy rates in 2023 have returned to pre-pandemic levels, while the Average Daily Rates (ADRs), in line with what was observed in other Italian and European cities, experienced a substantial increase in 2022 and 2023. Consequently, both ADR and Revenue Per Available Room (RevPAR) experienced an increase of over 40% over 2019. It must be noted that occupancy rates of hotels in the upper-upscale / low five-star segments hover around 75% and that the reported figure is impacted by ultra-luxury properties and by some large hotels that operate seasonally.

Hotel Investment Market

We have identified 18 transactions between 2019 and 2022 in Venice. In 2023, we are not aware of any significant hotel transaction taking place. The most significant transaction was the sale in 2019 of the Bauer portfolio: four assets and 290 keys for an estimated price of €400 million. The Bauer Palazzo was then resold to Signa in 2020 for a reported €250 million. Signa then filed for insolvency in late 2023. At the time of this article, Signa creditors are in a struggle to determine the new owner of the prestigious asset.

Other important transactions involved the Bonvecchiati Complex, the Hotel Baglioni Luna and the Hotel Excelsior Venice Lido, all sold for an estimated €100 million.

Outlook

Venice has always been a market of strong hotel performance. However, rather than stimulating innovation and investment, this stability has inadvertently hindered the hotel market. In recent years, there have been a few notable hotel transactions contributing to Venice being perceived as one of the markets with the highest barriers to entry in Italy. The city is characterized by a significant number of aging properties across all categories.

Looking forward, there is considerable investor and brand interest in Venice, particularly following the upturn in hotel performance over the past two years. However, greenfield projects are exceptionally rare due to the limited availability of land, and the conversion of existing buildings presents significant challenges, particularly of a bureaucratic nature. Therefore, with a scarcity of available properties for sale, many investors (and brands) find themselves unable to enter the market.

In the luxury segment there is some activity being observed, with seven projects in the pipeline totaling 784 rooms. Of these, 620 stem from the renovation and rebranding of existing hotel assets, and only 183 come from the conversion of non-hotel assets, of which 138 are in Murano (The Langham Venice). So, more than a proper pipeline of new hotels coming in, what is being observed is mostly the upward repositioning of existing assets where the spread between actual and potential performance created room for negotiation. Hotels in the lower segments, instead, tend to be small in size on average, which makes them less appealing to both brands and investors. Therefore, with the exception of the upcoming Hampton and B&B Hotels bringing new, modern inventory in the segment, the market in these categories is expected to remain largely unbranded, especially in the centre. Additionally, many of these hotels, predominantly family-run establishments, lack the resources and innovation capabilities to renovate their properties and enhance their offerings and are therefore expected to suffer the most from the competition with vacation homes in the future. However, there may be some transaction activity involving these assets in the future, driven by refinancing needs, generational transitions or the potential for achieving better performances by affiliating with more flexible “collection brands”. This could potentially catalyse the development of an intriguing boutique hotel scene in Venice.

Finally, it’s worth mentioning that there are some interesting projects in the feasibility and design stages on Murano Island. These projects (mostly) involve the potential conversion of disused glass factories, similar to what is being done with The Langham Venice, and are currently under evaluation.