|

|

|

|

|

|

|

2002 National Lodging Forecast Ernst & Young LLP National Lodging Trends, Outlook & Segment Reports |

|

| Introduction

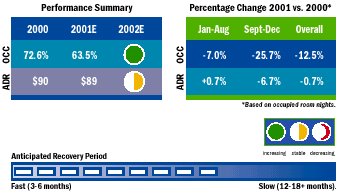

Orlando�s ability to achieve occupancies and average rates well above national averages, while maintaining one of the largest hotel room inventories in the nation, has been challenged by recent events. Theme parks, operating at 40 percent below typical attendance levels after September 11, are not anticipated to rebound to normal visitation levels until the third quarter of 2002. Given the number of projects in the development pipeline and recent demand changes, supply growth is anticipated to outpace negative demand growth, resulting in a downward trend in occupancy and average rate for 2002. Orlando Report

Major Demand Changes In response to lower levels of visitation, theme parks and lodging facilities began regional marketing campaigns to attract visitors within driving distance of Orlando, in hopes of combating the decline in air travel, which has led to significantly lower theme park visitation levels. With total passenger traffic at the Orlando International Airport down more than 23 percent in October, local area occupancies have dropped precipitously. For the months of September, October and November, occupancies were down approximately 28 percent, 24 percent, and 24 percent, respectively. Representing nearly 30 percent of Florida�s lodging inventory, these drastic demand drops in Orlando have significantly contributed to the decline in the state�s tourism revenues. Despite near-to-mid term weakening in Orlando�s tourism industry, the $748 million expansion of the Orange County Convention Center (OCCC) is anticipated to add one million square feet of exhibit space by late 2003. Upon completion of the expansion, group demand is anticipated to increase by approximately 30 percent over historical levels. By that time, the national economy is likely to have shown signs of recovery. Disney�s year-long celebration of the 100th anniversary of Walt Disney�s birth started in October of 2001 and includes special events, new attractions and live entertainment. These special events and attractions are anticipated to generate increased media awareness for the parks to boost demand. Though the original developer could not continue moving forward on the project, plans are still underway to build a World Expo Center in Kissimmee and the county has re-bid the project. Xentury City, developers of the Gaylord Palms Hotel, plans to bid on the project, which is anticipated to be completed by 2005 and attract additional convention and group demand to Orlando. Major Supply Changes Prior to September 11, projects in the pipeline through 2004 included the addition of approximately 21,000 hotel rooms, a 21 percent increase over Orlando�s 2000 year-end 108,100-room inventory. Limited-service hotels comprised less than 15 percent of this increase, which primarily consisted of large convention and full-service leisure hotels. Though no major projects have been cancelled to date, several have been postponed or delayed. Several projects opened in 2001 and approximately 4,700 rooms are slated to open in 2002. The 650-room Hard Rock Hotel at Universal Escape opened in January 2001, while the 1,307-room WDW Animal Kingdom Lodge and the 250-room Westin Grand Bohemian in downtown Orlando both opened in April of 2001. The Gaylord Palms Hotel, anticipated to open in February 2002, will feature 1,400 rooms and 400,000 square feet of meeting space. In addition, the 1,000-room Royal Pacific Resort is anticipated to open in June 2002 at Universal Escape. Orlando�s Grand Lakes Resort is anticipated to feature a 584-room Ritz-Carlton and a 1,000-room J.W. Marriott Hotel, both due to open in 2003. Additionally, hotelier Harris Rosen anticipates building a 1,500-room convention hotel, while Hyatt Hotels acquired land in the vicinity of the OCCC for a 1,500-room hotel. Both properties have a tentative opening date for 2004, but may be delayed to 2005. Other projects, however, are reportedly on hold, including Hilton�s planned 1,200-room hotel on land recently purchased from Universal Orlando, Disney�s 5,760-room Pop Century Hotel and the 1,000-room expansion of the Peabody Orlando. Also on hold is construction of the 732-room Omni at Champions Gate, a $700 million, 1,200-acre master-planned resort development adjacent to Celebration City. Next door, another major planned community, Reunion, has plans for up to 3,000 hotel rooms on its 2,100-acre site and is anticipated to open by the end of 2005. Political/Economic/Legal Changes Although the majority of Orlando�s service industry jobs have been saved and local county governments have approved $2 million for emergency marketing spending, it has been a very difficult time with major employers, including Disney and Universal Studios, resorting to layoffs and reduced work schedules. A possible increase in the tourist bed tax and a legislative change to use a portion of the tax proceeds to spur economic development is currently being discussed. A mid-term solution to traffic congestion is becoming increasingly important. New transportation improvement projects, totaling more than $3 billion, are currently in the planning stages and involve the widening of Interstate 4 through Orange, Seminole, and Osceola counties, the addition of high-occupancy vehicle and possibly toll lanes, as well as a new rail system. The Orlando International Airport is completing a $1.2 billion expansion, crucial for the area�s long-term tourism and business growth. Mark Lunt, Miami |

###

| M. CHASE BURRITT

National Director, Hospitality Services (305) 358-4111 BOSTON

DALLAS

LOS ANGELES

|

MIAMI

Mark Lunt (305) 358-4111 NEW YORK

PHILADELPHIA

PHOENIX

|

| Also See | 2002 National Lodging Forecast / Trends, Outlook, Market Segment Reports / Ernst & Young LLP / Feb 2002 |

| 2002 California Lodging Forecast / Ernst & Young LLP / Feb 2002 | |

| 2002 Manhattan Lodging Forecast / Top 10 Thoughts for 2002 and Beyond / Ernst & Young LLP / Feb 2002 | |

| Canadian Hotel Investment Report 2002 / Colliers International Hotels / Feb 2002 |