|

|

|

|

|

|

|

2002 National Lodging Forecast Ernst & Young LLP National Lodging Trends, Outlook & Segment Reports |

|

| Introduction

The Phoenix hospitality market slowed in 2001 and little new lodging development is on the horizon. In light of mixed market indicators including decreased corporate spending, rising unemployment trends, increasing drive-in demand potential, and continued population growth, a decline in RevPAR is anticipated for Phoenix during 2002. A slow, shallow recovery from a softened economy and September 11 is anticipated to occur in mid to late 2002. However, if the city�s hoteliers can weather the downward trend in the economy, RevPAR recovery may quicken its pace in the short-term due to limited new supply in 2002. In the long-term, new sports arena developments and the potential of a major convention center expansion may spur Phoenix�s tourism industry.

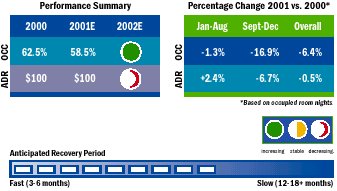

Source:Smith Travel Research,Ernst &Young LLP Major Demand Changes Phoenix, primarily a fly-to market with a heavy reliance on group business, is likely to see fewer visitors in 2002. The city�s hotel managers anticipate depressed operating profits due to corporate layoffs, limited business travel, fewer company retreats, and reduced convention/association meetings. By the fourth quarter of 2001, Phoenix�s office vacancy rates increased to approximately 15 percent while unemployment was approximately five percent, the highest level since 1996. The Camelback submarket was especially impacted, registering negative net absorption, as tenants found more economical space elsewhere. Despite negative economic factors, Phoenix is poised for a �soft-landing.� Due to reduced gasoline prices and refocused hotel marketing efforts, tourists are opting for closer destinations including short driving vacations. In addition, the city�s manufacturing sector is reportedly recovering from its negative inventory cycle which bodes well for local corporations such as Intel, Motorola, and Boeing. The 2001 World Series hosted in Phoenix and other local events such as the Phoenix Open and Fiesta Bowl, showcased the area as a destination city, and helped to generate interest in the area. Phoenix�s decline in 2002 RevPAR is partially a result of lowered room

rates to attract value-minded consumers. Operators foresee a softening

of the transient business segment, placing more dependence upon the leisure

and incentive group markets. While the extent to which the market will

fall is difficult to clearly project due to mixed demand signals, it is

anticipated that the market will regain its footing during the latter half

of 2002 primarily due to limited supply increases in all segments, with

the exception of luxury resorts.

Major Supply Changes Compared to the development pace of the mid-to-late 1990s, Phoenix has seen only one percent growth in new supply in 2001. This is compared to growth of five percent in 2000 across all segments. Capital improvement projects characterized most of the construction activity in 2001. The Fairmont Princess, the Boulders, and Sanctuary all completed spa amenities in 2001, while the Hyatt at Gainey Ranch added a new 12,000 square foot ballroom. With the exception of projects previously funded or under construction, 2002 is anticipated to be another slow year for developing new lodging properties due to unfavorable lending conditions. Major projects already slated for opening by late 2002 and early 2003 in the greater Phoenix area include, but are not limited to:

Political/Economic/Legal Changes Similar to other U.S. markets, Phoenix is experiencing an economic slowdown, especially when compared with recent high-growth years. Job reductions have become more common and new construction is constrained in all commercial segments. State spending has become a serious issue with a budget shortfall estimated at potentially $1.5 billion over the next two years. Michael Straneva, Phoenix

|

###

| M. CHASE BURRITT

National Director, Hospitality Services (305) 358-4111 BOSTON

DALLAS

LOS ANGELES

|

MIAMI

Mark Lunt (305) 358-4111 NEW YORK

PHILADELPHIA

PHOENIX

|

| Also See | 2002 National Lodging Forecast / Trends, Outlook, Market Segment Reports / Ernst & Young LLP / Feb 2002 |

| 2002 California Lodging Forecast / Ernst & Young LLP / Feb 2002 | |

| 2002 Manhattan Lodging Forecast / Top 10 Thoughts for 2002 and Beyond / Ernst & Young LLP / Feb 2002 | |

| Canadian Hotel Investment Report 2002 / Colliers International Hotels / Feb 2002 |