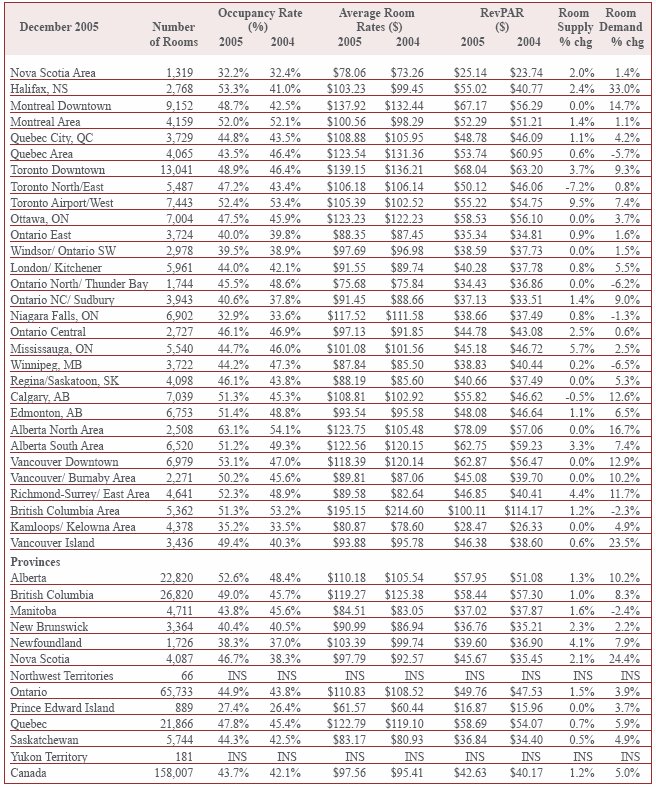

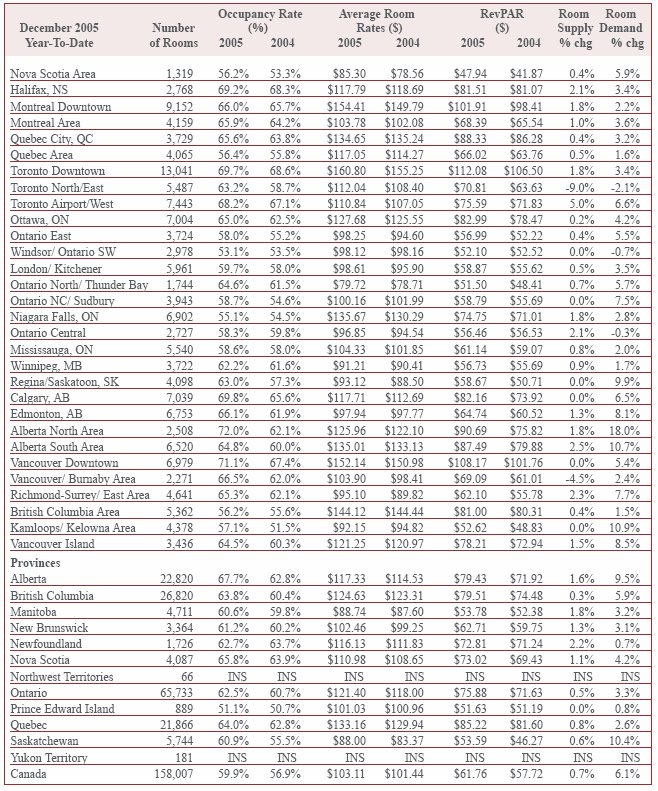

|

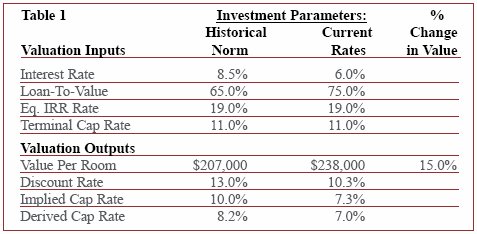

By: Suzanne R. Mellen, MAI, CRE - HVS International - San Francisco Since early 2004 reduced interest rates and lower equity yield requirements have had a substantial positive impact on hotel values. The greater availability and reduced cost of capital has resulted in roundly a 200 to 250 basis point decline in capitalization and free and clear discount rates from their pre-2004 historical norm, which, all other things being equal, has resulted in roundly a 15% to 20% increase in value, exclusive of net income driven gains. Additional value gains are now being fueled by more aggressive deal underwriting, as will be discussed in this article. The following example reflects the change in value for a representative hotel. Assuming an 8.5% interest rate, 65% loan-to-value ratio and equity yield of 19% results in a 13.0% overall free and clear discount rate, reflective of investment parameters prior to 2004. In the current market, with interest rates reduced to 6%, and the loan-to-value increased to 75%, the hotel is valued at a 10.3% free and clear discount rate. Conventionally, discount rates are generally equal to the overall capitalization rate plus the assumed underlying rate of change, or inflation. Thus, a projected 10.3% free and clear IRR equates to a 7% real rate of return, plus the assumed underlying inflation rate of 3%. Historically, a 13% discount rate would have been employed, equal to a 10% real rate of return plus the same 3% inflation rate.

Based on our observations, up to a year ago the hotel investment market recognized the transience of the current capital situation, that an eventual rise in interest rates, a swing to more conservative underwriting and a transfer of equity to other types of investments would ultimately result in a return of capitalization rates to their traditional norm, i.e. in the range of 8%to 12%, instead of the current 5% to 9% for quality hotel assets. Through early 2005, deals were still being underwritten assuming that there would eventually be a normalization of the cost of capital, i.e. that while acquisitions were being pursued at record low cap rates, there was a high likelihood that capitalization rates would return to their historical norm by the time the investment was to be exited, say within a five to ten year timeframe. Thus, the terminal capitalization rates applied to analyze the reversionary value at the end of an assumed holding period were more in line with historical norms, i.e. buyers assumed that cap rates would rise during their ownership period and they had to recognize this probability to insure that they were underwriting an achievable yield. Now we observe that a paradigm shift has occurred over the course of 2005: acquisitions are increasingly being underwritten assuming that there will be no �normalization� of capitalization rates -i.e. that the perfect confluence of capital factors that is in place today will remain in place when the asset is ready to be sold at some future point in time. Some of this thinking is fueled by the observation that new institutional players that have heretofore never been hotel investors are now competing for these assets, and that hotels are being viewed on the same plain as other real estate investments that had traditionally been perceived as lower risk, such as office buildings and shopping malls. The assumption is that these market participants, who are attracted by the higher relative yield of hotels, will remain in the investment pool, permanently changing yield requirements. Debt financing at high loan-to-value ratios is also expected to continue over the long term as hotel debt is increasingly being securitized based on consistently favorable underwriting. Another reason for this change in thinking on terminal capitalization rates may be that deal underwriters need to find more ways to support higher values in order to be the successful bidder in a very competitive market.

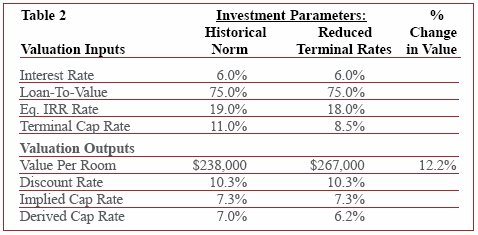

Utilizing an 11% terminal capitalization rate results in a value of $238,000 per room and implied and derived cap rates in the range of 7%. One can see the case being made that if an asset is being purchased at a 7% �going-in� capitalization rate then an 11% terminal cap rate is too high. However, it should be kept in mind that the 7% capitalization rate is being applied to a non-stabilized net income, i.e. some future upside in operating profits is expected over the near term. Reducing the terminal rate to 8.5% would still provide a 150 basis point spread over the �going-in� rate, the argument goes. Lowering the terminal rate to 8.5% actually increases the investment yield, or overall free and clear discount rate, making a case for a further lowering of the equity yield to 18%. The resultant free and clear discount rate for the investment remains the same, 10.3%, yet the value has increased by over 12%. Let us not forget that an 8.5% terminal capitalization rate implies that a new owner will apply a 7% to 7.5% �goingin� rate to formulate their purchase price, but that the rate will have to be adjusted upwards due to the likely need for capital improvements at the time of sale. Terminal capitalization rates have traditionally been adjusted upwards by 100 to 150 basis points above the �going-in� rate to reflect: 1) the increased age of the asset at the time of sale, 2) the need for significant capital expenditures above and beyond the annual reserve for replacement, and 3) the risk in forecasting a stabilized income stream so far into the future. Thus, applying an 8.5% terminal rate to this hotel investment implies that market conditions will be the same in the future as they are today, and that this rate will be applicable to a stabilized income stream, not one that is banking on future upside. If capitalization rates remain the same, the hotel will sell for $344,000 per room, indicating an appreciation of just under 3% per year, and the investor will earn their required yield of 18%. However, if the cost and availability of capital does return to its historical norm, and this hotel sells at an 11% capitalization rate (i.e. at 9.5% to 10%, adjusted upwards to reflect a terminal rate) then in ten years time the hotel will actually sell for slightly less than its original acquisition price ($266,000 per room), reducing the investment�s free and clear yield to a 8.5% and the equity yield to 14.2%. As appraisers we are charged with reflecting market conditions and the actions of buyers and sellers; only time will tell if we have indeed entered a new paradigm of lower yield expectations or if the traditional ups and downs of hotel operations and ownership will ultimately return hotel capitalization rates to historical levels. |

Table

1 illustrates the impact these changes in investment criteria have had

on value. The implied cap rate is the discount rate less the inflation

rate, while the derived cap rate is the forecasted first year�s net income

divided by the value conclusion. Both of these value calculations were

based on a ten-year discounted cash flow analysis with the application

of an 11% terminal capitalization rate, i.e. the cap rate applied

to a forecasted 11th year�s net income that would theoretically be used

by the next buyer to formulate a sales price upon the current owner�s exit

from the investment.

Table

1 illustrates the impact these changes in investment criteria have had

on value. The implied cap rate is the discount rate less the inflation

rate, while the derived cap rate is the forecasted first year�s net income

divided by the value conclusion. Both of these value calculations were

based on a ten-year discounted cash flow analysis with the application

of an 11% terminal capitalization rate, i.e. the cap rate applied

to a forecasted 11th year�s net income that would theoretically be used

by the next buyer to formulate a sales price upon the current owner�s exit

from the investment.

Table

2 illustrates the additional �value� that can be generated through the

use of a more aggressive, i.e. lower, terminal capitalization rate.

Table

2 illustrates the additional �value� that can be generated through the

use of a more aggressive, i.e. lower, terminal capitalization rate.