By Rod Clough

With contributions from Eric Guerrero, Josh Williams, Neil Flavin, Zabada Abouelhana, James Rebullida, and Aleisha Smith

Harry Javer and team executed another stellar Lodging Conference at the beautiful JW Marriott Desert Ridge, where over 2,700 attendees gathered to ponder and map the future of our great industry. We were thankful to sponsor such an important meeting, and I was honored to take the main stage at its start to share my perspectives on the direction of cap rates, discount rates, and values. Here are our takeaways from the conference:

- There is a notable disconnect at present between buyer and seller price expectations, with predictions that more sellers will work to meet the market in the coming months and year. Recent select-service hotel deals have closed in the 8.5% to 9.25% cap rate range, with limited-service trending higher and full-service trending a bit lower. Sellers may need to recalibrate into this range during their price discovery journey for stabilized assets. Buyers are taking into consideration high-cost PIPs, increasing expenses (such as insurance, property taxes, and labor), and adjusted, lower year-one NOIs (when priced with higher cap rates), and these may not match seller expectations, which may be based on T12 considerations, as well as cap rates that do not reflect up-to-the-minute trends.

- Cash is king, and well-capitalized buyers are winning deals because they can offer quick closing/short due diligence contingency offers. Creative financing (seller financing, seller carry, seller-preferred equity) may also be an option to get a deal done given the high cost of traditional debt at this time. A few lending sources are focusing on providing short-term, second-position loans to help bridge the gap or fund PIP investments. This money is being offered at interest rates in the mid-to-high teens.

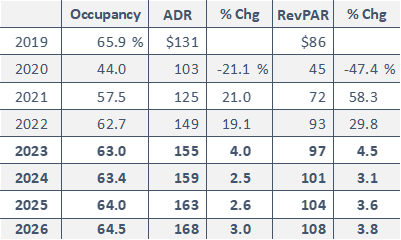

- There’s still an appetite for lenders (including private equity firms) to finance deals; they just have to be for financially strong buyers with a good global cash-flow on all assets owned. Concerns looming over industry forecasts include interest rates not expected to drop anytime soon, the upcoming election year, and the potential recession (however shallow it may be). We recently published our latest forecast and macro market overview, as shown below—read Anne Lloyd-Jones and McKenna Luke’s article here for more insight.Recent National Metrics and Latest HVS Forecast

Source: STR (Historical), HVS (Forecast)

- PIPs are now more expensive than they were pre-COVID. For example, a full renovation PIP for a Hampton by Hilton was recently quoted in the $35k- to $40k-per-key range, whereas pre-COVID, the same scope of work would have been $25k per key.

- Developers are still actively working on new ground-up developments. If you can build, build now while others can’t. When the dust settles, those who pushed through during difficult times will have the newest assets that will be fully stabilized when others start playing catch-up. Of course, the challenge has been obtaining debt (fewer lenders are keen on hotel constructions loans) and rising construction costs. A developer mentioned that their construction costs for a premium-branded convention center hotel increased 20% compared to their original budget pre-COVID. They had to reduce key counts or amenity offerings to lower costs.

- Hotel developers today are also making exciting advancements in the sustainability arena, with innovations implemented in both back-of-house and front-of-house areas. Hotel design also needs to consider the new generation of traveler that is combining business travel with leisure travel. New spaces need to address both larger public meeting needs and smaller, more intimate business needs for travelers and teams, as well as extended-stay travel that includes multi-generational families. Innovations in adjoining rooms, bunk rooms, and social spaces for groups and families to gather should be thoughtfully integrated.

Luigi Major will be speaking at the upcoming Latino Hotel Association Conference, which takes place at the Hilton in Southlake, TX on October 11 and 12. With his presentation and others, we look forward to continuing the conversation about the future of our industry. If you would like a private presentation of our latest thoughts and industry forecasts for your firm, please contact me to schedule a meeting.