By Ezio Poinelli , Pavlos Papadimitriou , Nana Boussia

Introduction

Tuscany is a region in central Italy with an area of about 23,000 km2 and a population of about 3.8 million (2013). The regional capital and most populated town is Florence with approximately 370,000 inhabitants while it features a Western coastline of 400 kilometers overlooking the Ligurian Sea (in the North) and the Tyrrhenian Sea (in the Center and South).

Tuscany is known for its landscapes, traditions, history, artistic legacy and its influence on high culture. It is regarded as the birthplace of the Italian Renaissance, the home of many influential in the history of art and science, and contains well-known museums such as the Uffizi and the Pitti Palace. Tuscany produces several well-known wines, including Chianti, Vino Nobile di Montepulciano, Morellino di Scansano and Brunello di Montalcino. Having a strong linguistic and cultural identity, it is sometimes considered "a nation within a nation".

Seven Tuscan localities have been designated World Heritage Sites by UNESCO: the historic centre of Florence (1982); the historical centre of Siena (1995); the square of the Cathedral of Pisa (1987); the historical centre of San Gimignano (1990); the historical centre of Pienza (1996); the Val d'Orcia (2004), and the Medici Villas and Gardens (2013). Tuscany has over 120 protected nature reserves, making Tuscany and its capital Florence popular tourist destinations that attract millions of tourists every year.

Accessibility

.jpg) Source: Lonely Planet

Source: Lonely Planet

By Air

Tuscany has two international airports, the “Galileo Galilei” in Pisa and the “Amerigo Vespucci” in Florence. Located only 80 kilometers apart, the Pisa airport is the larger of the two.

Pisa airport is located right next to a dual carriageway linking to the A1 motorway around Florence for easy access to destinations in Tuscany. Pisa airport receives a larger amount of visitors as it handles all the intercontinental non-stop flights reaching Tuscany. Florence airport is the nearest airport for most locations in Tuscany. It is a small but modern airport located is very close to the A1 motorway around Florence. Smaller planes fly into Florence due to its location. Inspite of the presence of these two airports, Rome Fiumicino , continues to attract a high number of visitors due to the big amount of international flights that land there.

By Car

Air travelers can fly into Milan or Rome and get transportation from there to Tuscany, about a three-hour drive by car from either direction. Roads are generally in a good state of repair throughout Tuscany and the system is comprised of regional, provincial and state roads and motorways. While there are major cities in Tuscany, the majority of the area is made up of small towns and villages that are best traveled to by car.

For travelers entering the country by car the main points of entry into Italy are the following:

- Mont Blanc tunnel from France at Chamonix which connects to the A5 for Turin and Milan

- Grand St. Bernard tunnel from Switzerland which also connects to the A5

- Brenner Pass from Austria which connects to the A22 to Bologna

By Train

The main train stations are located in Grosseto, Pisa and Florence. These cities as well as Siena, Lucca, San Gimignano, Arezzo and Volterra can be easily reached by train. Some train stations also have a connecting bus service that reach some of the more rural areas.

By Sea

Tuscany features a good port infrastructure with the main ports being the following: Livorno Harbour which has developed traffic with all the major ports in the world with the main destinations of the passenger turistic traffic being Sardinia, Corsica and Barcellona; the Port of Piombino in Livorno which provides many services for passengers and travellers who can take ferries towards Sardina, Corsica, Elba Island; and the Viareggio Harbour in Lucca. Additional smaller harbours or marinas are: Marina di San Rocco Port in Grosseto, Dockyard of Cinquale in Massa-Carra, Forte dei Marmi Touristic Pier in Lucca, Marina di Punta Ala in Grosseto and Port of Marina di Carrara in Massa Carra.

Provinces and Attractions

Tuscany is divided into ten provinces, each of them with its own distinctive identity: Arezzo, Pisa, Lucca, Prato, Siena, Livorno, Florence, Pistoia, Massa-Carrara, and Grossetto. At this point it should be mentioned that as the city of Florence constitutes a crucial market for the region of Tuscany that is fairly different from that of the countryside, we consider it necessary, for constistency purposes, to exclude from this article all data relevant to Florence and instead focus on the evolution of tourism in the countryside. Florence and its market pulse has been thoroughly presented in a past publication.

Some of the most famous attractions of Tuscany scattered throughout its provinces are the following:

- Piazza del Duomo and Renaissance Florence;

- Pisa's Leaning Tower and Campo dei Miracoli;

- Cathedral of Santa Maria Assunta in Siena;

- Lucca's Centro Storico (Historic Center);

- The Towers of San Gimignano, Etruscan and Roman Volterra;

- The island of Elba;

- The village of Montepulciano;

- The Medici Villas and Gardens and the small hilltop town of Arezzo.

Economy

The standard of living is generally higher than the national average though there are certain zonal differences. The rural and mountain areas (Maremma hinterland, countryside around Siena, upper Apennines) are less advantageous than the areas with high industrial concentration and the best communications networks (lower Valdarno, Florence, Lucca, Versilia, Leghorn).

Primary sector

Primary sector

Although its contibution is falling year by year, agriculture still adds significantly to the region’s economy. Tuscany, because of Chianti, is widely known as one of the most prominent wine regions while olive cultivation and vegetable production is worthy of note. Its products have received numerous awards while they are often proteceted under the quality assurance labels DOP/DOC (Protected/Controled Designation of Origin).

Secondary sector

The secondary sector is often characterized as the backbone of the agriculture of Italian industry. Given the abundance of underground resources, the industrial sector is prevailed by mining, though the specific activity has sharply declined compared to a few decades ago. Other activities of the secondary sector include the metallurgical (Piombino, Leghorn, Florence, S. Giovanni Valdarno), engineering (Florence, Pontedera, Pistoia, Arezzo), chemical (Rosignano Solvay, Leghorn), textile (Prato, Florence, Empoli), food (Sansepolcro), printing (Florence), tanning (S. Croce sull'Arno) and glass, making (Empoli) sectors. Craft industries flourish all over this region (faiences, lace, rush-weaving, wrought-iron). Special attention must be drawn on the textile industry prevalent in Prato which is one of the leading centers for luxury fabric manufacture worldwide. Tuscany is home to some of the most world renowned fashion stylists operating in the apparel and leather industries who focus on the export of niche market and luxury products accounting for approximately one quarter of European production. Its turnover is calculated at over €25 billion while it is the third largest supplier of clothing after China and Japan.

Tertiary sector

In the services sector, banking commerce and tourism are of the utmost importance. With regards to tourism Tuscany represents one of the most established touristic markets in Europe and the third most visited region in Italy after Lompardia and Veneto. Most visits in Tuscany are derived from its laid back lifestyle and its “Dolce Vita” way of living which urges all travelers to enjoy the region’s exemplary cuisine, its welcoming climate, its unique architecture and culture and its long history. The main tourist destinations by number of tourist arrivals are Florence, Pisa, Montecatini Terme, Castiglione della Pescaia and Grosseto. Additionally, the Chianti region, Versilia and Val d'Orcia are also internationally renowned and particularly popular spots among travelers.

The rich cultural heritage of Florence from one hand and the idyllic scenery of rolling hills and cypress trees that dominates in the exquisite countryside on the other, has given rise to another important market, that of real estate and has established Tuscany as one of the most prominent second-home markets, especially for overseas buyers who took advantage of the favorable currency rate conditions that were created due to the economic crisis.

Demand for Transient Accommodation

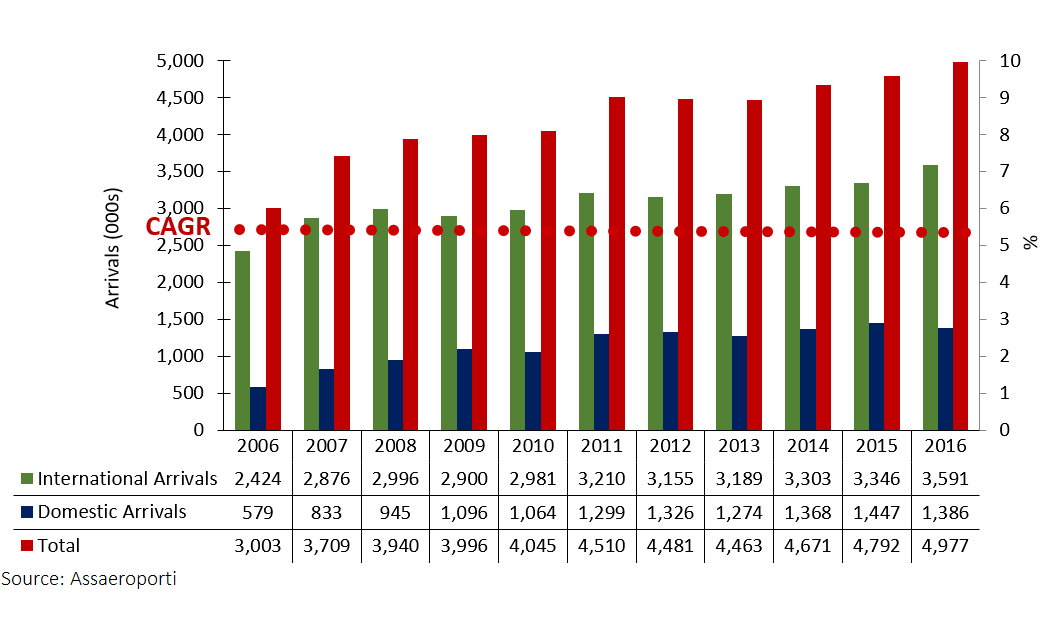

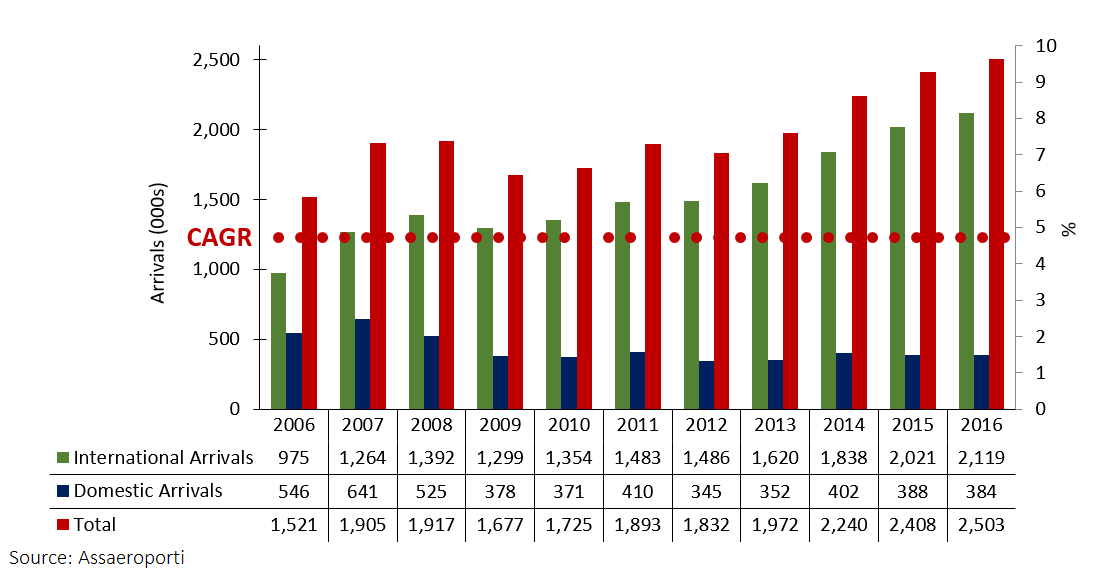

Passenger movements at Tuscany’s two major airports have been increasing at a good pace over the past 12-year period. The Compound Annual Growth Rate (CAGR) for the period was 5.3% for Pisa Airport and 5.1% for Florence Airport, whereas the total number of passengers moving at both airports grew in 2016 by 31.8% when compared to the respective number for 2009 (when a slump in traffic occurred due to the international economic downturn). International movements are more than domestic movements at a roughly 70:30 ratio for 2016 showcasing the international touristic nature of the region.

Toscana Aeroporti S.p.A is the new management company for Florence and Pisa airports. It was created in June 2015 through the merger of Aeroporto di Firenze S.p.A. (the management company of the Florence Amerigo Vespucci airport) and Società Aeroporto Toscano S.p.A. (the management company of the Galileo Galilei airport of Pisa).

The merger between the two companies represents a crucial step towards the creation of a unified Tuscan airport system, in line with what is set forth in the National Airport Programme approved by the Italian Ministry of Transport. The synergy between the two airports, and the dovetailing of the global offer of the system, will make it possible to expand the number of destinations that can be reached and the airlines operating within them, via adaptation of the respective infrastructures.

The long-term targets of Toscana Aeroporti, to achieve by 2029 are: 130 destinations all over the world, 45 airlines and 160 daily flights. The two airports will maintain their specific air traffic specialisation. The Vespucci airport will continue to develop business and leisure traffic through the full-service carriers, linking the main European airports. The Galilei airport will, on the other hand, continue to deal with the tourist traffic managed by low-cost carriers and cargo flights, also focusing on the development of intercontinental flights.

Through the integration of these two companies, Tuscany will be able to rely on one of the most important airport systems in Italy, capable of acting as a driving force for the economic development of one of the best-known and best-loved regions in the world.

Pisa International Airport

FIGURE 1: DOMESTIC AND INTERNATIONAL ARRIVALS 2006-16 (000s)

Florence International Airport

FIGURE 2: DOMESTIC AND INTERNATIONAL ARRIVALS 2006-16 (000s)

Basic Visitation Factors

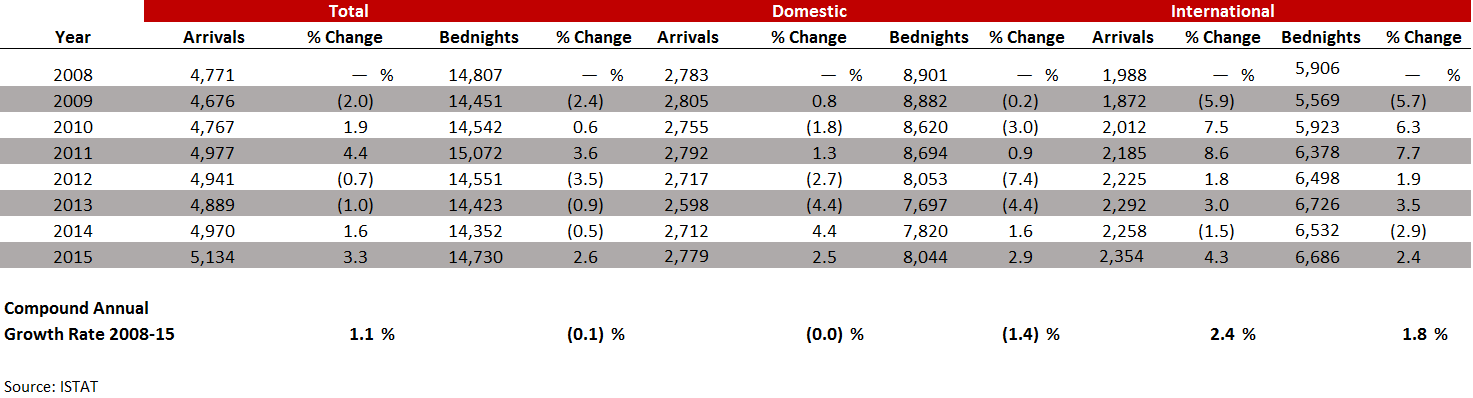

Tuscany is one of the best known and most sought after tourist destinations in the world. With its diverse cultural heritage, landscape, environments and ecosystems, it can meet a wide range of needs and provide a variety of destinations to visitors such as art and historical locations, hills, mountain and beach resort destinations, spa and sport facilities. Today, tourism accounts for more than 10% of regional GDP and Tuscany is one of the areas that have coped better than others with the global economic crisis. Figure 3 depicts domestic and international visitation and accommodated bednights for the wider area of Tuscany’s coutryside for the years 2008-15.

FIGURE 3: ARRIVALS AND ACCOMMODATED BEDNIGHTS IN HOTELS – TUSCANY 2008-15 (000S) (ALL THE REGIONS EXCLUDING THE CITY OF FLORENCE)

It is evident that during the examined period Tuscany’s (the data exlude the city of Florence but include the country side and the sea front destinations) has been visited almost equally both by domestic and international visitors who accounted for an average of 55.0% and 45% of total arrivals respectively. The high number of international visitation to the region and its slow but steady growth can be attributed to the fact that Tuscany is one of Italy's prime summer destinations for international travellers. Overall, the number of total arrivals at hotels in the region has experienced a CAGR of 1.1%. This upward trend was mainly driven by the steady increase in arrivals of international nature and at the same time the stagnation in growth of domestic tourism. During the examined period, international accommodated nights increased in absolute numbers by approximately 800,000 while domestic ones diminished by more than 100,000. The main cause of the stagnation in the performance of domestic tourism is the shrinkage of income that Italian citizens experienced as part of the economic crisis that affected most Mediterranean countries. Moreover, among Italians, Tuscany is considered as a rather expensive destination so they seek to visit alternative places. Nonetheless, during 2014-15, domestic figures in the region witnessed a steady cumulative growth of 7%. Albeit the lack of official data for 2016, press releases indicate an increase by 3% in total arrivals during the past year, an upward trend driven by the increase both in international and domestic arrivals by 3.5% and 2.5% respectively. For 2017, it is expected that tourists number will continue to rise while the percentage growth will be in line with 2016.

Main Source Countries

FIGURE 4: MAIN SOURCE COUNTRIES 2015

Tuscany had always been a popular desination among Americans who ranked first in arrivals for 2015 with almost 700,000 Americans visiting the region representing 7.6% of total arrivals in the region. During 2009-15, arrivals from USA have experienced a CAGR of 5.0% , the third biggest growth rate after China and Brazil with CAGRs of 27.5% and 12.3% respectively. Tuscany is increasingly becoming one of the favorite destinations for new emerging Chinsese social classes while in 2015 the number of Chinese travelers visiting the region almost reached 700,000, closely competing the American travelers. If Chinese tourism growth continued with the same pace in 2016, we expect to see China not only picking up the slack from other countries but also leaving them far behind. Moreover, by considering various factors such as the limited amount of direct flights connecting Italy to China, the inefficient management of the visas, the cultural and operational shortcomings of national and regional promotion have severely limited the incoming flows, the margins for future growth get even more remarkable. Another emerging market that is growing with a remarkable pace but did not manage to enter the top five source countries is that of Brazil with almost 140,000 incoming visitors in 2015. Other nationalities like Germany, France and United Kingdom have traditionally travelled to Tuscany and constitute some of the most significant source countries but given the stability problems in Europe, their growth rate is diminishing year by year.

Seasonality

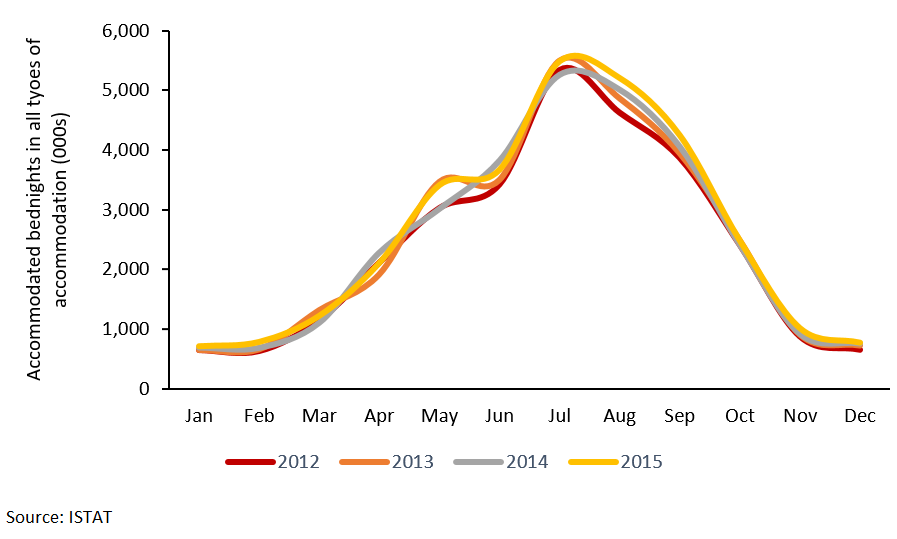

Tuscany displays a typical seasonality pattern for a summer destination (the data exlude the city of Florence but include the country side and the sea front destinations), with high-season extending from May-June to September, shoulder season in April and October, and primarily city destination demand in the remaining months. Most hotels in the region that are situated outside a city have seasonal operations, and usually open in late-March or early-April and close for the season in late October. Recently there have been efforts from some hotels located in the wider region of Tuscany, and especially those in the coutryside that in most cases feature also wineyards into their premises, to expand the operation period by keeping their properties open for business by the end of December and try to take advantage of the influx of visitors arriving in Tuscany to celebrate Christmas holiday.

FIGURE 5: SEASONALITY 2012-15 -TUSCANY

The Significance of the Wine Industry

Wine is believed to have been produced in Italy as far back as recorded history. Being one of the oldest wine regions in the world, it is often referred to as an “old world” wine region, in comparison to regions such as Australia or California that are often referred to as “new world” wine regions. This old-world region is believed to have origins in wine tracing back to between 4,000 and 3,000 B.C.

There are 18 major wine producing regions in Italy and one of them is the region of Tuscany which features one of the most prominent sub-regions, that of Chianti. The region boasts several wine estates spead out from border to border making wine tourism one of the most important experiential activities for visitors, several of who are already characterized as oenophiles touring the area to expand their knowledge on the Italian wine industry. Since the wine business is not considered anymore a niche market, but a commonly used practice to increase revenues, a new model has been established, that of a winery with lodging facilities where new techinques are being implementing to attract and engage all types of tourists mainly by enhancing the local agricultural element while empasis is given on the production and tasting of wine. Some of the most common practices are: weddings which take place in wineries, themed guided tours which peak at the grape harvest season during which visitors enjoy mini courses on viniculture, wellness vacations featuring vinotherapy, spa treatments and thermal baths or the integration of cooking schools inside the wineries were they provide cooking lessons and wine tastings.

The Significance of the Second Home Market

The combination of a timeless charm and a favorable currency rate is what inspires a lot of overseas buyers to acquire a house in the countryside of Tuscany. Being one of the longest-established and best-known places to enjoy a sense of “dolce vita” it has some of the highest-priced country properties in the world. Buyers tend to choose among the following option: restore and old property (commonly referred as Casali) according to their taste and specifications (by keeping the exterior architecture in line with specific regulations), buy one ready-restored or one newly-built. At the same time prices tend to range accordingly; depending on the region and the state of repair they may start from €100,000 for a village house or €250,000 for a good-sized country housed in the mountainous areas north of Lucca and may reach one million for a restored farmhouse located in central Tuscany while in terms of value per m2 ,prices range from €3,500 per m2 to €10,000 per m2 for restored Villas and Casali depending upon the location. Buying a property in Tuscany remains a valuable investment decision as the market is considered to be strong and stable. The reasons for that is firstly the resilience that the specific market demonstrated towards the recent economic turbulence due to its priviliged location and its prestigious lifestyle but also the strict planning laws and architectural regulations enforced by authorities to protect the traditional and authentic character of the region.

Hotel Supply

During 2008-15, although total hotel supply displayed CAGR of -0.4%, total room and total bed supply recorded growth of 0.3% for both categories. This means either that new properties built featured more rooms than the historical average or that a need for expansion of existing properties may has emerged. During the same period, five-star hotels increased significantly to 40 from 24 but it still remains the category with the lowest rate of market share. Four-star hotels also grew in number, whereas a drop was recorded in the number of three-, two-, and one-star hotels. The hotel market outside Florence features properties with relatively low average capacity of only 30 rooms and 65 beds mainly due to the fact that the market is dominated by small familly-owned-and-operated businesses. For 2015 the average five-star hotel featured 58 rooms and 133 beds while the same numbers for a four-star property were 54 and 120 respectively.

Growth in the higher market segments is attributed to the increasing number of guests looking for higher quality services and at the same time to the awareness of the hoteliers that in order to stay competitive they ought to keep their properties in line with the new requirements that have emerged from the growing trend of the luxury segment in the region’s market share. The five-star segment's growth can also be associated to the needs arising from the tourism outflow of affluent travelers from countries with booming economies (e.g. BRIC countries). Despite the growing demand for luxury properties and services the presence of upscale international brands is limited with only a few of them operating hotels. More specifically the only high end international brands who have penetrated Tuscany’s countryside market are: Timbers Hotels and Resort with Castello di Casole, Rosewood Hotels and Resorts with Castiglion del Bosco and Belmond Hotels and Resorts with Villa San Michele. Various other hotels are affiliated with Marketing Consortiums (e.g. il Borro, Castello di Velona and Relais La Suvera, Borgo Santo Pietro with Small Luxury Hotels, Borgo San Felice and Villa Mangiacane with Relais & Chateaux, Castel Monastero and Castello del Nero with Leading Hotels of the World, Castello Banfi il Borgo with Tablet Hotels). Tuscan hotel industry did not suffer greatly during the crisis. Nonetheless it displayed a similar picture to other destinations, registering a supply fall from 2012 to 2013 – it is generally accepted the Italian crisis reached a peak in 2012.

FIGURE 6: HOTEL SUPPLY – TUSCANY 2008-15 (EXCLUDING THE CITY OF FLORENCE)

.png)

New Supply for high end properties

Toscana Resort Castelfalfi has just announced the opening a new 120-room five-star hotel. It is the newest five-star hotel being developed in Tuscany and will be built on the 1,092 hectare estate in Tuscany, located in an 800- year old Medieval village. The new five-star property is owned and managed by TUI AG, a multinational travel and tourism company which invested €23.5 million in the hotel that is also affiliated with Preferred Hotels and Resorts.

Rosewood Castiglion del Bosco has granted the permits to further expand the Hotel by almost double its size (currently featuring 23 suites). The project is in its early development is expected to be concluded in 2019.

Various other projects are in the process of obtaining the permits for development or construction of high-end resorts but no official announcement has been made yet.

High-end Hotels Performance

Figure 7 summarises the important operating characteristics of a sample of high-end hotels in the broader region of Tuscany’s countryside with a focus on the following zone (Pisa, Siena and Firenze). The chart sets out the average occupancy, average room rate, and rooms revenue per available room (RevPAR) for a sample of 13 major upscale hotel properties representing in total 434 hotel rooms. For consistency reasons, despite the seasonal operation of the specific hotels (with a seasonal occupancy from April to October of approximately 65%) all occupancy percentages refer to 365 days of operation.

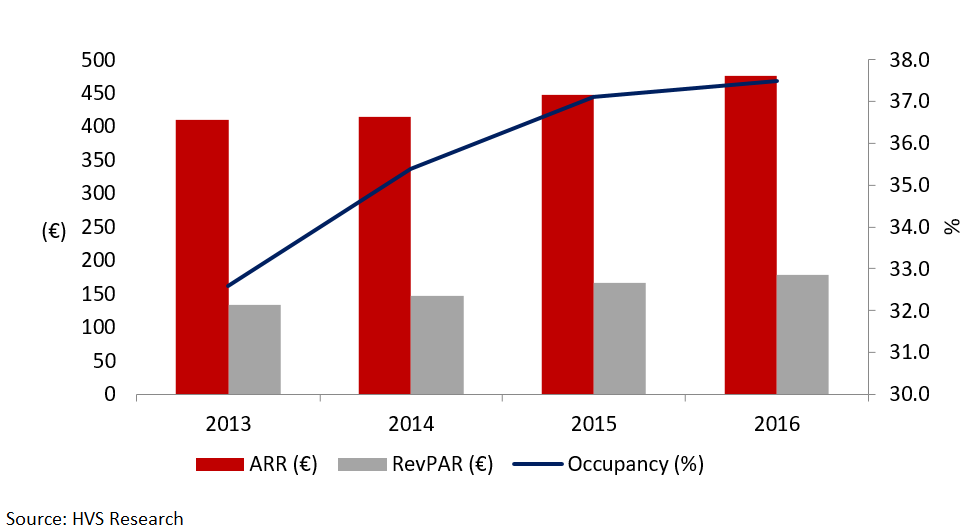

FIGURE 7: HOTEL PERFORMANCE – TUSCANY’S COUNTRYSIDE 2013-16

Performance of the selected hotels in Tuscany throughout the examined period is showcasing a constant improvement. During the last four years occupancy and average rate witnessed a CAGR of 5% respectively leading to cumulative increase of the RevPAR by 33.3%. This phenomenon could be attibuted to the fact that, given the region’s cosmopolitan character, executives are pushing for higher rates while at the same time occupancy is increasing as Tuscany gets introduced to new markets. The limited new additions to current supply also helps existing properties to achieve higher occupancy levels. Nonetheless, the region lacks a significant number of international hotel brands which could boost its upscale profile and recognition, thus leading to even higher levels of sales efficience and operating performance.

Conclusion

Tuscany’s coutryside is clearly a popular tourist destination because of its abundance in historical sightseeings, cultural attractions, art exhibits as well as many experiential activities. Local authorities, investors, tourism organizations and its citizens have managed to preserve througout the years the region’s unique character, irrextricably connected to the landscape, the notion of “well-being”, the natural resources and the history. Elegant yet authentic it attracts all sorts of leisure travellers from all over the world. By focusing on localhood, tourism professionals add value to the visitor’s journey resulting in making them feel as temporary residents and achieving an unconditional engagement. This is the reason most of the visitors in Tuscany’s countryside would consider it as the ideal second-home destination and consequently real estate market is booming. The region is currently constrained by its seasonality, which is a seven-month period that experiences a high-point in August. Albeit one of the most sought-after destinations for high-spending tourists there is almost trivial presence of international hotel brands mainly because of the difficulties facing in their effort to obtain necessary licenses and permits. Increased demand from the USA and BRIC, are expected to have a positive impact on international visitation to the area. For more information on Tuscany’s market, please contact: Ezio Poinelli: Senior Director HVS [email protected] Paolo Buffa Manager HVS [email protected]