advertisement

Shale Natural Gas Fueling Pennsylvania Hotel Industry

|

News for the Hospitality Executive |

advertisement

Shale Natural Gas Fueling Pennsylvania Hotel Industry

|

January 10, 2012,

Philadelphia, PA – While the vast majority

of U.S. lodging markets were suffering from declines in revenue during

the

recent recession, hotels in northeastern Pennsylvania bucked national

trends

and achieved significant growth in RevPAR each and every year from 2007

through

2011. During this period, RevPAR for hotels located in the

Pennsylvania

counties of Bradford,

Lycoming, Susquehanna and Tioga has grown at an estimated

average annual

rate of 14.8 percent. This compares to the 1.7 percent average

annual decline

in RevPAR experienced by the overall U.S. lodging industry during the

same time

frame.

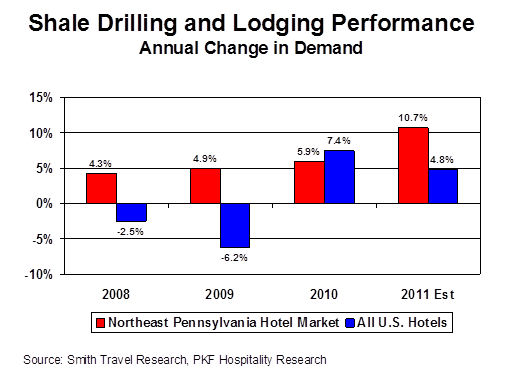

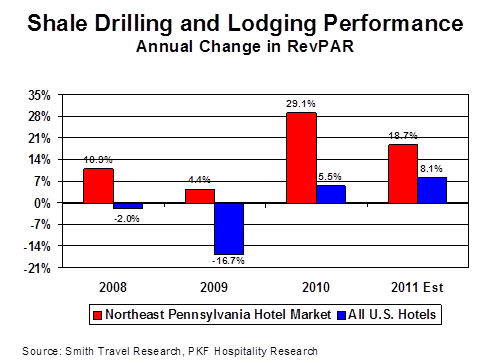

“When we present these data, most people think it is a misprint,” said Tony Biddle, senior consultant in the Philadelphia office of PKF Consulting USA. “The remarkable RevPAR growth observed in northeastern Pennsylvania is largely attributable to the exploitation of an old resource through the birth of a new industry: natural gas extraction from the Marcellus Shale.” The Marcellus Shale is a massive geological formation underlying much of northeastern Appalachia, including northern, central and western Pennsylvania. In August 2011, the U.S. Geologic Survey estimated that the Marcellus formation contains 84 trillion cubic feet (Tcf) of natural gas, propelling it to among the largest known shale natural gas “plays” in the world. Drilling and Demand Prior to 2007, market occupancies in northeastern Pennsylvania consistently averaged in the mid 50’s. However, in recent years, the occupancy rate has exceeded 70 percent and continues to increase.   “The correlation between drilling and lodging demand growth in the early stages of Marcellus development is intriguing,” Biddle said. “When you array the number of wells drilled in the region to the growth in lodging demand, you see a fairly consistent ratio of 200 new annual room nights of lodging demand per new well.” While the 14.8 percent annual growth in demand for the region’s hotels is remarkable, the 7.8 percent average annual increase in ADR over the past four years is even more outstanding given the sluggish economy and performance of the overall U.S. lodging industry. From 2007 to 2011, the average annual change in ADR for all U.S. hotels has been negative 0.7 percent. The Region’s Future The pace of future drilling activity is inherently difficult to predict due to a variety of factors, such as events in the political and legislative arenas and external macroeconomic trends. However, the Marcellus Shale Education and Training Center (MSETC), a collaboration of the Pennsylvania College of Technology and the Penn State Cooperative Extension, has published mid-term projections of Marcellus drilling for an area of Pennsylvania overlaying the northeast region. The MSETC projections indicate that heavy drilling activity in excess of 1,000 wells per year will continue in the region through at least 2014; however, the current rapid growth trend is expected to plateau in 2012. “Given the demonstrated historical relationship between drilling activity and lodging demand in the region, it appears that the majority of incremental drilling impacts to demand in this region have already been felt. That said, we note that prior projections by MSETC have underestimated drilling growth, and as we move forward, the 2012 outlook deserves close monitoring,” Biddle advised. National Implications An article in the December 27, 2011 edition of the Wall Street Journal noted that the boom in low-cost natural gas obtained from shale is “driving investment in plants that use gas for fuel, setting off a race by states to attract such factories.” This will continue to push the demand for shale natural gas. Therefore, we are seeing the new technological advancements which have unlocked shale gas reserves in Pennsylvania being applied in other regions of the U.S. “Hoteliers should be aware of the new shale explorations that are occurring all across the nation. Shale drilling has the potential to not only stimulate new lodging markets, like we’ve seen in Pennsylvania, but supplement existing markets as well,” Biddle concludes. To learn more about the impact of shale drilling on the lodging industry, please contact Tony Biddle at [email protected] or (215) 563-5300, ext 29. About PKF CONSULTING USA Headquartered in San Francisco, PKF Consulting USA (www.pkfc.com) is an advisory and real estate firm specializing in the hospitality industry. PKF Consulting USA is owned by FirstService Corporation (FSRV) and is a subsidiary of Colliers International. The firm operates two companies: PKF Consulting USA and PKF Hospitality Research. The firm has offices in New York, Boston, Portland, Indianapolis, Chicago, Philadelphia, Washington DC, Atlanta, Asheville, Jacksonville, Orlando, Tampa, Houston, Dallas, Los Angeles, Bozeman, and San Francisco. |

| Contact: Tony Biddle PKF Consulting USA Tel: 215 563 5300, ext 29 Email: [email protected] www.pkfc.com

Chris Daly |