By Krish Vipani

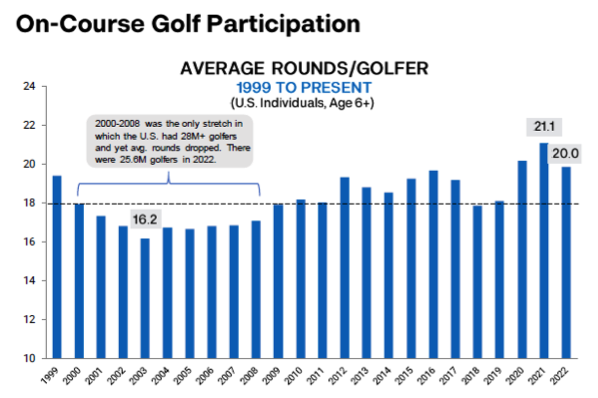

Without a doubt, leisure sports picked up in popularity during the COVID-19 pandemic- especially golf. According to the National Golf Foundation, 67% of golfers credited their increased play in the late summer of 2020 to having “fewer alternative ways to spend leisure time”. Not only did existing golfers increase their time on the course, but the National Golf Foundation also reports 25.6 million golfers on the course in 2022, a 1.3 million increase from 2019. Moreover, the National Golf Foundation reports an average of 21.1 rounds of golf played per golfer in 2021. This is the greatest average number of rounds per player in a single year seen since 1999.

Thesis

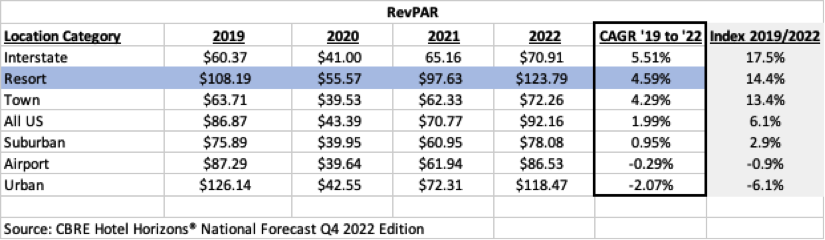

According to the CBRE Hotel Horizons® National Forecast Q4 2022, hotels in resort locations achieved the second highest RevPAR CAGR (4.59%) from 2019 to 2022, behind only hotels in interstate locations. Interestingly, the RevPAR for hotels in resort locations was 14.4% greater in 2022 than pre-pandemic levels in 2019. Based on location type, we assumed hotels in resort destinations benefited from “revenge travel” or pent-up leisure demand given the underlying trend in performance. Being that this pent-up demand in leisure includes an increase in golf play, we explored the subsequent impact to the hotel industry by analyzing the performance of hotels in resort locations with golf amenities.

Resorts With Golf Courses vs. Resorts with No Golf Amenity

We studied the performance of 55 resorts with an average over 500 rooms that provided an annual operating statement to CBRE from 2018 to 2022. Our research focuses on the period from 2019 to 2022 to highlight the impact of the pandemic. The composition of the data set includes two property groups: 22 resorts with golf amenities and 23 resorts with no golf amenity. Based on our analysis, we were surprised to see a minimal difference in CAGR for occupancy, ADR and RevPAR between the two property groups. Albeit unknown variables such as disruption in property operations from renovations, changes in supply, group booking patterns or other factors, we were further encouraged to investigate golf departmental revenues given the lack of disparity.

Golf Department Analysis

At the resorts that offered golf as an amenity, we observed an increase of 65.5% in golf revenue from 2019 to 2022 despite a drop in occupancy of 7.5% from 66.8% in 2019 to 61.8% in 2022. Golf revenue per available room increased by 66.3% from $7,730 in 2019 to $12,854 in 2022. With golf revenue growing faster than total revenue, golf revenue increased as a percent of total revenue from 2019 to 2022. With potential validation to our thesis, golf revenue per occupied room increased by 79.6% from $31.71 in 2019 to $56.95 in 2022—suggesting golfers composed of a larger percent of guests in 2022 compared to 2019.

Lack of Disparity in Revenue: Golf vs Non-Golf

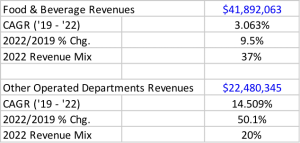

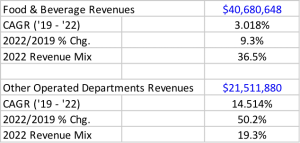

Although golf revenue contribution increased and the percent of golfers as hotel guests likely increased, hotels with golf amenities certainly did not outperform resorts without golf. We looked at the Food & Beverage Revenues to examine if resorts without golf courses were compensating for their income in this department. However, Food and Beverage Revenues for both property sets achieved a CAGR around 3% from 2019 through 2022 and had only a $1,211,415 difference in revenues. We analyzed the other operated departments, which golf departmental revenues are recorded in, for both property types to gain a better understanding for the lack of discrepancy. The CAGR for Other Operated Department Revenue from ’19-’22 was approximately 14.5% for both types of resorts. The substitutional amenities available at resorts with no golf courses clearly closed the gap in revenue between resorts with golf courses. Such amenities at resorts with no golf amenity include tennis, pool/water parks, spa, beach clubs and gift shops.

Golf Resorts

Non-Golf Resorts

Conclusion

Hoteliers may be mindful of enhanced revenue generation from their golf departments as illustrated in this study. Golf revenue at resorts increased despite a decline in occupancy from 2019 to 2022. This trend could be attributed to a greater mix of golfers as total guests post-COVID, an increase in green fees with greater golf demand, higher pro-shop spending with increased play, and potentially increased play from local residents. Golf resort recovery would most likely have been worse had it not been for increased golf play. The increased play did not create premium occupancy and ADR performance over non-golf resorts; however, golf play was a significant contributor to the success of golf resorts post pandemic. Without such an examination, hoteliers may not have realized the potential leisure sports, especially golf, can embark on the hospitality industry.