By Jerod Byrd

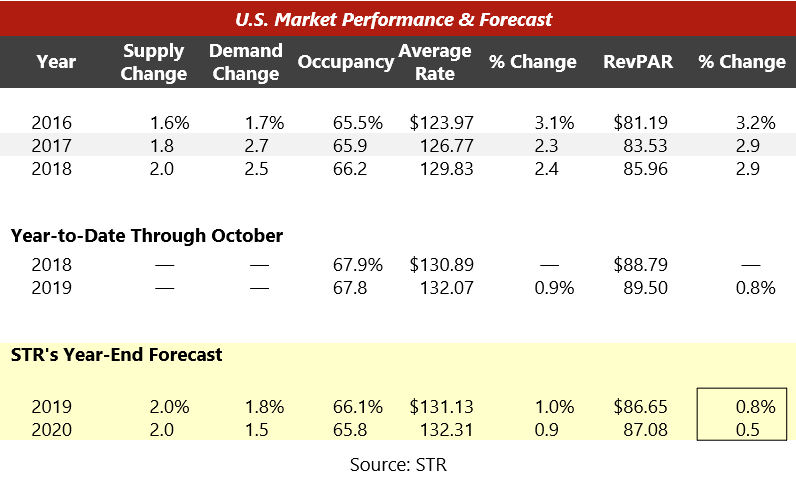

Occupancy levels across the U.S. remained generally stable through October 2019, while ADR registered a marginal increase of less than 1%. Research suggests that RevPAR will end 2019 below the 1% mark; this represents a further year-over-year deceleration in RevPAR, which has been the general trend since 2015. The continued entrance of new supply and the slowdown in job growth are the primary factors contributing to the recent trend. Supply is anticipated to continue to increase by nearly 2% in 2020, which will likely outpace demand growth. While RevPAR is projected to remain positive in 2020, the decelerating growth trend is expected to continue and drive fear among hoteliers in the near future.

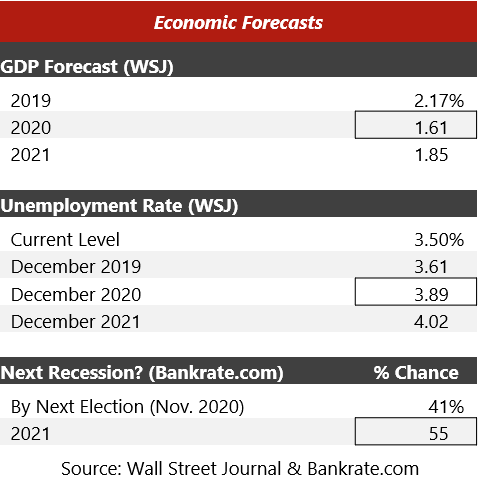

In terms of economic growth, many analysts are predicting the second half of 2020 to be more challenging given the job growth deceleration, recent yield-curve indicators, and dip in consumer and business confidence. According to the BLS, job growth has averaged 167,000 per month thus far in 2019, compared with an average monthly gain of 223,000 in 2018. According to Bankrate.com, 41% of industry participants anticipate the next recession to occur by late 2020, while 55% expect a recession the following year. Nonetheless, despite an anticipated decline in GDP in the near term, the unemployment levels over the next couple years should remain healthy, as forecast, increasing only slightly above the current national rate of 3.5%.

From a profit perspective, expect a continued downward trend through 2020. While the lending appetite is still healthy for hotels, lenders for new construction are requiring more equity to move a project forward than in recent years. Equity yields and cap rates are anticipated to weaken slightly in the near term, particularly as employment growth continues to slow; however, changes to monetary policy, such as the recent rate cut by the Fed in October should help buffer some of the negative effects of the imminent slowdown.