By Chris Remund

Over the past several years, Austin has been one of the fastest developing cities in the United States. Festivals such as South by Southwest, Formula One racing at the Circuit of the Americas, and its long standing reputation as the “Live Music Capital of the World” has propelled the city onto the international stage. Austin is a growing technology hub, home to major offices for multi-national companies such as Oracle, National Instruments, Dell, and IBM, to name a few. The city was once again named America’s fastest growing city by Forbes magazine in 2016, taking the number one spot in five of the past six years. Home to numerous entertainment venues and historical attractions, Austin has long been a major tourist destination, and is also home to the University of Texas, one of the largest universities in the U.S. Add in a solid base of government demand, and you have a city that serves as a cultural, economic, and political powerhouse, rivaling many of the traditional top U.S. 25 hotel markets in terms of strength and diversification of demand.

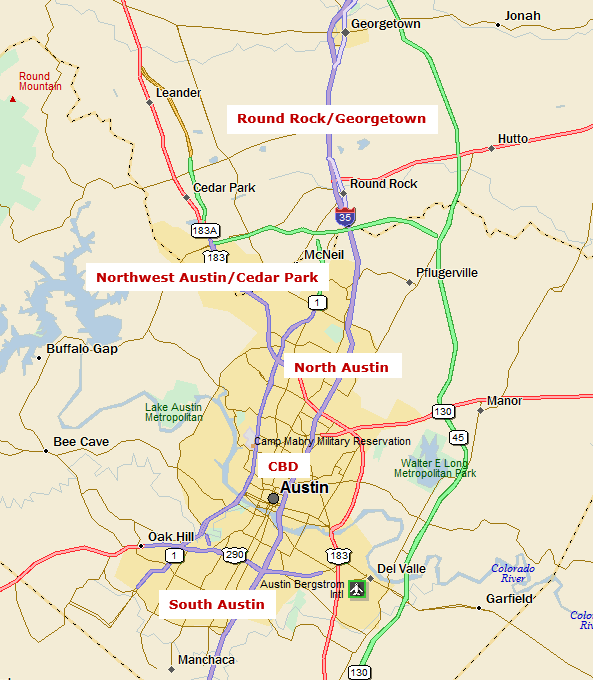

Lodging Market Overview, a Growing City  The Austin lodging market can be broadly divided into five submarkets which include: the Central Business District, North Austin, Round Rock/Georgetown, Northwest Austin/Cedar Park, and South Austin. However, as the greater Austin lodging market continues its rapid expansion, these submarkets have become blurred as new hotels open throughout the city. Areas such as West Austin, East Austin, and Austin-Bergstrom International Airport are all seeing an influx of new hotel development, creating newer mini-submarkets. However, the majority of the large, first-class full-service hotel properties remain located in Downtown/Central Austin, near the convention center, the University of Texas, and the Capitol building. The CBD market currently features roughly 8,500 hotel rooms, or nearly 25 percent of total supply in the city. However, even with the current room supply downtown, many developers believe the CBD market remains underserved and the downtown area is experiencing the largest influx of new hotel supply. Five hotels and 2,002 rooms opened over the past year and more than eleven projects, containing over 3,000 rooms, are currently in varying stages of the development process.

The Austin lodging market can be broadly divided into five submarkets which include: the Central Business District, North Austin, Round Rock/Georgetown, Northwest Austin/Cedar Park, and South Austin. However, as the greater Austin lodging market continues its rapid expansion, these submarkets have become blurred as new hotels open throughout the city. Areas such as West Austin, East Austin, and Austin-Bergstrom International Airport are all seeing an influx of new hotel development, creating newer mini-submarkets. However, the majority of the large, first-class full-service hotel properties remain located in Downtown/Central Austin, near the convention center, the University of Texas, and the Capitol building. The CBD market currently features roughly 8,500 hotel rooms, or nearly 25 percent of total supply in the city. However, even with the current room supply downtown, many developers believe the CBD market remains underserved and the downtown area is experiencing the largest influx of new hotel supply. Five hotels and 2,002 rooms opened over the past year and more than eleven projects, containing over 3,000 rooms, are currently in varying stages of the development process.

Growth in other areas of Austin is primarily driven by increased land prices in the central part of the city, the growth in population and development of Austin’s suburbs, and the desire of developers to look for alternatives to the already very competitive downtown market. One of the more notable growing “mini-submarkets” is the Domain, a large upscale residential, retail, and office development located 12 miles north of downtown Austin. The Westin Domain opened in 2010, while more recent additions include an aloft hotel in 2011, Valencia Group’s Lone Star Court in December 2013, and a Home2 Suites in April 2015. More new supply is on the way with the 171-room Archer Hotel Austin slated to open by the end of 2016. Recent hotel development in Austin’s other submarkets is primarily restricted to major branded upscale extended-stay, limited-service, and select-service hotels, with notable exceptions being the 194-room Hotel Granduca and 195-room Sonesta Bee Cave, both of which opened in the western part of Austin in 2015, and the 222-room Sheraton Georgetown, which opened at the end of July 2016.

Supply Growth Pushes Outside of the CBD Strong performance metrics over the past five years has resulted in a surge of new hotel supply, and the growth is showing no signs of slowing down. Since January 2015, 18 hotels have opened, totaling over 3,500 rooms. In addition to a number of downtown hotels, new properties are opening up in neighborhoods that traditionally lacked first-class accommodations, such as the South Congress district and East Austin. Overall, the addition of new hotel properties over the past 18 months represents an increase of roughly 13 percent of total room supply in Austin, while in the downtown market, room supply increased roughly 33 percent. The following chart outlines hotel properties that opened in Austin since 2015, the most notable projects being the 1,012 room JW Marriott and the 366 room Westin, both developed by White Lodging Services, Inc. Three new hotels recently opened just north of the city, a 91-room Home2 Suites in Round Rock, a 78-room Hampton Inn & Suites and the Sheraton in Georgetown.

Despite the recent substantial rise in hotel supply, Austin’s lodging pipeline remains robust. There are nearly 25 projects in various stages of development, including 15 hotels currently under construction. Half of these projects are located in the downtown area, while other projects are spread throughout the metro area. Over 2,900 rooms are expected to be added to the city by the end of 2017, roughly 10 percent of current supply, with nearly 1,500 more rooms in various other stages of development. The chart below depicts potential new hotel supply.

The most notable proposed hotel projects currently in the pipeline include the 1,048-room Fairmont Austin, which will be located directly east of the convention center, the dual-branded aloft/element hotels at Congress and 7th Street, and the Archer Hotel Austin, part of a new boutique hotel brand that debuted in New York in 2014. The airport market is growing with one new hotel, in addition to the new Residence Inn Austin Airport, which opened in July. Other neighborhoods experiencing new supply include North and Northwest Austin, the Domain, and South Austin.

As new hotel properties continue to open, the pressure is mounting for current property owners to renovate and improve their properties. The Hilton Austin recently began a $23 million improvement project set to be completed in the Fall of 2016. Improvements include lobby, meeting room, and other public area renovations. The hotel will also reinvent its existing food and beverage outlets and open the Reverbery, a banquet hall concept, Austin Taco Project, and Cannon + Belle. The hotel spent roughly $29,000 per room in 2014 renovating its guestrooms and executive lounge. Other notable renovation projects include the $27,000 per key renovation of the Hyatt Regency’s guestrooms in 2015 and the addition of a parking garage and 14,000 square foot Zilker Ballroom to the hotel in 2014. Following its purchase by the Sydell Group earlier this year, it was announced that the Radisson Hotel & Suites in downtown Austin will be renovated and converted to a Line Hotel. The $75 million renovation will address all areas of the hotel and is expected to be completed by the spring of 2018. Even newer hotels are undergoing renovation projects, with the JW Marriott adding a 4,600 square foot spa expected to open in the Fall of 2016.

New lodging development is also looking outside the traditional hotel developer’s “box.” A 12 room “luxury hostel” is opening in East Austin in late 2016/early 2017, partially funded by a NextSeed crowdfunding campaign. In April 2016, it was announced that Rob Mossburg and Rockford Construction signed a $150 million agreement to develop eight WaterWalk franchises in San Antonio, Denver, Dallas, and Austin. Billed as ‘hotel apartments,’ the properties feature hotel-style amenities and fully-furnished units inside gated multifamily communities. The WaterWalk franchise is spearheaded by Jack DeBoer, the founder of modern extended-stay hotel brands such as Residence Inn and Summerfield Suites (now Hyatt House). Additionally, Kalahari Resorts announced in June 2016 that they plan on developing a 1,000+ room Kalahari Resort in Round Rock. The $250 million project will be located near the Dell Diamond minor-league baseball stadium and feature indoor and outdoor waterpark facilities, restaurants, a spa, and a convention center. As the greater Austin lodging market continues to expand, current owners have cited the availability of skilled labor as a concern. With a sub-3.0 percent unemployment rate in the city of Austin, new and existing hotel owners will have to compete for top candidates.

Occupancy Remains Strong Despite New Supply Austin’s standing on the international stage has led to impressive hotel performance metrics and trends. According to city officials, citywide occupancy has increased every year bewteen 2010 and 2015 and average rate has increased roughly 6.0 percent per year over the same period. The CBD illustrated a similar occupancy trend, with the exception of minor dips in 2013 and 2015 as new supply was absorbed, while CBD average rate increased 8 percent, on average, every year since 2010. Citywide occupancy finished at 73.8 percent in 2015, a slight increase over 2014, while the CBD market experienced a slight decline, finishing the year at 77.4 percent. The CBD occupancy decline of less than two percentage points is still impressive given the substantial influx of new hotel rooms. In the year-to-date period through June 2016, which includes the peak month of March, citywide occupancy reached 75.3 percent, while the downtown market finished the first half of the year at 79.8 percent, both slightly less than 2015 statistics. As new supply enters the market, occupancy will likely continue to be reduced in the short term, while continued average rate increases should result in moderate RevPAR gains.

Hotel Sales Overview With all of the positive press over the recent past, it is no surprise that investors have been looking to Austin to supplement their hotel portfolios. Based on data from STR, Austin led secondary hotel markets in terms of transaction activity during 2015, with 10 hotels transacting at an average price per room of $311,000. This price per key rivaled the majority of the top 25 hotel markets, being exceeded by only five cities. Notable select single-asset transactions are outlined below.

Recent sales have run the gambit from smaller select- and limited-service properties to major full-service hotels including the Four Seasons and Radisson Hotel & Suites. Prices per key rival many top cities as investors are confident in the long term prospects of the Austin market. Notably, the dual-branded Holiday Inn Express and Hotel Indigo that opened downtown during the spring of 2016 is already on the market for sale, being marketed by Holliday Fenoglio Fowler (HFF) for the developer, JCI Hospitality.

City-Wide Development Austin’s building boom is not restricted to hotels. The city is filled with cranes in the process of constructing robust office and multi-family developments. More than 5,800 multifamily units have been added since 2015 and over one million square feet of office space is currently under construction. Austin will soon be home to the tallest residential tower west of the Mississippi and East Austin is home to a multitude of new multi-family projects. Major mixed-use projects are also underway, including the redevelopment of the Green Water Treatment Plant, part of the Seaholm Development District. Notable development projects are further outlined below.

- The University of Texas Dell Medical School welcomed its first students in June 2016. The school is the first new medical school at a tier 1 university in over 50 years and hopes to revolutionize how doctors are trained. The school’s $250-million Dell Seton Medical Center teaching hospital topped out in November 2015 and is on pace to be completed by 2017. The new state-of-the-art facilities are expected to create 15,000 direct and indirect jobs in Austin.

- The Seaholm Development District lies on a 7.8-acre site in downtown Austin, formerly home to a city of Austin power plant. Initial construction commenced in 2013, with the first phases opening in 2015. The project consists of a mix of residential, retail, office, and restaurant uses, including a Trader Joes grocery store and the New Central Library. Major office tenants include Under Armour and Athenahealth, and as of May 2016, 100 of the 280 condominium units had been occupied. Including $100 million in infrastructure improvements by the City of Austin and an additional $120 million towards funding the library, roughly $2 billion has been spent on redeveloping the area.

- Led by master developer Trammell Crow Company, the former Green Water Treatment Plant is currently undergoing redevelopment into a mix of residential, office, hotel, and retail spaces. The first phase of the project includes an office tower at 500 West 2nd Street with 489,403 square feet of leasable space, a 436-unit apartment tower, and ground floor restaurant and retail spaces. Google is confirmed to be leasing 200,000 square feet of office space in the new office building, which is expected to be completed in first quarter of 2017. The Austin Proper Hotel is also part of the project, which includes 245 hotel rooms and 99 branded luxury residences. At completion, the redevelopment project will contain approximately 1.7 million square feet of new space.

- The Independent is a 370-unit, 58-story residential tower currently under construction in downtown Austin. The tower broke ground in January 2016 and is set to open in 2018. The property will be the tallest residential tower west of the Mississippi, with units priced in the mid-$400,000s to over $3 million.

- Austin-Bergstrom International Airport is currently undergoing an expansion project set to increase capacity by four million passengers per year. The $350-million project will add 70,000 square feet of facilities including new concessions, restrooms, walkways, and nine additional gates at the east end of the airport. The project is expected to be complete by late-2018.

The Convention Center Question The influx of new hotels in downtown Austin has allowed the convention center to better compete with markets such as Denver, San Antonio, and Nashville, many of which recently underwent or are undergoing their own hotel supply boom and/or convention center renovations/expansions. The opening of the JW Marriott Hotel, among others, as well as the pipeline of first-class hotels in the downtown CBD has attracted less price-sensitive corporate, technology, and medical conferences. However, despite all of the new hotel properties, many of the convention center’s main competitors have as much as two to three times the convention space and many more lodging options in close proximity to the center. For example, San Antonio’s newly expanded convention center features over 500,000 square feet of contiguous convention space and nearly 10,000 hotel rooms within close proximity, versus roughly 250,000 square feet of exhibit space in Austin. Continued new supply will allow the convention center to attract high-quality meetings and events; however, the lack of convention space remains a challenge for the Austin CVB.

Perhaps the greatest unknown that could substantially affect hotel performance over the coming years is the effort to expand the city’s convention center. Convention officials have said that the center is losing as many conventions as they are accommodating due to the lack of availability and space. A plan to expand the center by roughly 320,000 square feet is currently being considered by the city council and center officials are pushing for a ballot measure in November 2016 for voter approval of construction bonds. Voters could be asked whether or not to rededicate a 2 percent venue tax within the hotel occupancy tax collections to expand the convention center, without increasing property taxes. The cost of expansion is estimated at roughly $405 million, with an additional $45 million to $50 million in land acquisition costs. Other options for the land in question include partnering with the University of Texas to replace the Frank Erwin Center with a new sports arena; however, no other official proposals have been submitted. Expansion plans remain somewhat uncertain at this time and if plans proceed, the earliest an expanded center would open would likely be late-2021.

Future Outlook – Will RevPAR Growth Decelerate? Even with the substantial increase in hotel supply over the last year and a half in addition to the multitude of new rooms either under construction or proposed, local owners and operators remain bullish on the Austin market. Although new supply may hamper year-over-year occupancy gains, new, high-quality hotels are expected to allow for continued, albeit more sustainable, average rate growth. There is some concern that areas experiencing the largest influx of new hotel properties, such as downtown, may experience RevPAR declines as the new supply is absorbed into the market; however, operators appear confident in long-term performance, understanding that the double-digit gains over the last few years were not sustainable. Austin’s diverse base of lodging demand and strong fundamentals bode well for sustainable long-term growth.

In terms of future development, the Austin hotel pipeline represents an impressive mix of traditional nationally-affiliated focused-service hotels, independent boutique projects, and large full-service branded developments. As land prices increase, some developers have turned to mixed-use in order to finance their projects and maximize returns. Developments such as the Austin Proper, which contains a substantial residential component, may soon become the norm for most major new hotel developments.

Although concerns surrounding the influx of new hotel supply are justifiable, the expansion of office, multifamily, and medical sectors bode well for Austin’s future. A convention center expansion would certainly be a welcome addition for local owners and operators, while projects such as the airport expansion prove that investment in the city is continuing at a healthy pace. Austin’s continued rapid expansion in the hotel, office, and residential sectors has propelled the city to new levels and begs the question whether a city that will soon house the largest Fairmont hotel in the world and tallest residential building west of the Mississippi can truly be considered a second-tier city.