|

|

|

|

|

|

|

2002 National Lodging Forecast Ernst & Young LLP National Lodging Trends, Outlook & Segment Reports |

|

| Introduction

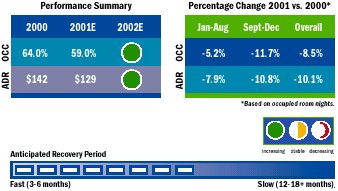

The Philadelphia lodging industry is suffering from the effects of a down year for convention bookings, a slowdown in the national economy, corporate travel cutbacks, empty rooms from cancellations caused by September 11, and additions to the city�s hotel room inventory in 2000 and 2001. The previous mayoral administration�s push for �2000 rooms for 2000� to host the Republican National Convention (RNC) resulted in the addition of nearly 3,700 new rooms over the past two years. With convention bookings up in 2002, the lodging market is anticipated to reflect slight gains in occupancy and a stable ADR as the market begins to absorb new supply. Recent additions to Philadelphia�s hotel room inventory should force many poorly located, older hotels to close entirely or partially, convert to alternative uses, employ aggressive room discounting programs, or focus on operational cost savings to remain competitive. Philadelphia Report

Major Demand Changes By 2005, the $500 million planned expansion of the Philadelphia Convention Center is anticipated to increase exhibition space by 50 percent, thus increasing commercial lodging demand for the city and bringing the Center to a total of approximately 1.5 million square feet. A planned $250 million Simon-DeBartolo 600,000 square foot retail/entertainment project, to be located along the Penn�s Landing waterfront, continues to experience indefinite postponements. The city received an economic boost throughout 2001 by hosting the NCAA Men�s Basketball East Regionals, ESPN�s X Games, the World Dragon Boat Championships, the U.S. Gymnastics Championships, and Cirque du Soleil. Positive economic momentum is anticipated to continue with the opening of the $245 million Kimmel Performing Arts Center by late 2001 and the ground-breaking of the planned $105 million National Constitution Center on Independence Mall, to be completed by spring 2003. The Philadelphia International Airport opened its new commuter terminal in the summer of 2001 and the $450 million international terminal is anticipated to open in 2002, which should enhance air travel capacity to the city. The Pennsylvania Convention Center has hosted an average of 23 citywide conventions per year since it�s opening in 1994, however, bookings dropped to an all time low of 19 in 2001. Bookings for 2002 have increased significantly to a record of 27, providing a much needed increase in room night demand. Although an expansion of Philadelphia�s convention center would allow it to compete with other Northeast locations for large meetings and conventions, competition will be fierce as 94 other convention centers nationwide will be expanded or constructed within the next 10 years. With the upcoming new commercial and institutional developments coupled with a $3 million promotional campaign targeted toward out-of-town tourists, the Birth Place of America is poised to capture additional commercial and leisure demand in the mid to long-term. Major Supply Changes The cumulative effect of 10 new or expanded hotels from 1999 to 2001, plus the anticipated addition of 430 rooms to downtown Philadelphia in 2002, represents a room increase of over 50 percent to be absorbed by the market in 2001 to 2002. Projects under construction or in planning include the $50 million, 270-room Residence Inn under construction at One East Penn Square, scheduled to open early 2002, and a $25 million, 50-room, five-star luxury hotel proposed for Old City. Several condominium hotels have been rumored, however, their status is uncertain given current market conditions. With increased convention center bookings for 2002, downtown hotel operators are likely to stabilize their 2000 to 2001 losses in occupancy levels. Older, marginally located, non chain-affiliated hotels are anticipated to suffer the worst performance levels due to new competitive supply, a lack of national reservation systems, few amenities, and/or a need for renovations. Political/Economic/Legal Changes With projects already underway in Washington DC and Boston, Philadelphia�s convention center expansion may not break ground until 2003 due to financial constraints as government officials deliberate fund allocations among other citywide and statewide political priorities. Good news for the existing convention center, however, included an early 2001 labor pact agreement anticipated to stem historical labor difficulties and increase the center�s low repeat business rate of 25 percent. Yet, with labor costs 30 percent higher than other competitive convention centers, return business to Philadelphia continues to be hampered. Challenges for the current political administration include a variety of issues such as the implementation of tax breaks, attracting and growing local businesses, reducing room rates, wages, and gross receipts taxes, developing new stadium projects, as well as governing and moderating municipal union labor issues regarding the operation of the convention center and the teachers� union. The convention center�s expansion will be placed under further financial uncertainty as a result of the city and statewide politics. Jay L. White, Philadelphia |

###

| M. CHASE BURRITT

National Director, Hospitality Services (305) 358-4111 BOSTON

DALLAS

LOS ANGELES

|

MIAMI

Mark Lunt (305) 358-4111 NEW YORK

PHILADELPHIA

PHOENIX

|

| Also See | 2002 National Lodging Forecast / Trends, Outlook, Market Segment Reports / Ernst & Young LLP / Feb 2002 |

| 2002 California Lodging Forecast / Ernst & Young LLP / Feb 2002 | |

| 2002 Manhattan Lodging Forecast / Top 10 Thoughts for 2002 and Beyond / Ernst & Young LLP / Feb 2002 | |

| Canadian Hotel Investment Report 2002 / Colliers International Hotels / Feb 2002 |