advertisement

U.S.

Lodging Growth Continues

Despite

Federal Economic Malaise

|

News for the Hospitality Executive |

advertisement

|

March 12, 2013, Atlanta, Ga. –

Despite news of “fiscal cliffs” and “sequesters” coming out of

Washington D.C., the U.S. lodging industry is forecast to continue to

achieve

strong gains in both revenue and profits in 2013. According to

the

recently released March 2013 edition of Hotel

Horizons®, PKF Hospitality Research, LLC (PKF-HR), is

projecting

that U.S. hotels will enjoy a 6.1 percent increase in revenue

per available room (RevPAR)

for the year, along with a 10.2 percent boost on the bottom-line net

operating

income.

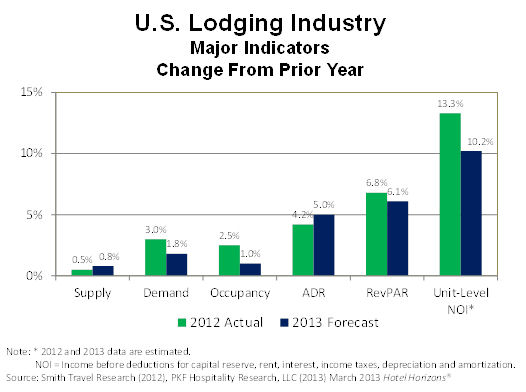

“The uncertainty and fear generated by Congress’ handling of the fiscal cliff and sequester may have tempered the pace of economic growth, but it has not completely shut down the growth in demand for lodging accommodations,” said R. Mark Woodworth, president of PKF-HR. “Our forecast of a 1.8 percent increase in demand for 2013 is somewhat muted compared to the 3.0 percent increase recorded by Smith Travel Research (STR) in 2012. However, when you combine the 1.8 percent growth in lodging demand with a projected increase in supply of just 0.8 percent, occupancy levels will rise to 62.0 percent. This will take the U.S. lodging industry past the long-run average occupancy level of 61.9 percent, a significant milestone.” Some of the economic headlines seen during the first two months of 2013 can be perceived as alarming. The Commerce Department issued a downward revision to its estimate of real Gross Domestic Product (GDP) for fourth quarter of 2012, and some prognosticators believe the economy will stall in 2013 because of the sequester. “Further analysis of these statements reveals that a significant factor driving this bearish outlook for GDP is a reduction in government spending,“ said John B. (Jack) Corgel, PhD., the Robert C. Baker professor of real estate at the Cornell University School of Hotel Administration and senior advisor to PKF-HR. “Fortunately, when it comes to the drivers of lodging demand, government spending is a relatively minor component of GDP. PKF-HR is more encouraged by Moody’s Analytic’s expectations for strong growth in personal consumption and business investment in 2013. These are the expenditures that really drive the demand for hotels.” “Of course, we realize that the hotel industry is a local business, and there will be some properties that are sensitive to the cutbacks in government spending triggered by the sequester,” said Woodworth. “Those most vulnerable are hotels that rely on government groups or are located near military bases, national parks, and other significant government installations the generate demand from both government workers and vendors to the government.” Good News in a Slowdown The 6.1 percent pace of RevPAR growth forecast for 2013 is less than the 6.8 percent increase achieved in 2012. However, to put it in perspective, the 2013 growth rate is more than double the long-run average of 2.9 percent.   Another benefit of raising room rates is the positive impact on hotel profits. After the 5.0 percent growth in ADR forecast for 2013, PKF-HR is projecting average room rates to grow at an even greater rate through 2016. “We are in the middle of a five year period where industry fundamentals are extremely solid: supply growth will be below average for the foreseeable future, which will lead to revenue and profit growth well in excess of the norm,” Woodworth noted. Great

News in the Acceleration

After slowing down in 2013, the pace of revenue growth for U.S. hotels is expected to accelerate dramatically in 2014. PKF-HR is forecasting RevPAR for the U.S. lodging industry to increase by 8.4 percent in 2014, the greatest annual gain in RevPAR since 2005. The RevPAR growth will be the result of a combination of a 2.1 percent increase in occupancy and a 6.2 percent rise in ADR. “Given where we are in the lodging cycle, the 6.2 percent growth in 2014 ADR is expected. On the other hand, the 2.1 percent rise in occupancy is an eye-opener. It can be attributable to the lift in employment growth as forecast by Moody’s Analytics, which will result in more demand moving toward the more moderate priced chain-scales in search of available and affordable rooms,” Woodworth explains. Looking beyond 2014, the optimistic outlook continues. New hotel development is expected to pick up and surpass 2.0 percent in 2015. However, based on Moody’s economic outlook, demand growth should continue at a level sufficient enough to maintain occupancy levels above 63.0 percent. In addition, room rates will grow greater than 5.0 percent through 2016. “The robust pace of the recovery will slow down a little in 2013, but it is important to remember that the industry is still growing despite the economic headlines. We continue to believe that this is a great time to invest in the U.S. lodging industry,” Woodworth concluded. To purchase a March 2013 Hotel Horizons® report, please visit www.hotelhorizons.com. Reports are available for each of 50 major metropolitan areas in the U.S., and contain five year projections of supply, demand, occupancy, ADR, and RevPAR. About PKF CONSULTING USA, LLC Headquartered in San Francisco, PKF Consulting USA, LLC (www.pkfc.com) is an advisory and real estate firm specializing in the hospitality industry. PKF Consulting USA is owned by FirstService Corporation (FSRV) and is a subsidiary of Colliers International. The firm operates two companies: PKF Consulting USA, LLC. and PKF Hospitality Research, LLC. The firm has offices in New York, Boston, Indianapolis, Chicago, Philadelphia, Washington DC, Atlanta, Jacksonville, Tampa, Orlando, Houston, Dallas, Los Angeles, Bozeman, and San Francisco.

|

| Contact: R. Mark Woodworth, President, PKF Hospitality Research, LLC 404 842 1150 ext. 222 [email protected] www.pkfc.com Chris Daly Daly Gray Public Relations Tel: 703 435 6293 [email protected] www.dalygray.com |