Note: Due to the Christmas and New Year’s holidays, the next edition of Weekly Insights will run on 12 January 2024

Analysis by Isaac Collazo, Chris Klauda, Will Anns

Countries included: China, Germany, Japan, United Kingdom, and the United States

Highlights

- The Top 25 Markets propelled U.S. RevPAR growth to a three-week high.

- Group demand gained.

- Soccer ruled in the U.K. and Germany with all but one of the five markets hosting UEFA Champions league matches posting double-digit occupancy increases.

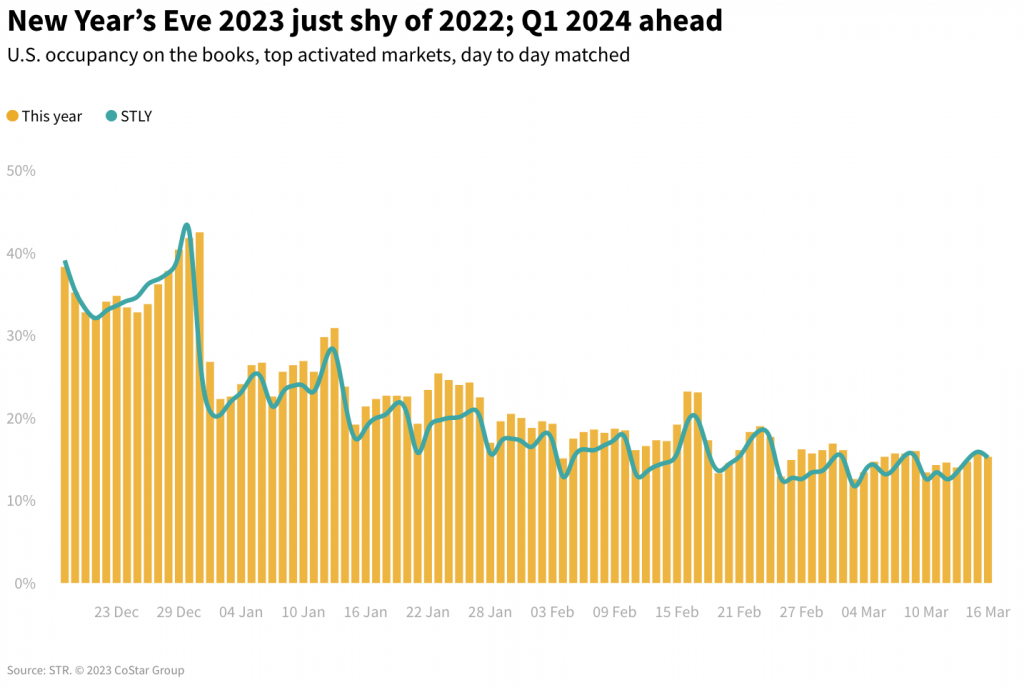

- College Bowl games and New Year’s Eve will provide a boost to the industry as the year winds to a close. New Year’s Eve demand is expected to be down slightly in the U.S. and up in most other countries around the rest of the world.

U.S. performance

U.S. hotel revenue per available room (RevPAR) rose by the highest percentage of past three weeks (+5.8%), which was also among the highest growth rates since April. The gain was propelled by the Top 25 Markets, where RevPAR was up 10.7%, driven by growth in San Francisco, Las Vegas, San Diego, and several others. RevPAR outside of the Top 25 Markets was up 1.1%.

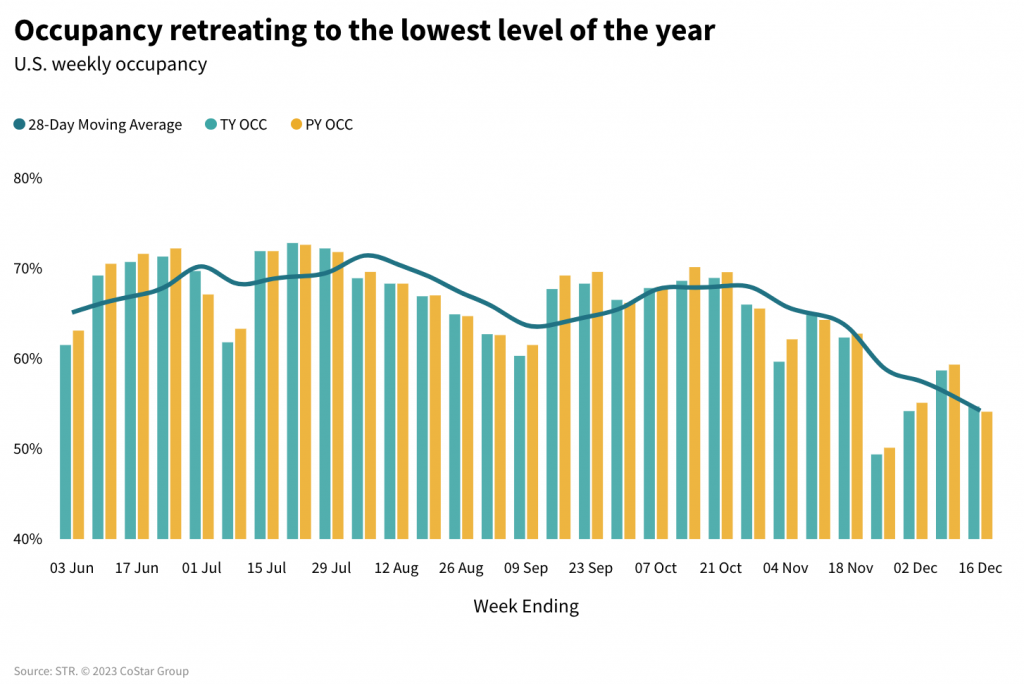

U.S. industry occupancy increased 0.6 percentage points (ppt) year over year (YoY) to 54.7% with average daily rate (ADR) rising well ahead of inflation at +4.7%.

Like a few weeks ago with its F1 Grand Prix event, Las Vegas saw strong performance again via the National Finals Rodeo, Cowboy Christmas, and a Las Vegas Raiders Thursday night game helping to drive RevPAR up 54.1% YoY. The strong growth came even with new supply from the opening of the 3,644-room Fontainebleau Las Vegas.

U.S. industry occupancy calculated without Las Vegas was still up (+0.1ppts), and ADR gained 3.8% (ahead of inflation), netting a RevPAR increase of 4.0%. Las Vegas is the largest U.S. market, accounting for 3.1% of U.S. room supply. When significant events occur in a market the size of Las Vegas, especially during December, which generally sees the lowest demand of the year, the impact is felt throughout the country.

While Las Vegas posted strong performance, San Francisco took the top spot with RevPAR increasing 60.3% YoY as occupancy advanced 17ppts and ADR rose 21.5%. The growth was led by the fall meeting of the American Geophysical Union (AGU) at the Moscone Center. San Diego and New York City rounded out the list of the top RevPAR gainers with year-over-year increases of 27.3% and 25.7%, respectively. Both markets attracted increased group and transient business during the week.

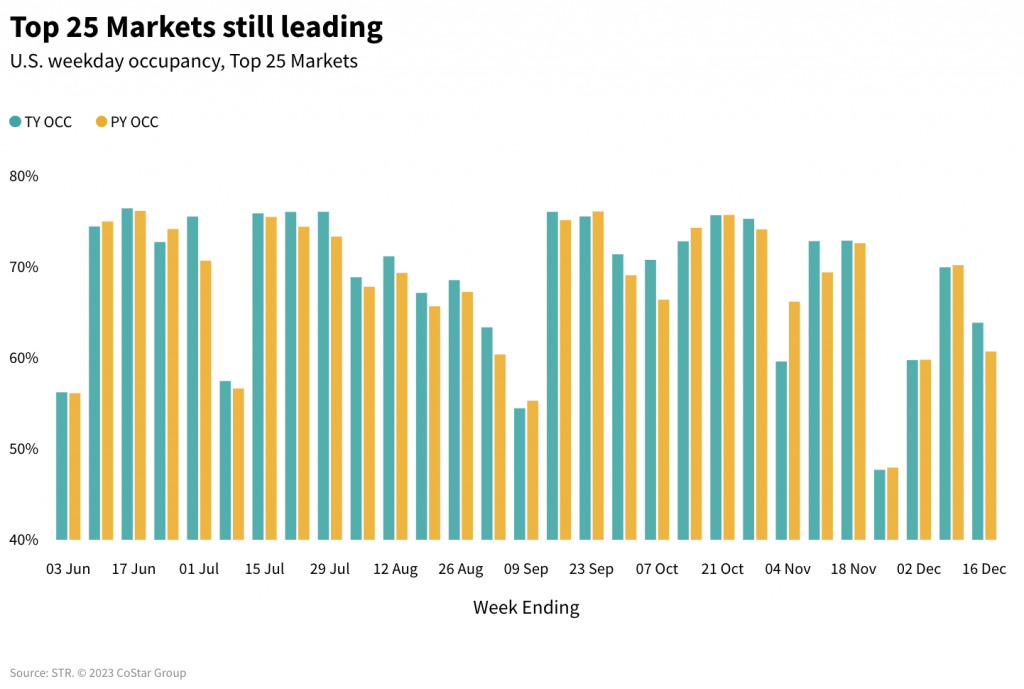

As in past weeks, the Top 25 Markets drove industry growth with RevPAR growth (+10.9%) dominated by strong ADR (+6.8%) and a solid occupancy increase (+2.3ppts). Even when excluding Las Vegas, Top 25 Market RevPAR was up 7.4%, almost exclusively due to ADR increasing 5.7%. While performance in the Top 25 was good, it still paled the level of growth seen in 2019 when occupancy reached 72.1% (versus this year’s 63%) and RevPAR jumped by 16.6% YoY.

Weekdays (Monday-Wednesday) posted the largest occupancy gains across the Top 25 Markets, while the shoulder days (Sunday & Thursday) saw the highest ADR growth. Both weekdays and shoulder days produced a 12.5% RevPAR increase. The weekend (Friday & Saturday) in the Top 25 Markets showed RevPAR up 7.3%, driven by ADR (+5.7%). Outside of the Top 25 Markets, weekday RevPAR increased 3.8% followed by shoulder days growing 0.7%. Weekend RevPAR fell 2.0% on falling occupancy (-1.4ppts) and low ADR gains (+0.6%).

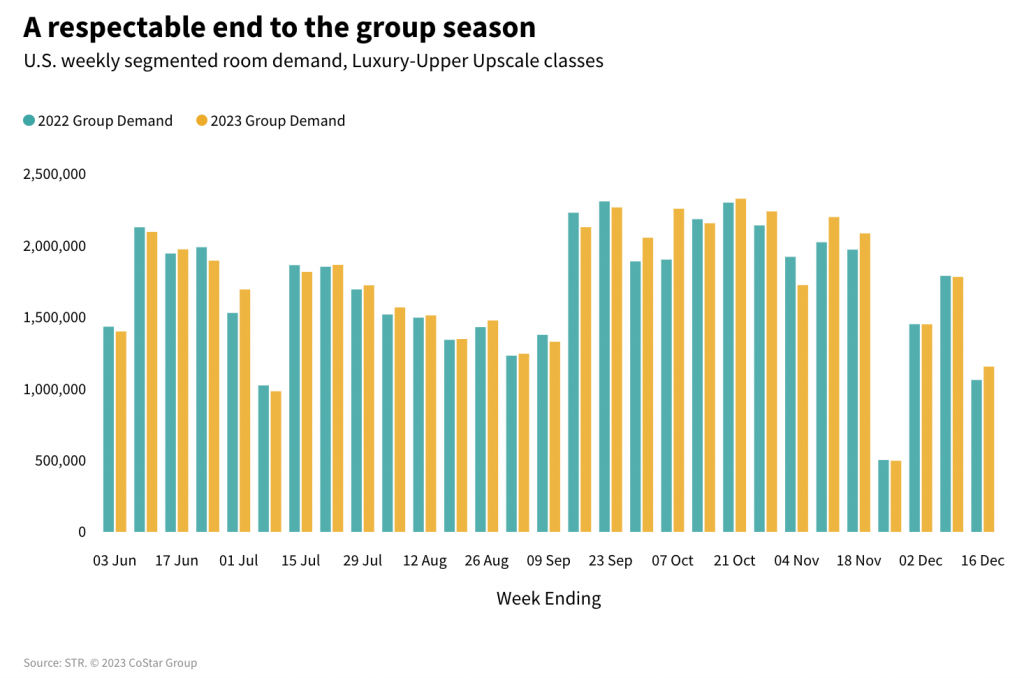

Group demand, which is generally slow this late into the year, posted a notable increase of 8.8% compared to the same week last year. San Francisco and San Diego increased group occupancy 18.8ppts and 4.3ppts, respectively. Atlanta also recorded a healthy gain with group occupancy up 6.0ppts, assisted by the Celebration Bowl.

The three top hotel classes, Luxury, Upper Upscale, and Upscale, dominated the industry’s RevPAR growth, increasing 8.8%, 8.6% and 7.8%, respectively. Luxury growth came entirely from occupancy, while Upper Upscale and Upscale growth was a result of both occupancy and ADR growth. RevPAR in the Upper Midscale segment increased 2.5%, led by ADR. Midscale remained flat (+0.5%), while Economy fell 4.3% on declining occupancy, which has been the case all year.

Global hotel performance

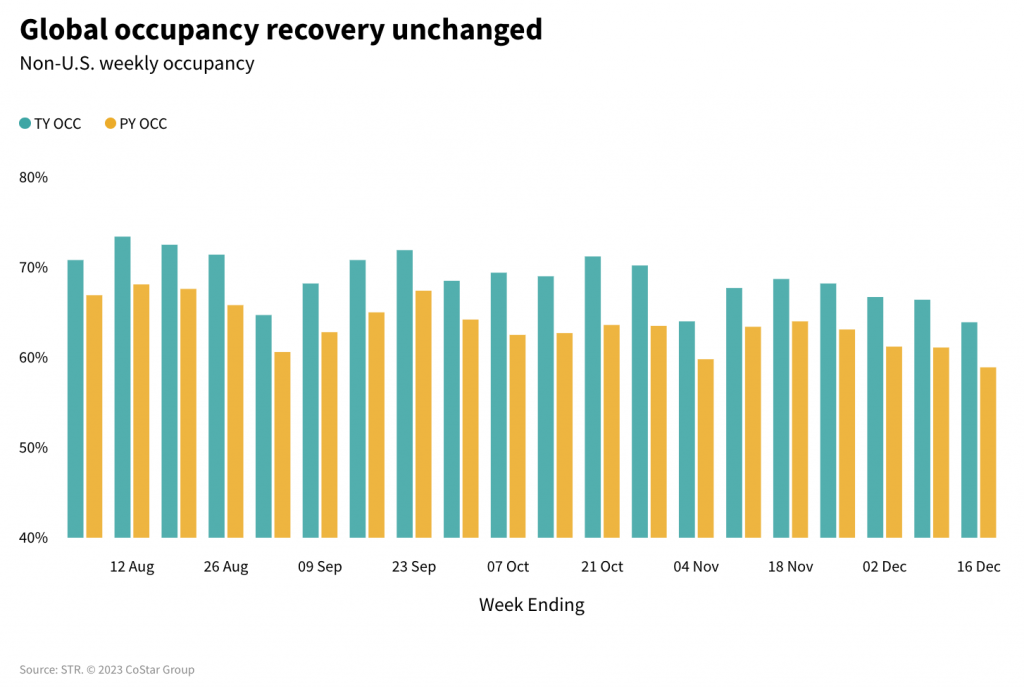

Global occupancy, excluding the U.S., continued to slow as the holidays near (63.9%) but continued to reflect strong year-over-year growth (+5ppts). ADR growth has also moderated from double-digit gains to +6.5%, which was the smallest increase of the year. RevPAR continued to show strong growth with the measure rising 15.6%, but that was also the smallest gain of the year.

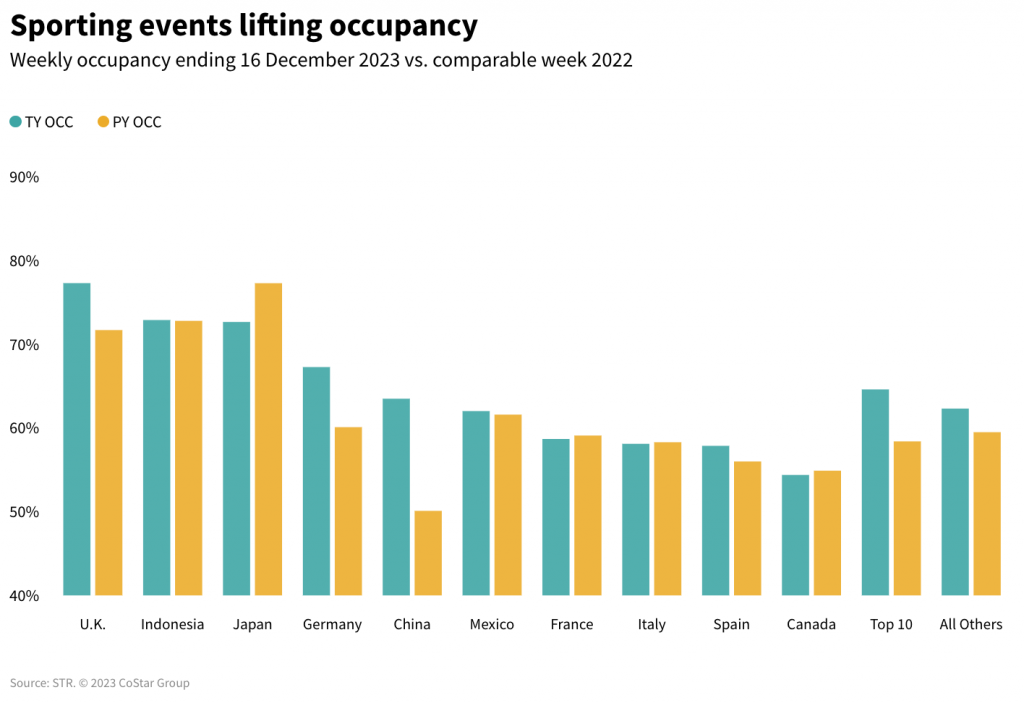

In the top 10 countries, based on total supply, the U.K. saw occupancy advance 5.6ppts to 77.3%, driven by the UEFA Champions league matches. Liverpool and Newcastle, which hosted an international match, saw some of the highest growth in the country as occupancy moved 16.5ppts and 11.3ppts, respectively. Germany also benefited from the league matches with several cities posting strong occupancy growth: Dortmund (+7.5ppts to 69.2%), Berlin (+4.6ppts to 67.6%), and Leipzig (+11.4ppts to 75.1%). Overall, Germany was among highest occupancy performers (67.3%, +7.2ppts), while the U.K. led.

China continued to see strong RevPAR gains with the measure rising 37.7% on a 29.1-ppt increase. Japan also saw robust RevPAR growth (+26.9%) followed by Germany (+19.5%) and the U.K. (+16.9%).

Over the past three weeks, Japan has seen posted occupancy decreases, down by 4.7ppts this week, with the measure falling in most markets. However, ADR growth has remained strong and continued to drive solid RevPAR increases. ADR has been up in each week this year with it rising by more than 35% in the fortnight.

Looking ahead

As the year ends, we expect U.S. ADR to remain strong despite falling demand. College bowl games will boost markets hosting those games and their surrounding events. New Year’s Eve, which historically produces the highest absolute RevPAR for the month, will be slightly softer than last year due to the calendar shift from Saturday to Sunday. However, we don’t expect ADR to suffer, and the industry should see strong RevPAR growth for the day. Additionally, Q1 occupancy on the books in the top U.S. markets is trending ahead of last year, indicating a strong start to 2024. Outside of the U.S., performance will remain robust, slowing as the new year advances.