By Larissa Lam and Daniel J Voellm

How will Brexit affect UK Tourism?

For several years, the term Brexit has become a household name in not only countries in Europe but also countries around the world, being the withdrawal of the United Kingdom from the European Union. In 2012, UK Prime Minister David Cameron rejected calls for a referendum on membership in the European Union. However, he did not rule out a referendum happening in the near future. Fast forward to 24 June 2016, the people in the UK gathered and voted after a heavily publicised and contested pre-referendum period by both the ‘Leave’ and ‘Stay’ camps. In the end, 48.1% of those who voted preferred to stay and 51.9% preferred to leave. The vote was largely split by the greater London area and Scotland being in favour of ‘Stay’, whereas most other parts of the UK voted in favor of ‘Leave’.

No FX: The British Pound pressured by Brexit

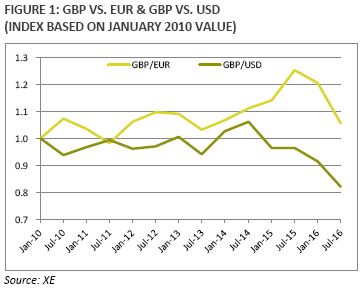

Nowadays, currencies often reflect the health and prospective outlook of countries’ economies. Favorable forecasts yield currency value increments and adverse ones lead to value declines. With voters supporting a Brexit, the UK is on course for major changes and a significant amount of uncertainty surrounding future economic prowess. No matter the duration of the actual Brexit negotiations, there will be a decrease in political and economic stability. As shown in Figure 1, the British Pound (GBP) dropped in value against key global currencies since the vote on June 24 and its value will likely remain low until the UK will be able to shed a light on a (bright) future path.

Nowadays, currencies often reflect the health and prospective outlook of countries’ economies. Favorable forecasts yield currency value increments and adverse ones lead to value declines. With voters supporting a Brexit, the UK is on course for major changes and a significant amount of uncertainty surrounding future economic prowess. No matter the duration of the actual Brexit negotiations, there will be a decrease in political and economic stability. As shown in Figure 1, the British Pound (GBP) dropped in value against key global currencies since the vote on June 24 and its value will likely remain low until the UK will be able to shed a light on a (bright) future path.

Foreign travellers will likely capture this opportunity to visit London and other popular destinations in the UK. Conversely outbound travel will be impacted, certainly among more value oriented travellers that constitute a large share of the European travel market. How about Asia Pacific?

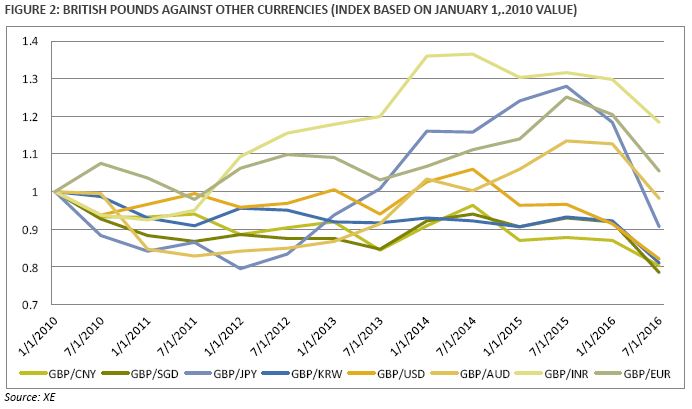

As shown in Figure 2, the British Pound’s value weakened against key Asian currencies. From June 1, 2016 and July 1, 2016, the British Pound dropped against the Chinese Yuan, Euro, United State Dollar, Indian Rupee, Singapore Dollar, Australian Dollar, Korean Won, and Japanese Yen ranging from 6.4% to 13.6%.

Given the movements of individual currencies, the effect was amplified and most severe against the Japanese Yen at a 23.5% drop over a six month period. While foreigners travelling to the UK may rejoice at the value decline of the British Pounds, natives may need to reconsider their outbound travel plans to other countries. The weakening of the British Pounds against other currencies may negatively impact British outbound travel in the future, especially to Asian countries which are relentlessly developing.

Brexit and Tourism

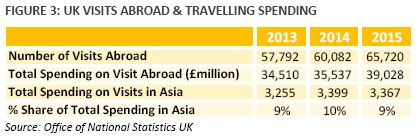

Tourism is an important factor of an economy’s welfare, be it inbound or outbound travels. In 2015, the UK outbound travel market was worth more than GBP39 billion for 65.7 million visits. Asia welcomes about 5% of those travellers and represents around 9.0% of the spending, largely due to the cost of airfare.

Tourism is an important factor of an economy’s welfare, be it inbound or outbound travels. In 2015, the UK outbound travel market was worth more than GBP39 billion for 65.7 million visits. Asia welcomes about 5% of those travellers and represents around 9.0% of the spending, largely due to the cost of airfare.

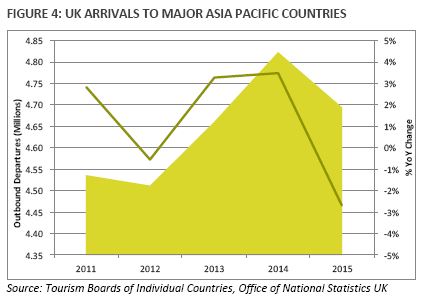

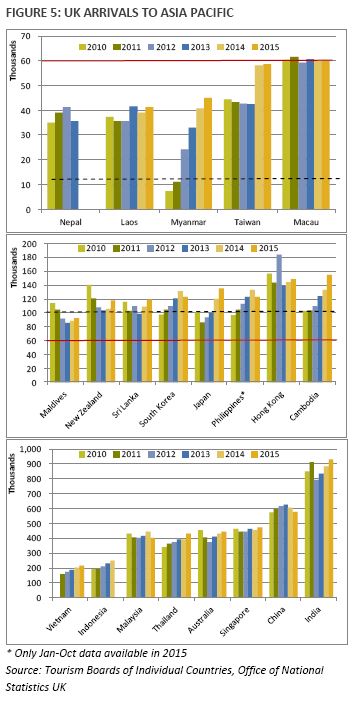

From 2011 to 2014, the UK experienced a steady growth of outbound tourists travelling to major countries in Asia¹. In those five years, visitor arrivals achieved 4.8 million in 2014. When the uncertainties of Britain’s future began to daunt on its people in 2015, some have refrained from travelling.

The decrease of 1.9% in YoY change in 2015 demonstrated signs of worry and insecurity. Officials recorded 91,000 fewer outbound travellers to Asia. However, the top five destinations for the British travellers maintained strong performance in 2015. With the exception of Mainland China, positive YoY increases were recorded in India, Singapore, Australia, and Thailand. Among the five, Thailand achieved the highest YoY growth of 10.2% with 432,000 British arrivals 2015.

The decrease of 1.9% in YoY change in 2015 demonstrated signs of worry and insecurity. Officials recorded 91,000 fewer outbound travellers to Asia. However, the top five destinations for the British travellers maintained strong performance in 2015. With the exception of Mainland China, positive YoY increases were recorded in India, Singapore, Australia, and Thailand. Among the five, Thailand achieved the highest YoY growth of 10.2% with 432,000 British arrivals 2015.

Which Markets are most likely to feel the Pinch?

Which Markets are most likely to feel the Pinch?

For foreigners, Asia seems to exert a gravitational pull, constantly attracting travellers from across the globe. Tourism demand has evolved in both corporate and leisure segments. Destinations such as China, India, Hong Kong, and Singapore have long been welcoming British visitors for business. While some markets have established their share in the British outbound leisure market, many other Asian countries have just started to develop their respective economies and tourism for foreigners to capture both business and leisure demand. Britain remained a bright spot for outbound European demand as the continent suffered from a depreciated Euro and general economic woes after the Global Financial Crises (see Greece, Spain, and Italy). India and Mainland China have been benefitting from a significant number of British inbound arrivals for quite some time. Of the above countries, British visitors account for the largest share of total visitor arrivals at 11.6% in 2015 in India. Following a volatile period, India welcomed a record 931,000 British visitors, posting a 4.5% Year-on-Year growth in 2015. Despite the decline of arrivals compared to that of 2014, more than half a million British visited China in 2015. Principal growth destinations since 2010 include first and foremost Thailand, but also Indonesia and Vietnam. At a smaller scale, Cambodia, Philippines, Japan, South Korea and Myanmar also registered positive trends.

Figure 6 illustrates the percentage share of UK visitor arrivals of each destination’s total. Not surprisingly India and Sri Lanka rank high given the share of overseas Indians visiting relatives and friends. Similarly Australia and New Zealand register relatively large shares. However, Maldives likely faces the largest downside risk. Although luxury demand tends to be more price inelastic, the Maldives has become an aspirational destination which attracts not only luxury travellers, but ‘once in a lifetime’ visitors. Another set of destinations that could feel a significant impact are those where UK tourists might not represent a high share, but rank high in terms of spending power. This would be the case for Myanmar, Vietnam, Indonesia and Thailand. Driving average rate in those ‘at risk’ destinations might become a challenge as the exchange rate driven UK tourist stays at home, travels within Europe or opts for shorter itineraries.

Figure 6 illustrates the percentage share of UK visitor arrivals of each destination’s total. Not surprisingly India and Sri Lanka rank high given the share of overseas Indians visiting relatives and friends. Similarly Australia and New Zealand register relatively large shares. However, Maldives likely faces the largest downside risk. Although luxury demand tends to be more price inelastic, the Maldives has become an aspirational destination which attracts not only luxury travellers, but ‘once in a lifetime’ visitors. Another set of destinations that could feel a significant impact are those where UK tourists might not represent a high share, but rank high in terms of spending power. This would be the case for Myanmar, Vietnam, Indonesia and Thailand. Driving average rate in those ‘at risk’ destinations might become a challenge as the exchange rate driven UK tourist stays at home, travels within Europe or opts for shorter itineraries.

Conclusion

For many years, residents in the UK have enjoyed very strong spending power overseas. The strength of the British Pound opened up destinations further afield to a broader part of the population. Following the devaluation, the share of people able to maintain this lifestyle is likely set to decrease. In addition, tourism spending might be redirected to destinations easier on the wallet.

Asia has been a popular destination for UK travellers, mostly for its tourism resources, such as beaches and cultural heritage, but also a general affordability at a high standard of hospitality. Likely a number of hotel markets in destinations such as Maldives, Thailand, Myanmar, Vietnam and Indonesia will feel and impact. FIT demand will be slower to pick up and agents show greater price sensitivity.

Operators have three options: do nothing, wait until the British Pound regains strength or focus more heavily on that smaller pie. After all, higher-spending guests that utilize the facilities and outlets are what every hotelier is yearning for.

¹ Major countries in Asia include Australia, Cambodia, China, Hong Kong, India, Indonesia, Japan, Laos, Macau, Malaysia, Maldives, Myanmar, Nepal, New Zealand, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, and Vietnam.