November 11, 2021 — Profitability has improved across much of the globe as the hotel industry continues its slow recovery. In measuring that recovery, 2019 data is the benchmark, and by indexing with pre-pandemic levels, hoteliers can gain key context for the amount of profitability they are recapturing.

Building on its initial launch in the U.S., STR now features monthly P&L data reporting in Europe, the Middle East, Asia Pacific, and the full Americas region.

In our latest P&L press release focused on the Asia Pacific region, we noted that profitability in the region’s hotel markets was well below pre-pandemic levels as of September 2021. In this latest update, we expand to a global perspective to check in on Europe, the Middle East & Africa, and South America.

Global comparison

In the Middle East & Africa, gross operating profit per available room (GOPPAR) was 68% of September 2019 levels at US$30.04.

South America (US$5.73) came in at 57% using the same time comparison, while Europe GOPPAR was US$57.87 (60% of its 20219 levels).

Much further down the line, Asia Pacific (US$13.21) GOPPAR was just 35% of September 2019 levels, even with improvement after the world’s worst profitability decline in August.

While looking at specific markets from each region, the Maldives, Qatar, Moscow, and Shanghai recovered better than 80% of 2019 GOPPAR levels.

On the other side of the spectrum, five of 27 key international markets still realized negative profit levels in comparison with September 2019: Bangkok (-31%), Bali (-24%), Kuala Lumpur (-21%), Hong Kong (-9%) and Tokyo (-4%).

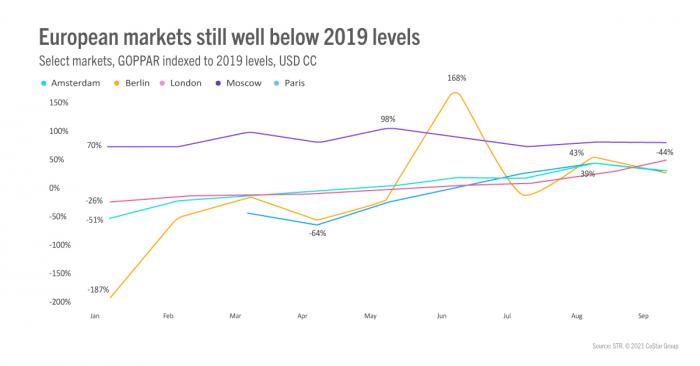

Europe on its way to recovery

Although the summer months in Europe could have not reached the highest expectations, there was substantial improvement from the same time last year. September showed a GOPPAR dip for most of Europe’s top markets after summer highs.

Moscow, which had reached as high as 98% of its comparable 2019 level back in May, led the major European markets with September 2021 GOPPAR of US$36.30 (70% of 2019 comparable). Berlin, which had been at -12% of its 2019 GOPPAR in July returned to a positive level of US$7.79 in September. London showed slow and steady improvement over the summer months but remained at 44% of 2019 GOPPAR in September at US$6.43.

Strong September for top Middle East markets

After weak summer months, key Middle East and markets reported profitability improvements during a strong September.

Dubai GOPPAR of US$158.68 was 153% of September 2019 levels. Qatar (US$148.64) came in at 89% using the same time comparison, while Saudi Arabia’s GOPPAR level was US$103.78 (33% of its 2019 levels).

Asia Pacific profitability well below pre-pandemic levels

Beijing’s GOPPAR of US$29.91 was 70% of September 2019 levels. Singapore (US$39.99) came in at 35% using the same time comparison, while Hong Kong (US$6.22) was at just 10%. Sydney, Bali, Bangkok and Tokyo were all in negative GOPPAR territory—Tokyo has seen the biggest profitability decline over the past several months.

Slow, steady improvement in South America

Top South American markets are trending upward in hotel profitability.

Lima, which had fallen to as low as -13% of its comparable 2019 level back in February, led the major South American markets with GOPPAR of US$25.41 (16% of 2019 comparable). Bogota, which had been at 30% of its 2019 GOPPAR in April, returned to a positive level of US$49.75 in September. Rio de Janeiro has shown slow and steady improvement since June but remained at just 75% of 2019 GOPPAR in September at US$63.92.

Industry stakeholders interested in Monthly P&L participation should contact [email protected].