Analysis by Isaac Collazo, Chris Klauda, Will Anns

Countries (markets) mentioned:

- United States (Baltimore, Daytona Beach, Denver, Fort Lauderdale, Fort Myers, Las Vegas, Miami, Minneapolis, Oahu, Orlando, Phoenix, San Antonio, Sacramento, St. Louis, Tampa and Tucson).

- Germany (Cologne and Frankfurt), Indonesia, Singapore

Highlights

- U.S. ADR down for the first time this year, RevPAR a third time.

- Groups still driving high-end U.S. hotels.

- Germany sees strong, group-induced RevPAR gains.

- Singapore loves Taylor Swift.

- 2024 solar eclipse demand to top 2017 event.

U.S. Performance

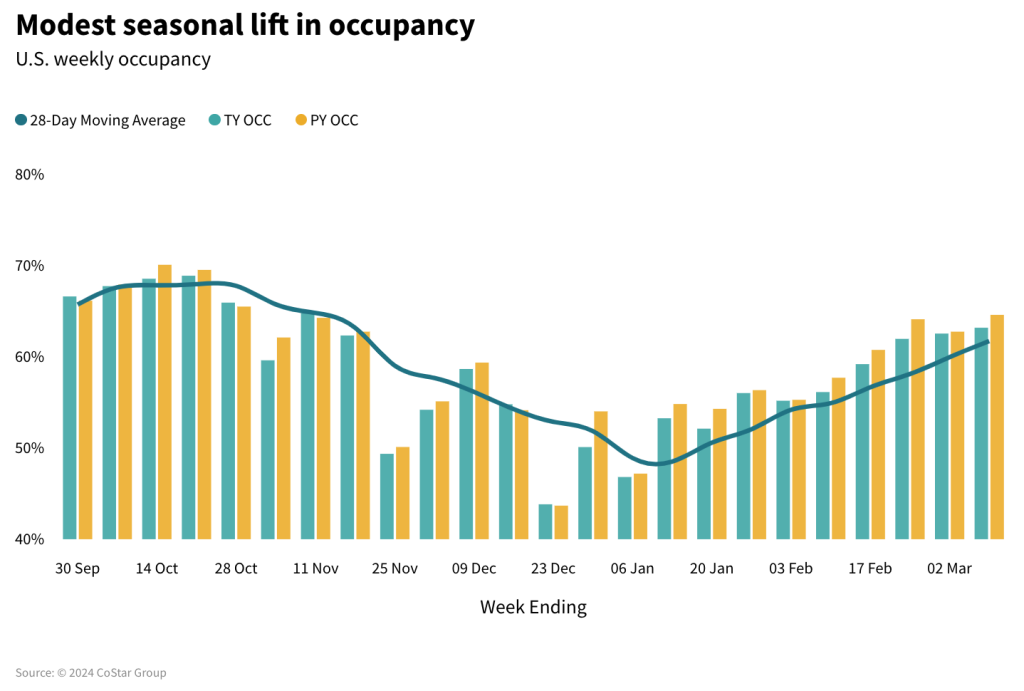

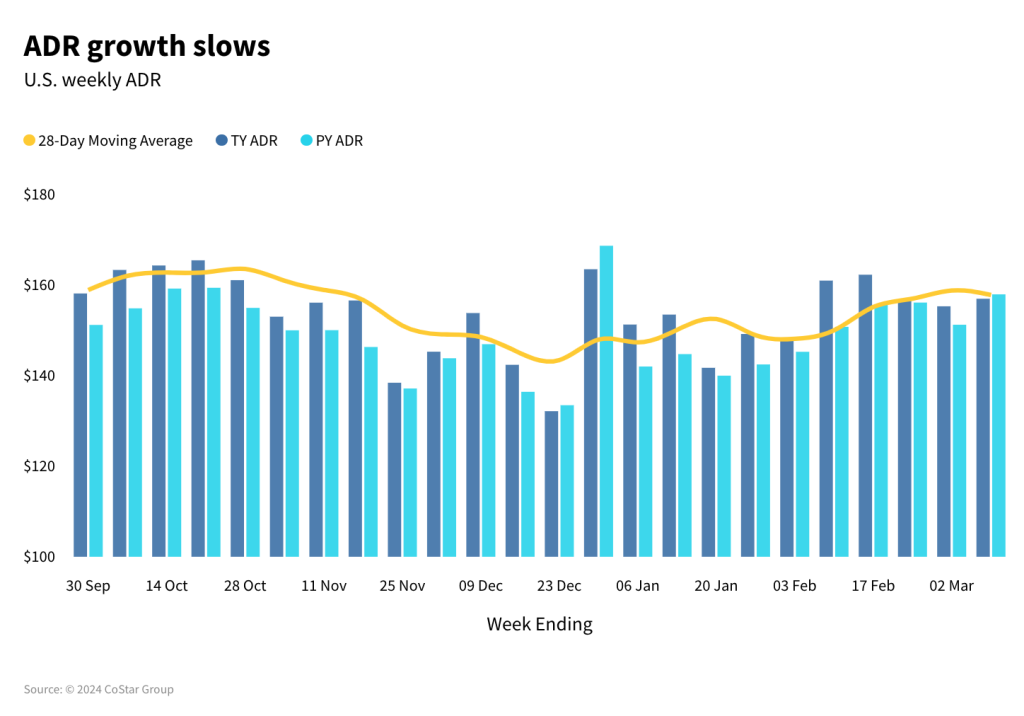

U.S. hotels continued to see week-on-week growth as the spring season blossoms, however, year-over-year growth stalled with revenue per available room (RevPAR) falling 2.8% via decreasing occupancy (-1.4ppts). Economy class hotels contributed the most to the gross demand loss (58%) with Midscale and Upper Midscale class hotels also contributing. Upper-tier hotels (Luxury, Upper Upscale and Upscale) continued to see growth, but their collective gain was insufficient to offset the losses in lower-tier hotels. Average daily rate (ADR) was also down (-0.6% YoY), representing the first YoY decrease in the metric since the last week of 2023.

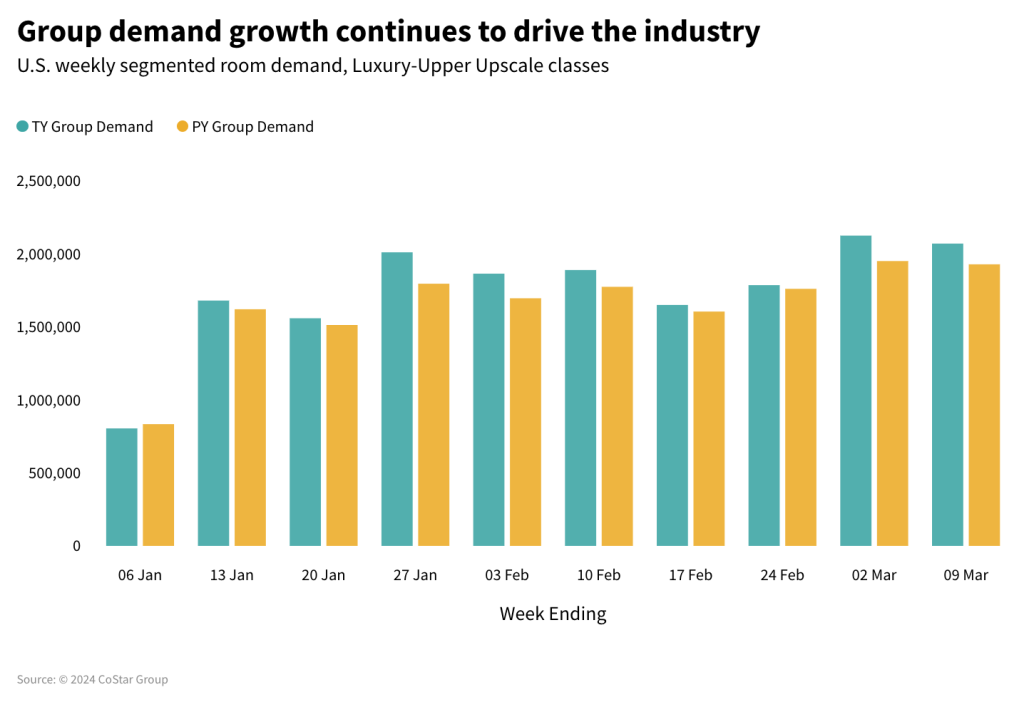

As seen over the past several weeks, Las Vegas continued to play a pivotal role in the industry’s performance. RevPAR in Las Vegas was down 30.6% YoY due to a convention calendar shift. Even with the shift, group demand in Las Vegas among Luxury and Upper Upscale class hotels was up versus a year ago. The nation also saw group demand increase for a 10th consecutive week.

Day-of-Week Movement

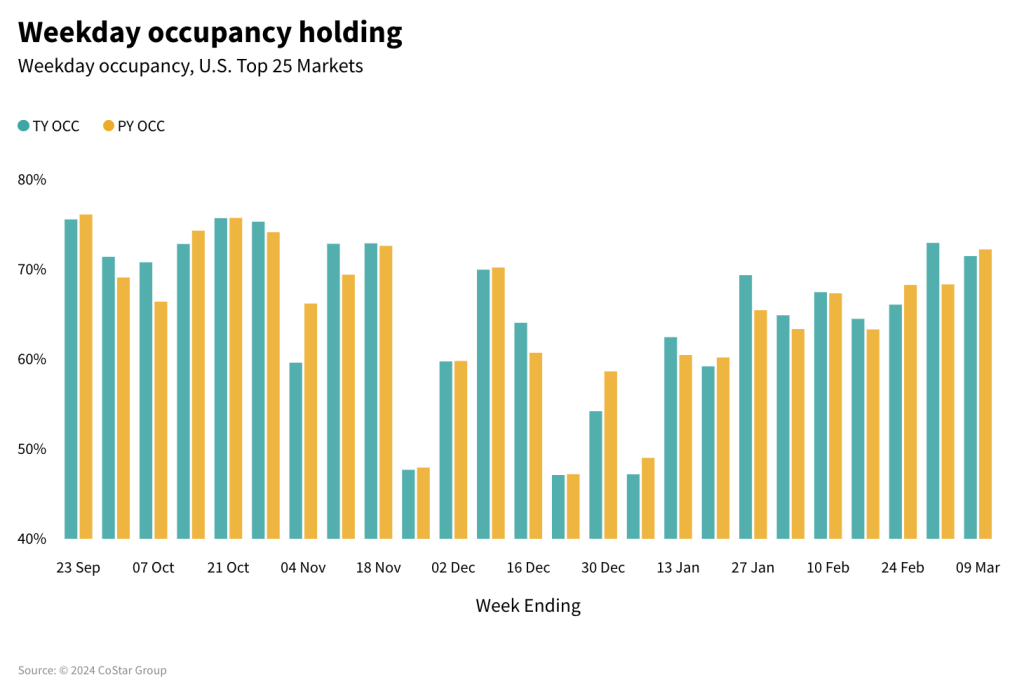

While RevPAR in Las Vegas fell every day, that wasn’t the case nationwide. Excluding Las Vegas, the relatively stronger weekday (Monday-Wednesday) performance seen over the past year continued as weekday RevPAR was flat (-0.2% YoY) with an occupancy decline of 0.5ppts offset by a 1% ADR gain. Weekends (Friday & Saturday) showed the worse decrease with RevPAR dropping 2.7%, driven mostly by declining occupancy (-1.5ppts). Shoulder days (Sunday and Thursday) also produced a RevPAR decline, down 1.8% and driven entirely by falling occupancy.

Market-Level Leaders

Nine of the Top 25 Markets saw RevPAR gains with Minneapolis posting the nation’s largest growth (+45.1% YoY) as it hosted the Big Ten Women’s Basketball Tournament. St. Louis and Washington, D.C. also saw double-digit RevPAR growth. Across the next 25 largest markets, Baltimore, San Antonio, Sacramento, and San Jose had great weeks with RevPAR up 10%+ YoY, lifted by both ADR and occupancy gains. Phoenix had the nation’s highest occupancy (85.6%) followed by eight Florida markets where occupancy ranged from 81.6% in Fort Myers to 84.1% in Fort Lauderdale. Tucson and Oahu also reported occupancy above 80% for the week. Weekend occupancy surpassed 90% in Daytona Beach, Miami, Orlando, Phoenix, and Tampa.

Group Driving Industry Performance

For the 10th consecutive week, group demand (among Luxury and Upper Upscale hotels) increased, rising 7.4% YoY. Group demand was just one percent below 2019. Group ADR, which had shown healthy growth (5%+) over the past four weeks, declined slightly (-0.8%). Nearly all the growth (75%) in group demand occurred in the Top 25 Markets with both the Top 25 and the rest of the country seeing slight ADR declines. Twelve of the Top 25 Markets posted group occupancy gains above the average with Minneapolis, St. Louis, and Denver topping the list.

All Classes Slow

All six hotels classes saw RevPAR fall with the largest decline in Economy (-10.5%) and the smallest in Upper Upscale (-1%). ADR drove the decrease in the top two classes while occupancy played a greater role in the decrease across the next four classes. Over the fortnight, room demand has grown in Luxury, Upper Upscale and Upscale with Upper Upscale claiming nearly half of the gross increase, which we believe has been driven by gains in groups and conference business. We continue to investigate the declines in Midscale and Economy seen over the past three quarters. It seems that the tier is being impacted by multiple factors, including hotel closures, economic pressures on budget travelers, and a change in traveler composition. The recent softness in Upper Midscale is also a concern. Some have hypothesized that all of this is a market correction with more traditional demand patterns and growth returning in the summer.

Germany Stands Out

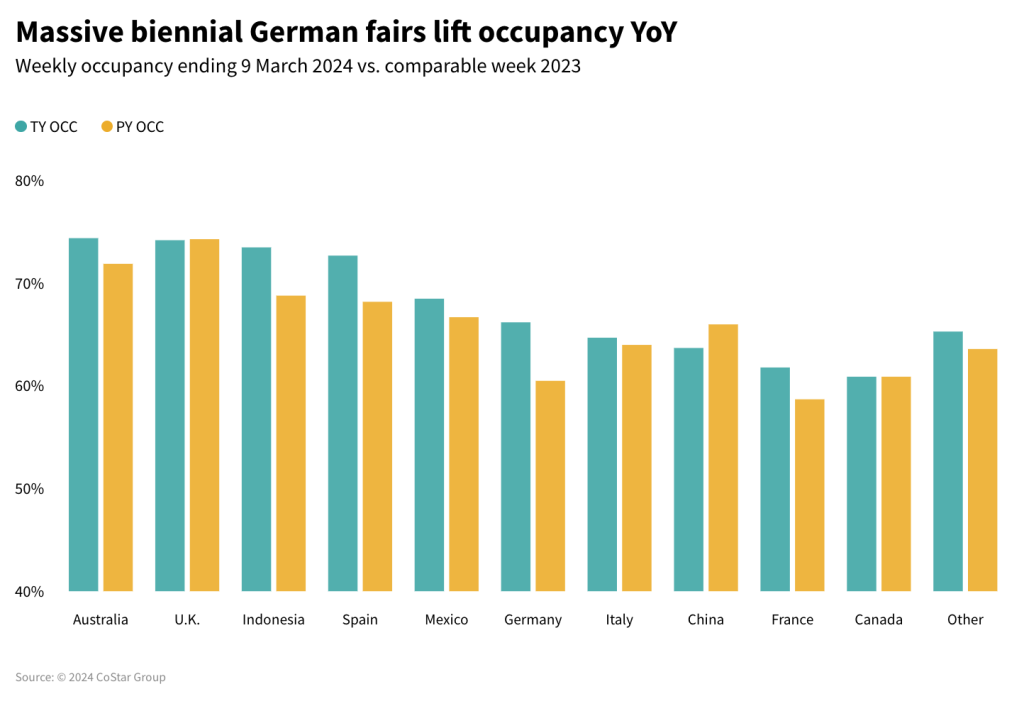

Among the countries with the largest hotel supply in the world, Germany led with the highest RevPAR growth (+27.9%). Occupancy in Germany increased 5.7ppts to 66.2% with ADR up 16.8%. Performance was boosted by large trade fairs across the country, particularly biennial events in Cologne and Frankfurt. The Lighting + Building trade show led Frankfurt to a 108% RevPAR gain with occupancy rising 11.7ppts and ADR growing 78.7%. Cologne hosted the EISENWARENMESSE – International Hardware Fair. As a result, occupancy rose 14.5ppts to 80.4% and helped propel ADR upwards by 60.7%, leading to a 91% RevPAR gain. While Frankfurt and Cologne led German Markets, nearly all others saw double-digit RevPAR growth for the week. Only two markets reported decreasing RevPAR.

Indonesia Gains Occupancy Again

Indonesia occupancy has surpassed 2019’s level in all but one week this year and has been above the level seen last year in all but two weeks. From the beginning of the year, occupancy has grown 13.2ppts and similarly last year grew 12.2ppts. Looking forward, we expect occupancy to soften due to Ramadan, which began on 11 March.

Singapore Loves Taylor Swift

Taylor Swift’s performances in Singapore concluded on Saturday, resulting in impressive ADR growth (+32.1%) and a rise in occupancy (+11.2ppts). RevPAR grew 50%, which was the largest increase of the past 25 weeks. Occupancy (88.7%) was the highest seen since mid-June 2023.

Solar Eclipse Impact

In early-April 2024, a total solar eclipse will once again pass over many North American cities, resulting in a room demand spike. Compared to the last eclipse in August 2017, this one is expected to last longer with the duration of totality almost double that of 2017. More importantly, it will pass through more large hotels markets than the last one, from San Antonio to Montreal, and it will happen during the spring break season. While both 2017 and 2024 eclipses occurred on a Monday, due to the above-mentioned factors, we expect to see higher occupancy, ADR and RevPAR levels in the eclipse markets on the days leading up to the event and the event day itself.

Looking ahead

The softness in U.S. RevPAR may be a sign of a correction. Long gone are the continuous gains experienced post-pandemic. The next three months will provide greater clarity into the strength of the industry. However, we remain optimistic, buoyed by positive forward-bookings trends, strong group demand, an early spring break season (nearly 40% of school students be on spring break next week), and the solar eclipse. Next week’s data should include several markets showing a boost from the many NCAA basketball conference tournaments taking place. Global performance is also expected to remain on a positive trajectory over the coming months as the stabilization seen continues