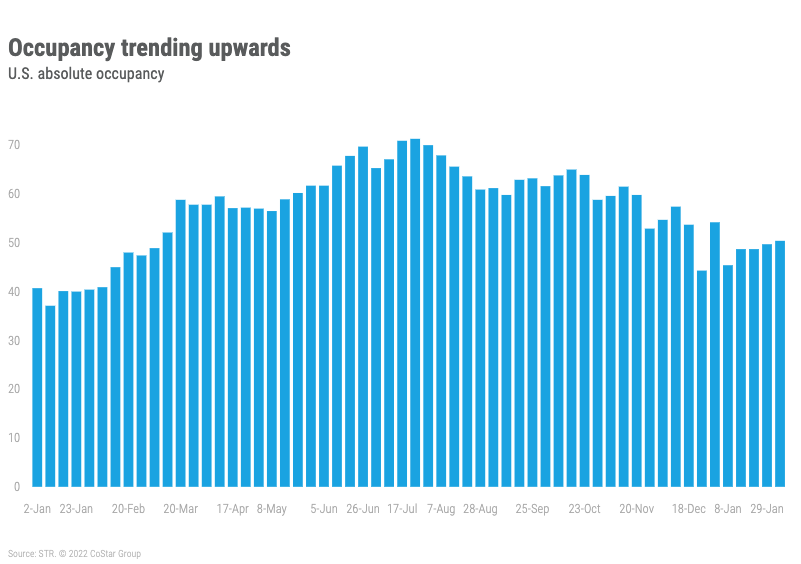

The post-holiday doldrums appear to be ending. U.S. hotel occupancy advanced again, rising 0.8 percentage points to 50.4% in the week ending 5 February 2022. This was the first time in the past five weeks that weekly occupancy surpassed the 50% level, although the index to 2019 fell from the prior week. All day categories saw growth in the week led by shoulder days (Sunday & Thursday) and the weekend (Friday & Saturday). Weekdays (Monday-Wednesday) also advanced. Average daily rate (ADR) increased by its largest rate since the holidays, up 2.1% week over week, driven by a weekend increase of 3.8%. With growth in both occupancy and ADR, revenue per available room (RevPAR) increased by the largest week-on-week percentage (3.6%) since the beginning of the year.

For a fifth consecutive week, airport hotels reported the highest occupancy (59%) of any location type. Severe winter weather over the past two weeks likely lifted demand for these hotels. Texas airport locations saw the largest bump in airport demand from the prior week. However, it wasn’t airport hotels that led to the national increase in occupancy and demand. Suburban hotels accounted for a third of the weekly demand increase, particularly in Nevada, California, and Florida. Urban and resort hotels each represented 20% of this week’s demand growth. We were pleased to see the improvement in urban hotels. Of the urban gainers, New Orleans, Houston, Nashville, Los Angeles, New York City, and Austin made up 50% of urban location growth during the week. On the opposite end, Atlanta, San Francisco, and Indianapolis accounted for most of the decrease among urban decliners. Despite the positive movement, urban hotels still have a way to go in their recovery as they were at just 68% of the comparable 2019 demand level. Interstate hotels saw demand that was 4% higher than it was back in 2019, while small metro/town locations were at the 2019 level. While airport hotels led the industry this week, demand for those properties was still 14% lower than what it was prior to the pandemic.

For the first time in eight weeks, the Florida Keys did not lead the nation in hotel occupancy. That honor went to Tucson, which posted an occupancy of 84.8%. The week prior, Tucson had the third highest market occupancy, and three weeks ago, it was in the 19th position. Florida markets continued to dominate the top 10 highest occupancy slots, but Arizona had the highest state occupancy (66.1%) followed by Florida (65.8%). The lowest occupancy was Washington, DC (37.5%) followed by Minnesota (39%). In terms of week-over-week demand growth, Nevada led the nation followed by California, Florida, and Tennessee. At the market-level, New Orleans, Los Angeles, and Houston saw the largest demand gains. New York City demand was also up, but occupancy remained on the low side (44%).

Central Business Districts (CBDs) also saw their largest occupancy increase of the past three weeks, rising by a percentage point to 40% with New Orleans, Houston, and Nashville leading the growth. The Atlanta CBD saw the largest weekly occupancy decrease, but the lowest occupancy was in the Minneapolis CBD (21%) followed by Chicago CBD (24%). Tampa remained the hot spot among CBDs (71%).

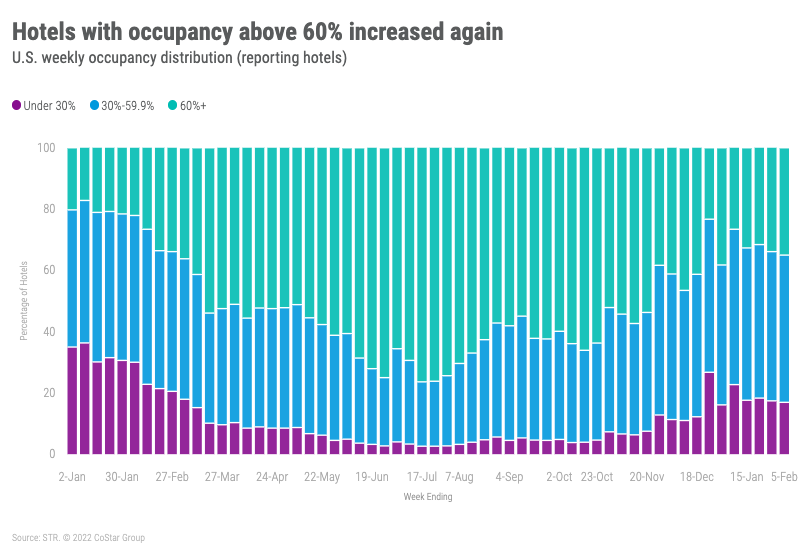

Group demand is slowly rising, but thus far in 2022, it remains at less than half of what it was in 2019. Predominately group-focused hotels reported occupancy of 44% in the week with those in the Top 25 Markets a bit lower (43%). While the average is moving upwards, we did see that 22% of group-focused hotels reported occupancy below 30%.

The 2.1% increase in industry ADR translated to a gain of US$2.52, with the largest contribution coming from resort hotels. They accounted for US$1.09 of the total industry gain. Resort locations also had the highest weekly ADR for the week (US$222). Urban hotels, which have seen good demand growth over the past two weeks, also showed solid ADR gains, contributing US$0.54 to the industry total. Urban hotels had the second highest ADR of any location type (US$149). ADR indexed to 2019 has remained nearly unchanged over the past four weeks at 98. Resort hotels were the strongest as compared to 2019 with a weekly index of 116 followed by small metro/town (113) and Interstate (108). Resort ADR has been above 2019 consistently since April 2021. Small metro/town and interstate hotels started surpassing 2019 levels shortly thereafter. Relative ADR for urban hotels is the furthest away from 2019 with a 10% deficit.

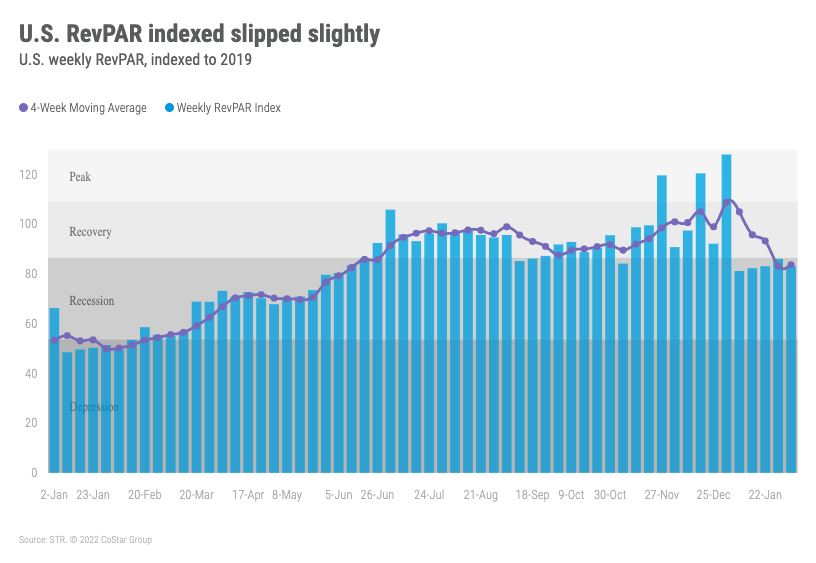

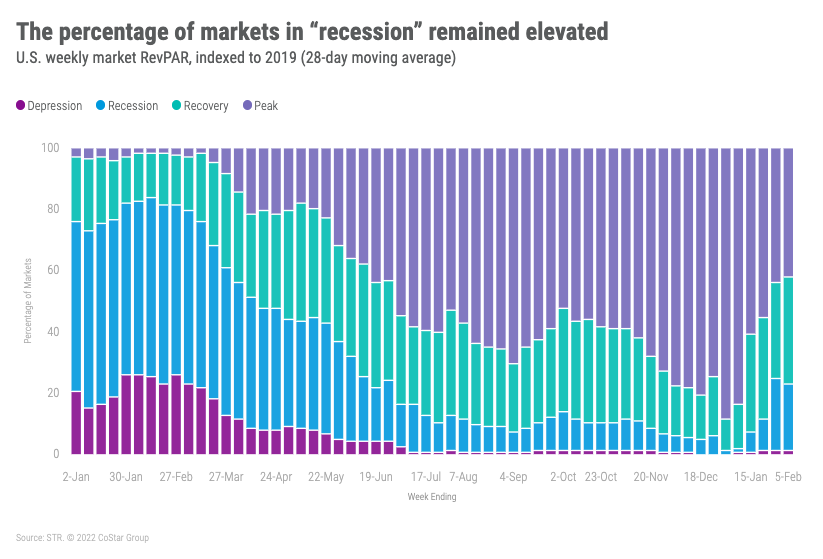

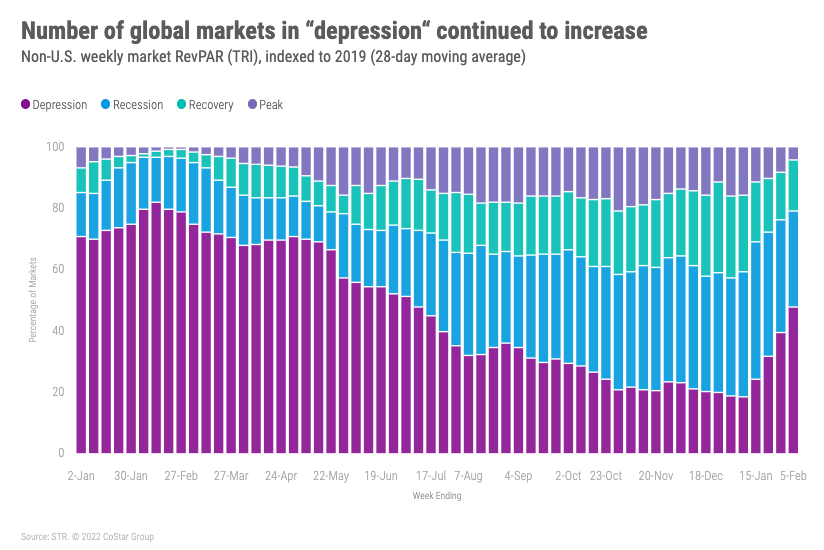

Even though the week-over-week RevPAR growth was the largest of the past three weeks, RevPAR lost ground to 2019 as the index fell from 86 to 83. This was the first decrease in the index of the past three weeks, and the decline was spread across all days of the week. Even with the weekly decline, industry RevPAR remained in STR’s “recovery” category (RevPAR indexed to 2019 between 80 and 100). Across the U.S., 36% of the 166 STR-defined markets were in “recovery” with 40% at “peak” (RevPAR indexed to 2019 above 100). Taking a broader view, over the past 28 days, the U.S. RevPAR index was at 84 with 42% of markets in “peak” and 35% in “recovery.” Because of the Omicron and post-holiday slowdown, 22% of markets were “recession” (RevPAR indexed to 2019 between 50 and 80) on a 28-day basis. The percentage of markets in the “recession” category has been elevated for the past two weeks and is at its highest level since June 2021. On an inflation-adjusted basis, 28-day industry RevPAR indexed to 2019 remained in the “recession” category for a second straight week.

Around the globe

After falling for four consecutive weeks, global occupancy, excluding the U.S., rose a half point to 38% with ADR increasing by nearly 10%—the second straight weekly gain. Weekly occupancy ranged from 76% in Guam to 13% in Morocco. Morocco closed its borders to all international arrivals in late-November but reopened on 7 February. Occupancy among the top 10 largest countries, based on hotel supply, was 37% with ADR rising by more than 16% week on week due to strong growth in China. China’s ADR was up sharply due to Lunar New Year celebrations and the beginning of the 2022 Olympic games. Occupancy ranged from 56% in the U.K. to 29% in Germany. While China drove the top 10’s ADR growth, the country’s occupancy was low at 31%.

Most global markets (48%) remain mired in “depression” (28-day RevPAR indexed to 2019 under 50) with another 31% in “recession.” The percentage of markets in “depression” has risen for the past four weeks. This week, 18% of the 348 non-U.S. markets had a RevPAR that was less than 30% of what it was in 2019, which was the most of the past six months.

Big Picture

While U.S. occupancy remains uncomfortably low, we are encouraged by the movement above 50% as well as the gains seen in urban locations. Looking ahead, STR’s School Break Report shows that nearly one-third of public schools will have a long President’s weekend (18-21 February) with 14% having the entire week off. Like last year, this will mark the return of leisure travel. Spring Break travel, also covered in the School Break Report, ramps up the week of 6 March for colleges and the following week for K-12 schools. At the same time, we expect business travel to strengthen along with groups and meetings. Better days are ahead.