By Anne R. Lloyd-Jones

Supply growth has been the dominant headline for the New York City lodging market over the past decade. The number of hotel rooms in the city increased from 66,000 in 2007 to 99,000 in 2018, a 50% increase in inventory. Another 15,000 rooms are under construction or proposed; if all of these rooms are built, the city’s inventory will have increased by 75% in a 16-year period. Increases in demand kept pace with supply growth through 2018. However, in the first quarter of 2019, supply outpaced demand for the first time in the current cycle. While there are a number of factors that influenced these results, it is clear that the supply side of the equation is putting increasing pressure on the lodging market. This is evident in recent average rate trends, which illustrate sluggish ADR growth since 2010, including three years of actual declines.

There is good news with respect to supply. In addition to rising construction costs and decreasing availability of construction financing, several recent developments in the city are expected to curtail the net supply growth in the market.

Changes to M1 Zoning

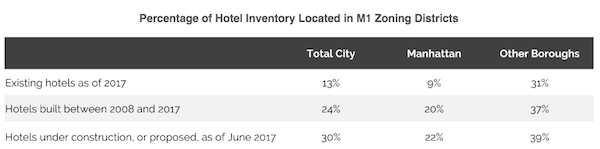

In December 2018, the City adopted a text amendment to the M1 zoning district regulations, as a result of which hotel development in M1 districts now requires a special-use permit. Prior to this change, hotels had been an as-of-right use in M1 districts. This change is anticipated to have a significant impact on the development of new hotels in the city, as the M1 district has realized a disproportionately high concentration of new hotel development over the past ten years. The following table illustrates the proportion of hotel uses in M1 zoned areas.

The M1 Light Manufacturing District is designated for areas with light industry, a wide range of manufacturing, and other industrial, commercial, and community facility uses. The M1 district is further divided between six subdistricts; permitted FAR is the principal differentiation between these districts. The M 1-6 district, which permits FAR of 10.0 (and up to 12.0 with a public plaza), is primarily found in central Manhattan, in areas where multi-story manufacturing originally developed. This includes the Garment District and areas of the Chelsea and Midtown South neighborhoods, all of which have a high concentration of sites zoned M1-6. Other significant concentrations of M1 zoning are found in the outer boroughs, with the largest concentration in Queens, including Long Island City and areas around the airports. Most of these areas are zoned M1-3, M1-4, and M1-5 and, thus, feature lower permitted FARs but are also characterized by lower land costs and more available sites.

The M1 district has been targeted by hotel developers because hotels usually represent the highest and best use of the land. Hotels can be constructed on sites with relatively small footprints and still take advantage of the full permitted FAR, as the site and setback requirements permit tower construction. Most other permitted uses in the M1 district require a larger footprint, which can necessitate assemblage of multiple sites and higher site costs. In addition, most of these uses are not compatible with high-rise construction and, thus, are not able to use the full FAR. Finally, there are no parking requirements in the M1-4, M1-5, and M1-6 districts, which further enhances the feasibility of hotel projects in these areas.

The proliferation of hotel developments in the above-noted neighborhoods illustrates the influence of these circumstances. Also contributing to this trend is the dearth of sites that are both zoned and suitable for hotel development, which is particularly true in Manhattan. The limited availability of vacant, affordable land in the primary commercial districts has led developers to seek out alternate locations, resulting in the high proportion of hotel developments in M1 districts.

The impetus behind the text amendment was concern that hotel developments are changing the character of the neighborhoods in which they are located, causing the displacement of traditional light-industrial uses and pre-empting development of new light-industrial projects. Other permitted commercial uses have also been affected, resulting in a decline in commercial uses that support the businesses in the district, as well as the residents of adjacent, residentially zoned districts. City documents also note the incompatibility of high-rise hotel buildings with the surrounding areas, which in most cases feature low- or mid-rise buildings.

The text amendment was adopted in December 2018, and hotels are no longer a permitted use as-of-right in most M1 zones; the exceptions are certain areas by LaGuardia and JFK airports, as well as areas where a special permit was already required for hotel development. As a result of the text amendment, the lot area where hotels are permitted as-of-right has been reduced by 45%, and the as-of-right permitted FAR decreased by 25%, according to data published by the City. Hotel development is still an option within M1 districts, but now requires a special-use permit from the City Planning Commission (CPC). Obtaining this permit requires developers to comply with a site-specific review process, which is time consuming and can be expensive. The time and costs associated with obtaining a special-use permit, as well as the potential that the project will not be permitted, is expected to be a significant deterrent to the pace of hotel development in these areas.

Expiration of Local Law 50

Enacted in 2015, Local Law 50 prohibited the conversion of hotels with more than 150 rooms to alternate uses. The original two-year term of the law was extended for a second two-year period in 2017, but with no further extension, the regulation expired in June 2019. Under this law, owners of large hotels could convert 20% of their inventory to another use, but the requirement to retain 80% of a property’s inventory for hotel use effectively eliminated the redevelopment alternative for most properties.

Prior to 2015, the market had experienced some decreases in supply as hotels were taken out of service, either for conversion to an alternate use or for demolition to permit new construction. In most instances, the properties were converted to residential use, as was the case with two of the most high-profile conversions—the Plaza and the Waldorf Astoria Towers. By replacing the hotel units with residential condominiums, ownership was able to recover its investment through the sale of the residential units, usually fairly quickly. Such conversions also have the advantage of eliminating the often-significant operating costs associated with a hotel; this benefit is particularly compelling for properties with the high labor costs typically associated with union contracts, including those with large food and beverage operations.

With the expiration of Local Law 50, hotel owners now have the option to convert their property to an alternate use. It is difficult to know how soon, or how many, properties will take advantage of this option. There are some projects already in the works; for example, the 1,300-room Grand Hyatt New York is scheduled to be demolished and will be replaced with a two-million-square-foot, mixed-use complex, including office and retail space, as well as a smaller hotel. Other projects will no doubt follow, although given the current soft conditions in the higher end of the condo market, the economic advantages of residential conversions are not as compelling as they were when the law was enacted in 2015. Ultimately, the removal of existing inventory will help to offset the increases in supply resulting from new construction. This trend should help to stabilize the market and support ADR growth.

National Trends

In addition to the above-discussed factors, hotel development in New York City is also being affected by two influential trends that are affecting the industry on a national basis.

Rising Construction Costs: According to the Turner Building Cost index, construction costs have risen steadily since 2011. Between 2013 and 2016, costs increased by an average of 4.5% per year, rising to 5.0% in 2017 and 5.6% in 2018. As a result of these cost escalations, a hotel that cost $100,000 per room to construct in 2012 would now cost $132,000 per room, all other things being equal.

The cost escalations of the past eight years predate the tariffs imposed on China in 2019, which include a 25% tariff on steel and a 10% tariff on aluminum. As China is one of the primary sources of these key construction materials, construction costs in the U.S. will be affected. In addition, the tight labor market has made it increasingly difficult to find both skilled and non-skilled workers, which has resulted in rising labor costs. Given these conditions, construction costs are expected to increase at an accelerating pace. With RevPAR growth now expected to be in the 1.5% to 2.0% range over the next two years, the feasibility of new construction will be increasingly difficult to support.

A recent HVS assignment in a major urban market demonstrates this dynamic. At the time of the original feasibility study, the construction cost, including site work and FF&E but excluding soft costs and land, was roughly $125,000 per room. Three years later, the costs had increased to $175,000 per room, a 40% increase. Over that same period, RevPAR in the market increased only 13%. The disparity between cost increases and revenue growth caused the IRR to drop from about 11% to roughly 7%, a level that is below the threshold considered acceptable for most investors. It is these metrics that will ultimately cause the pace of supply increases to slow. As always, project feasibility will vary from market to market and project to project, but in terms of national trends, the pace of new hotel development can be expected to decline as costs continue to rise.

Limited Construction Financing: Industry sources have reported decreased availability of construction financing. Construction financing has historically been the hardest loan to secure, with fewer lenders active in this space than in the traditional debt markets. In response to sluggish revenue growth and concerns about over-supply, many lenders have taken an increasingly cautious view of new hotel projects, and some have left the market altogether. The difficulty in obtaining construction loans, coupled with sometimes higher lending costs, has made executing new deals increasingly difficult. Again, these circumstances vary based on the project and location, but, overall, the decreased availability of construction financing can be expected to result in a decline in the volume of new supply.

A Note on Airbnb

New York City is reportedly Airbnb’s single largest market, with roughly 50,000 units listed in inventory. While the degree of competitive interaction between hotels and Airbnb units can be debated, it seems clear that the proliferation of Airbnb units, and particularly entire units in multi-unit, residential settings, has contributed to the competitive pressures on the market. There is good news on this front. New York City recently entered into an agreement with Airbnb, whereby the Mayor’s Office of Special Enforcement (OSE) will receive data on Airbnb listings and usage. The data will enable the OSE to identify and act against illegal short-term rentals (city law prohibits the rental of an entire apartment for less than 30 days, unless the owner is present). The OSE has already raided several illegal rental units and has stated it will continue to do so. The City has identified two primary goals in pursuing a crackdown on illegal short-term rentals. The first is to ensure that the city’s housing inventory remains available for full-time residents, a critical issue in a tight housing market. The second is to address safety and security concerns about transient usage of unregulated buildings; these concerns consider both the guests of the short-term rentals and other tenants in the buildings. While neither goal speaks directly to the lodging industry, the industry will benefit from the stricter enforcement of the short-term rental laws made possible by the new agreement.

Conclusion

Supply has been the predominant theme in the New York City lodging market for the past decade. The rapid increase in supply was facilitated by the availability of sites in the M1 district, which were the target of a disproportionate amount of new development. The prohibition on converting larger hotels to alternate uses imposed artificial constraints on owners and limited the natural “aging out” of existing hotels that no longer represent the highest and best use of the property. With these constraints removed, and the availability of sites entitled for hotel development as-of-right significantly reduced, the net increase in inventory should begin to decline. Adding to these New York City-specific factors are the rapid increases in construction costs and decreased availability of construction financing. The combination of these influences should result in a much more moderate pace of supply growth in the city over the next five years, which can be expected to benefit the market in terms of occupancy, average rate, and RevPAR.