| By: Stephen Rushmore, MAI, CHA - HVS International - New York

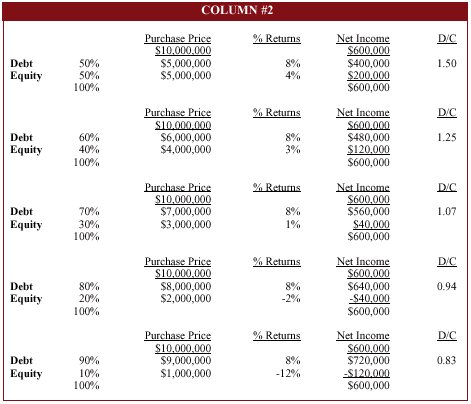

Investors acquire hotels to earn a return on their invested capital. This return includes periodic cash flow profits accruing after payment of debt service plus any property value appreciation or mortgage amortization realized when the hotel is sold. A return typically is expressed as a percentage of the capital invested and reflects the various risks associated with that particular investment. Hotels are considered risky investments as they require specialized management expertise, are vulnerable to economic downturns and overbuilding and suffer from rapid functional obsolescence. Hotels are relatively illiquid in that it can take three to six months to sell such an asset -even in a good market. Most hotel acquisitions generally are financed with both debt and equity capital. Debt comes from lenders such as banks, insurance companies, pension funds and other similar capital sources. Equity is typically raised by the hotel's owner and can come from friends, family, investors or equity funds. The primary difference between debt and equity is that debt generally has first preference to the Net Income of the hotel because payment of debt service must be made before profits can be distributed to the investors. Because debt lenders have this preference on the hotel's cash flow, their return requirements typically are lower than those of the equity investors. This differentiation between the returns desired by the debt and equity money sources gives rise to a phenomena known as financial leverage. Financial leverage is a method of increasing the returns to the equity investors by borrowing debt capital with lower return requirements and thus reducing the amount of equity needed to purchase the hotel. The more debt used to replace equity, the higher the leverage and the higher the "potential return" to the equity investor. For example, let's say a hotel generates a Net Income of US$1 million per year and can be acquired for US$10 million. If the buyer uses all equity to purchase the hotel, the return would be 10%. Now let's assume the buyer finances the hotel with 50% debt, which requires a debt service payment of 8% of the US$5 million borrowed or US$400,000 per year. This leaves US$600,000 to the equity investor as a return on the US$5 million equity invested or 12%. Column #1 in the following table shows how the equity return increases as the leverage escalates from 50% to 90%. With 90% of the hotel's purchase price financed by debt, the equity investor would achieve a 28% return on the US$1 million invested. Not bad. The downside of financial leverage is that should the US$1 million assumed Net Income in Column #1 decline, it is possible to create a negative leverage situation. Column #2 shows the consequences of what happens if the Net Income declines to US$600,000. With 50% leverage there is US$200,000 available to the equity investor producing a 4% return on the US$5 million invested. That equity return drops to 1% with 70% leverage and then crosses over to negative territory at 80% and 90% leverage, which means that the debt service exceeds the Net Income, and the equity investors must find additional sources of capital to pay the lender's debt service. With 90% leverage, the debt service is US$720,000, which is US$120,000 short of the US$600,000 of assumed Net Income. Not a pretty picture. Lenders attempt to reduce their risk exposure by evaluating the expected debt coverage ratio, which is the Net Income divided by the Debt Service. The debt coverage ratio for the 50% leveraged hotel with a US$1 million Net Income is 2.50. This ratio declines to 1.39 when the hotel is financed with 90% leverage. Most lenders want to see a debt coverage ratio of at least 1.25 debt coverage ratio at the US$600,000 Net Income. Leveraging a hotel acquisition can produce magical financial returns in up markets where expected Net Incomes are rising. However, leverage can work quickly against you when the economic picture darkens and Net Incomes decline. Most hotel investors opt for a more conservative approach to leverage and typically look to make an equity investment of between 25% to 35% of the purchase price. Even at this level of leverage, the equity return is enhanced by more than 50% when compared to an unleveraged return.

|