advertisement

PKF's U.S. Hotel Forecast Indicates Recovery Better For Some, Not All

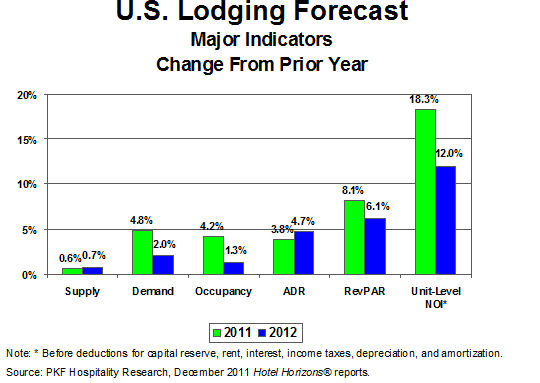

Overall RevPAR Projected to be up 8.1% in 2011 Followed by 6.1% Increase in 2012

|

News for the Hospitality Executive |

advertisement

PKF's U.S. Hotel Forecast Indicates Recovery Better For Some, Not All

|

December 13, 2011,

Atlanta, GA – While many hoteliers

are feeling angst and uncertainty caused by intimidating macroeconomic

conditions, PKF Hospitality Research (PKF-HR) is assertively

forecasting the

continued recovery of the U.S. lodging industry. How well you do

in 2012,

however, will vary depending upon the price of your room and where you

are

located. According to the recently released December 2011 edition

of Hotel

Horizons®,

PKF-HR forecasts that rooms revenue (RevPAR)

for U.S. hotels will rise 8.1 percent in 2011, and increase another 6.1

percent

in 2012.

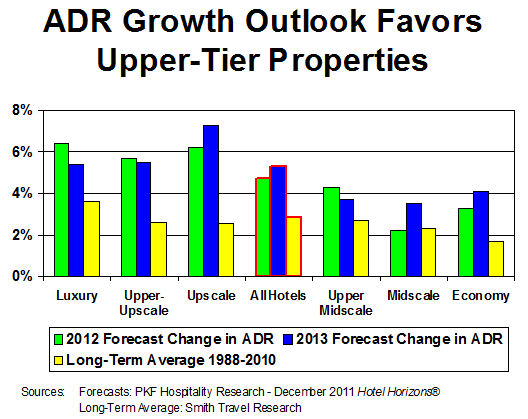

“Analyzing the performance of U.S. hotels in 2010 and 2011, we have seen the progression of indicators that one would expect during an industry recovery. Occupancy levels increased in 2010, followed by real average daily rate (ADR) growth in 2011,” said R. Mark Woodworth, president of PKF-HR. “The only surprise has been the pace and magnitude of the surge in hotel demand.”

Of greater importance is the future direction of lodging industry performance. “Looking forward, we are seeing familiar signs along the road to recovery. Owners and operators are now focused on more aggressive pricing policies, which in turn will translate into strong growth in hotel profits. We believe market conditions during the next few years will allow them to achieve these goals,” notes Woodworth. Recovery Disparities PKF-HR always cautions its clients that the national statistics may, or may not, apply to the type and location of hotels they own or operate. Looking deeper into the data, PKF-HR finds a continued bias favoring the future performance of hotels in the upper-tier segments of the industry. “The imbalance of lodging performance is extremely evident when observing the forecast occupancy levels by chain-scale,” Woodworth said. “Hotels operating in the upper-tier (luxury, upper-upscale, upscale) segments are all forecast to achieve occupancies above 70 percent in both 2012 and 2013, which will exceed their long-term average occupancy levels. Conversely, hotels in the lower-priced chain-scales will continue to achieve occupancy levels below their long-term average through 2013.”  The unevenness of the recovery is also apparent when analyzing the performance of the 50 markets for which PKF-HR prepares Hotel Horizons® forecast reports. In 41 of the 50 markets, hotels are renting more guest rooms today than they ever have in their history. However, the distribution of demand recovery varies by segment. In 49 of the 50 markets, upper-tier hotels have passed their previous peak levels of accommodated demand, but lower-tier hotels have reached the same milestone in only 16 cities. The Pricing Challenge “With national occupancy levels approaching their long-term average, and no meaningful new hotel supply additions in the foreseeable future, it is not a surprise that the pace of ADR growth is forecast to accelerate,” Woodworth said. PKF-HR is projecting the ADR for all U.S. hotels to increase 4.7 percent in 2012 and another 5.3 percent in 2013. The long-term annual average for ADR growth is 2.8 percent. With occupancy levels for upper-tier hotels forecast to exceed the 70 percent level, ADR growth for these properties will exceed the ADR increases projected for lower-tier hotels. However, all chain-scale segments are forecast to surpass their long-term average annual ADR growth rates in both 2012 and 2013.  “Hotel managers are eager to push room rates, but growth in ADR can have both positive and some offsetting consequences later,” warns John B. (Jack) Corgel Ph.D., the Robert C. Baker Professor of Real Estate at the Cornell University School of Hotel Administration and senior advisor to PKF-HR. “We know that RevPAR driven by ADR is more profitable for hotels. However, Economics 101 says that price increases ultimately reduce the demand for a product or service.” PKR-HR is forecasting U.S. lodging demand to grow 2.0 percent in 2012. This is less than the annual growth rates observed in 2010 (+7.4 percent as reported by Smith Travel Research) and projected for 2011 (+4.8 percent). “Industry participants should not be alarmed,” Corgel said. The pace of growth for indicators such as demand, occupancy, RevPAR, and net operating income will be slightly less in 2012 than they were in 2011. This does not mean the industry is slipping back into a recession. A deceleration in growth is to be expected at times during a recovery. The trajectory of performance is still on the rise, just not as steep.” Overall Optimism For 2012 “Many of our clients have been scared by the news of gridlock in Washington and the negative economic climate in Europe. They are not pessimistic. They are cautious in setting their expectations for 2012,” Woodworth observed. “When we look at industry fundamentals, as well as the national economic forecasts of Moody’s Analytics, we remain quite confident that 2012 will be another favorable year of growth for U.S. hotels. However, each owner and operator needs to make sure they have a thorough understanding of the local market factors and economics that will impact their hotel. Hotel performance will be great for some in 2012, but others will continue to struggle.” About PKF CONSULTING USA Headquartered in San Francisco, PKF Consulting USA (www.pkfc.com) is an advisory and real estate firm specializing in the hospitality industry. PKF Consulting USA is owned by FirstService Corporation (FSRV) and is a subsidiary of Colliers International. The firm operates two companies: PKF Consulting USA and PKF Hospitality Research. The firm has offices in New York, Boston, Portland, Indianapolis, Chicago, Philadelphia, Washington DC, Atlanta, Asheville, Jacksonville, Orlando, Tampa, Houston, Dallas, Los Angeles, Bozeman, and San Francisco. |

| Contact: R. Mark Woodworth PKF Hospitality Research Tel: 404 842 1150, ext 222 Email: [email protected] www.pkfc.com

Chris Daly |