By Lionel Schauder and Sophie Perret

Brussels, with a population of approximately 1.2 million, enjoys a strategic location in the heart of Western Europe, making it both a regional metropolis and an international hub. In addition to its role as capital of Belgium, the city is home to NATO’s headquarters and is widely known as the ‘capital of Europe’, hosting both the European Parliament and the European Commission. Described as the ‘new Berlin’ by the New York Times in 2015, an eclectic and creative facet of Brussels has recently emerged, represented by its community of artists, architects and designers.

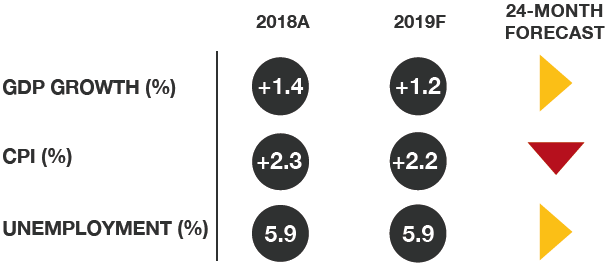

ECONOMIC INDICATORS – BELGIUM

Sources: Economist Intelligence Unit; IMF

Sources: Economist Intelligence Unit; IMF

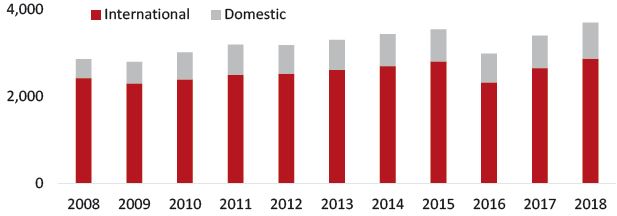

Tourism Demand

Arrivals in Brussels grew consistently since the decline observed in 2009 – following the economic crisis – to 2015. After the terrorist attacks in March 2016, which highly impacted visitation to the city, 2017 showed signs of recovery, primarily coming from the business demand generated by the various EU and international entities based in Brussels, while leisure demand was still below previous levels. However, the Leisure segment recorded the strongest growth in terms of arrivals and bednights in 2018 and is now accounting for 49% of the total demand, broadly in line with historical levels. The MICE segment also recorded a positive year.

VISITATION – BRUSSELS (000s)

Source: TourMIS

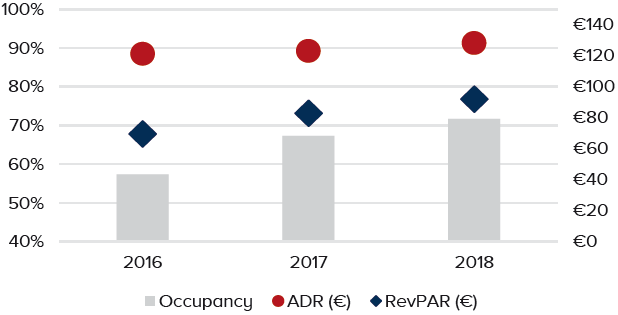

Hotel Performance

- Brussels hotel market’s occupancy grew from the low 60%s in 2009, following the economic crisis, to around 70% in 2015, before the March 2016 terrorist attacks and lockdown of the city which caused a significant decline in room nights for that year. However, 2018 saw the return of the Leisure segment, allowing occupancy to fully recover and even exceed the 70% mark;

- Overall, hoteliers (especially at the upper end of the spectrum) managed to maintain average rate levels in 2017, despite the challenging situation. Figures for 2018 indicate a healthy increase, although we note that average rate in constant (uninflated) prices remained below the 2009 level;

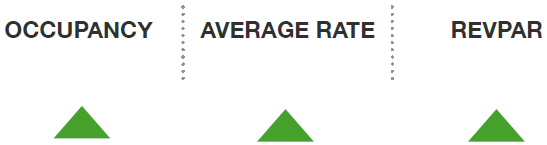

- Performance for the first quarter of 2019 indicates that the positive trend in occupancy and average rate continues, as illustrated by another impressive RevPAR growth of almost 10% over the same period last year.

KEY METRICS – BRANDED HOTELS

Source: HVS Research

PERFORMANCE Q1 2019

Source: HVS Research

Hotel Supply

With Brussels being primarily a business-driven market with a substantial number of corporate clients, three-star and four-star properties represent more than half of the total number of hotels.

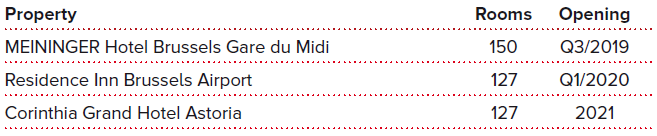

HOTEL PIPELINE – BRUSSELS

Source: HVS Research

The pipeline of new rooms coming to the city centre represents only 1.5% of the current supply. Brussels city centre is expected to see the opening of nearly 300 rooms in the next few years, spread over two hotels of different categories. The 170-room MEININGER Hotel Brussels Gare du Midi is expected to open in the third quarter of 2019, followed by the reopening of the 127-room Hotel Astoria, vacant since 2006 and acquired in 2016 by Corinthia in order to be fully renovated into a luxury property. We also highlight the rebranding of the NH Brussels Bloom hotel into a nhow (H2 2019) and there are plans to rebrand the 511-room Sheraton Brussels Centre which closed in December 2016. In addition, it was recently announced that, as of November 2019, the Hilton Brussels City will be rebranded to an Indigo and subject to a renovation programme. Furthermore, the adjacent Crowne Plaza Le Palace will also be subject to a comprehensive renovation and a potential extension of around 150 rooms on the adjacent plot of land, scheduled for 2022.

Investment Market

Brussels’ hotel investment market is somewhat less liquid than leading European markets such as London or Paris. The transaction volume in 2018 decreased to €77 million from the €101 million achieved in 2017 and represents a third of the record – €228 million – reached in 2016. The most recent transactions include the sale of the Aloft Brussels Schuman by Thornsett Group in April 2019 to a joint venture between Extendam, Schroder Invest and Silverback for an undisclosed price; and the Sheraton Brussels Airport sold by Blackstone to Brussels Airport Company in February 2019 for €37 million. For the latest value trends, please refer to our European Hotel Valuation Index.

HOTEL TRANSACTIONS – BRUSSELS

![]()

Source: HVS Research

Outlook

In addition to its resilient corporate demand, Brussels can now capitalise on the return of leisure and MICE demand to fully recover from the 2016 events, with the current pipeline not representing an immediate challenge for the short to medium term. Moreover, the city has recently seen the first benefits of its actions directed towards the promotion of the city as a city-break destination, which is expected to continue to have a positive impact on occupancy levels. Overall, Brussels remains a strategic city with solid fundamentals, and its improved performance is only likely to further advance its prospects in the eyes of investors.

VALUE TREND

Source: HVS Research