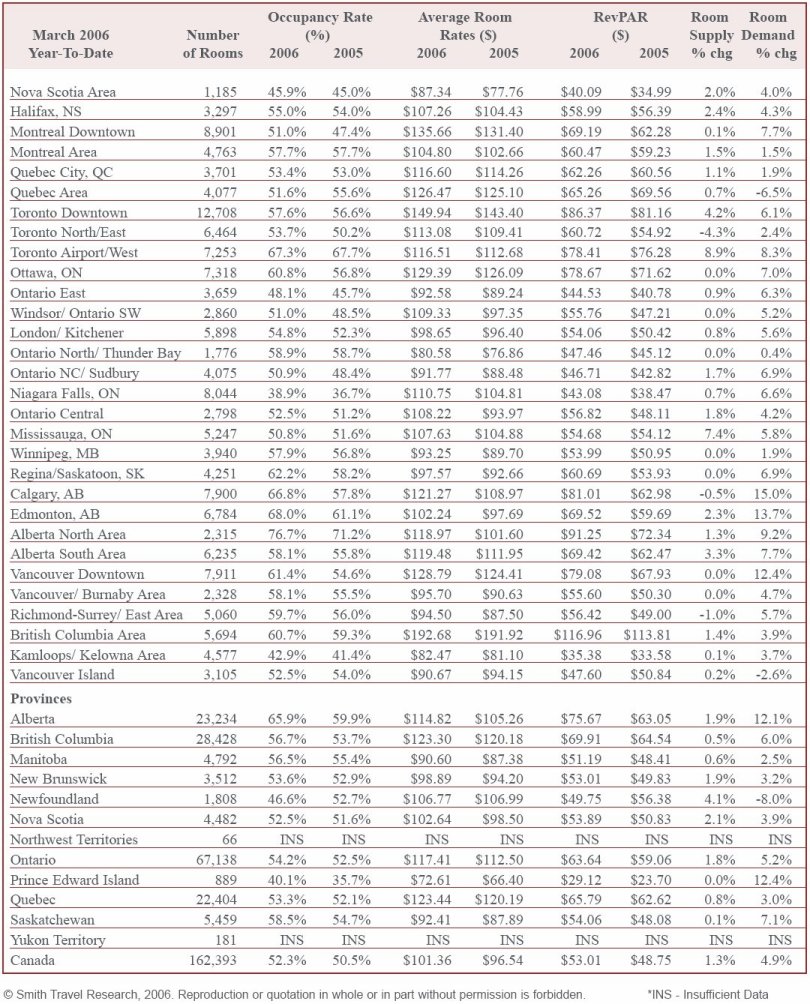

| Reprint From 1997 HVS Newsletter By: Betsy

MacDonald, MAI, AACI and Steve Rushmore, CRE, MAI, CHA.

Hotel feasibility, market demand studies, valuations, and appraisals have long been used by lodging developers and owners to justify new projects and expansions of existing properties. Both mortgage lenders and equity investors rely on these reports to direct millions of dollars. For the most part, feasibility studies, market demand studies, and appraisals are well researched and professionally prepared. However, occasionally studies and appraisals are issued which may be termed a �stretch,� or one that employs certain unusually aggressive assumptions to either render an unfeasible project marginally feasible, or a marginally feasible project more feasible. The feasibility of a hotel development is based on its anticipated income generating capability, or a forecast of income and expenses. Any assumptions which tend to overstate revenue and/or understate expenses will make a project more economically viable or feasible, or provide a higher value. Since opening in Canada, HVS International has been requested to review numerous feasibility studies, valuations, and appraisals prepared by other firms. Based on these reviews, we have developed an awareness of potential areas where aggressive assumptions are sometimes employed to make a proposed hotel project more feasible, or give a higher value to an existing property. One of the most obvious problem areas is overstating competitive hotel room night demand. A room night demand analysis is a process by which market demand is estimated by totalling the number of occupied hotel rooms within a market area and forecasting future changes to this level of demand. Any overstatement of the existing demand or the expected demand growth rate tends to inflate area occupancy levels and increase market potential for any proposed new lodging properties, or existing properties. Aggressive feasibility firms will often go outside primary market areas and pad the base level of demand by including more existing properties in the competitive supply than would normally be considered competitive with the proposed or subject property. They may also overstate the annual percentage growth rate of room night demand. For an example, consider a primary market area that has five properties totalling 1,250 guestrooms. The area occupancy is 75%. Current room night demand is calculated as follows: 1,250 guestroom x 75% occupancy x 365 days/year

=

Now the feasibility firm wants to be aggressive and enlarges the primary market area to include in its base eight hotels with 2,500 guestrooms, operating at an average occupancy of, say, 71%. Current room night demand in this instance would be: 2,500 guestroom x 71% occupancy x 365 days/year

=

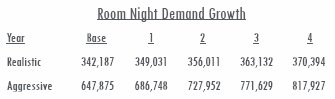

An analysis of the area�s room night demand growth

rate shows a 2% compounded annual increase to be reasonable. An aggressive

firm might contend that a 6% growth rate is justified. Applying the 2%

growth rate to the realistic base demand and the 6% to the aggressive base

demand results in the four-year room night demand estimate shown in the

table below.

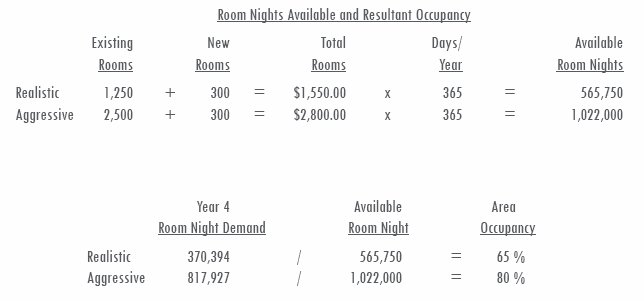

Now, assume that the feasibility firm is evaluating a new 300-room hotel for the area. The calculation in the table at the top of page two shows the impact of a 300-room hotel in the area occupancy when it enters the market in year four. Under the realistic assumptions, the area occupancy declines from its current level of 75% to 65%. Under aggressive assumptions, the area occupancy actually increases from 71% to 80%. .  These two minor points - definition of market area and estimate of demand growth rates - can make a marginal property appear successful. Now, where we see appraisers fail in this area, is when they stabilize a hotel�s occupancy, and they have taken no consideration into additional new supply coming into a market. This can be for either an existing hotel, or a proposed hotel. Some appraisers just apply a capitalization rate to the stabilized net income, and take absolutely no consideration to the start up years of operation which commonly have a lower occupancy and average room rate, or the fact that a new 500-room hotel is about to open and a 600-room hotel is proposed. These events are most likely going to affect a hotel�s achievable occupancy and average room rate, and should definitely to be considered by an appraiser. The same can be done with a hotel�s average room rate. One of the leading problems we see with hotel appraisals, is that appraisers do not know the difference between rack rate (that quoted by the hotel at the front desk or through the reservations department), and the average room rate. The rack rates are invariably higher than the average room rate, which blends all the rates including discounted rates. A hotel appraiser who only looks at the rack rates, and states that a subject hotel or a proposed hotel can achieve an average room rate in the range of the stated or quoted rack rates, is definitely overstating potential income. This, of course, overstates the value. Most hotel feasibility firms know the difference between average room rates and rack room rates. However, these firms may again overstate the market average room rate by increasing the competitive rooms supply base, or by including hotels that are not really competitive but achieve higher room rates. Lets assume that our five hotels are a Holiday Inn, Ramada Inn, Clarion Inn, Best Western, and a Delta Hotel, running an average occupancy of 75% with an average room rate of $80. Now we increase our competitive supply and add a Four Seasons, a Westin, and a Canadian Pacific Hotel. These hotels bring market occupancy down to 71%, but increase the average room rate to $105. If the feasibility firm selects an average room rate below the market average, lets assume $95, this would appear reasonable. However, when the primary competitive hotels are only averaging $80, the estimated $95 average rate may be the highest of the primary competitive hotels. We are always cautious of a proposed hotel which is expected to achieve an average room rate above the highest competitor is the market. This will not always be evident in a feasibility report, because they tend to only give averages, and never reveal actual numbers for specific properties. Therefore, lenders and investors are not aware that the proposed hotel is expected to achieve the highest average room rate in the primary competitive field. The inflation on the average room rate can also

have a significant impact on a hotel�s feasibility or value. Let�s assume

that a realistic average room rate is $78 with an average growth rate of

2% annually for four years. Now, assume the aggressive feasibility study

firm or appraiser uses the $95 average room rate with a 5% inflationary

growth factor. The following table summarizes the effects of these seemingly

slight differences in the assumptions.

As previously stated, an overstatement of revenue may lead to a more feasible project, or a higher value. Some feasibility and appraisal firms obtain revenue estimates from national averages, without knowledge of the facilities included in those averages. For example, food and beverage revenue achievable by a hotel with 30,000 square feet of meeting space should not be comparable to a hotel with only 5,000 square feet of meeting space. Revenue achievable at the facility with the larger facilities will most likely not be achievable by the smaller facility. Understated expenses occur when an appraiser or a feasibility firm do not take into consideration that most operating expenses are both fixed and variable. At lower occupancies, in the start up years, expenses are commonly higher as a percentage of sales than at a stabilized occupancy. We have seen hotel appraisal reports which have just held expenses steady based on national averages, with no consideration of fluctuations in occupancy and average room rate. One expense category which is of great debate, is the reserve for replacement for hotels. A number of firms do not take the reserve for replacement into consideration. We believe they are overstating income, and value, by not reflecting this expense. There was a study done in the United States on Hotel Capital Expenditures over a 25-year period. This study was conducted by the International Society of Hospitality Consultants (ISHC), which found actual capital expenditures for hotels over a 25-year period were significantly higher than the normal 3% reserve for replacement used by feasibility firms and appraisers. In fact, the real cost over 25 years for a fullservice hotel with 300 rooms was more like 6.9% of total sales. HVS now has major Canadian Financial Institutions requesting that we use a 5% reserve for replacement. We have also seen appraisers reflect a reserve for replacement, but take a percentage of the income before debt, and not of total revenue. If followed in real life, this procedure would leave a hotel with insufficient capital for the replacement of furnishings and equipment. The textbook The Appraisal Of Real Estate, published by the Appraisal Institute of Canada, states that: �Replacement allowances are, however, relevant for certain types of properties that encounter very high periodic expenditures for replacements that have a limited economic life, such as the soft goods and furnishings associated with hotels and motels. The cost of replacements may reach $20,000 per unit and require replacement every five years. Since replacement is usually accompanied by colour changes or patterns, a significant expenditure occurs periodically. These costs may be reflected in a reserve for replacement allowance, amortized or simply stabilized.� HVS International performs a feasibility analysis with every hotel appraisal. We do not believe you can appraise a hotel accurately, without looking at the current market and future supply and demand factors. Unlike some forms of real estate that are stabilized by long term leases, hotels have to fill up daily. Any changes in the economy or the competitive supply can affect a hotel�s value. So, beware of firms and appraisers that are experienced in real estate, but have no thorough hotel experience, and vice versa. A hotel is not only real estate, but also has a business component. We recommend you use a professional with experience in both. |