advertisement

|

News for the Hospitality Executive |

advertisement

|

by Miguel Rivera, Senior Vice President,

HVS Asset Management & Advisory

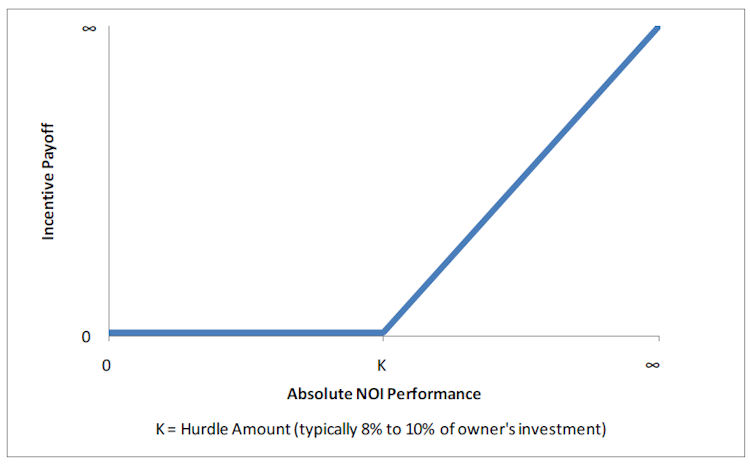

September 2011 If one starts with the basic premise that hotel managers should be paid for managing, the incentive management fee structures that are prevalent today largely miss the mark. They actually compensate managers based primarily on overall market performance, rather than their individual merits as managers. Hotel managers are typically paid a base fee equal to 2.0%-to-3.0% of total revenue—3.0% being the most common—plus an incentive. Incentive fee structures vary, but over the last decade or so, they have coalesced around a formula that pays managers 10% to 20% of cash flows that exceed a certain performance threshold. This threshold is generally reached when the net operating income exceeds a return on the owner’s investment of between 8.0% and 10%. The concept behind incentivizing managers based on free cash flows available to owners is to align the interests of management companies with those of owners. Unfortunately, an even more basic concept is often forgotten─ that managers should be compensated based on how well they manage. The structure of incentive fee thresholds compensates managers primarily based on the performance of the market, rather than the results achieved by management—exclusive of market performance. As a case in point, during the go-go years between 2004 and 2007 scarcely a manager went without incentive fee compensation, while in the down years of 2009 and 2010 the opposite was true. A better system would compensate high-performing managers for better-than-average performance in years good and bad. Management’s effectiveness is evidenced by two primary results: the ability to generate an appropriate share of top line revenue within the relevant competitive market (in other words, to produce the highest possible level of revenue per available room—RevPAR—penetration1); and to convert that revenue into as much sustainable cash flow available to the owner (net operating income, or NOI) as possible. Thus, the best way to truly align the objectives of management with those of ownership would be to base management compensation on RevPAR and Gross Operating Profit (GOP) margin penetrations2. Using GOP margins instead of NOI margins makes sense because expenses that are deducted from GOP to derive NOI, like insurance and real estate taxes, are mostly outside of management’s control. Managers should be compensated for executing well on things that are under their control; they should not be rewarded—or penalized—for things that are not. Below is a quick reference list of things that can be primarily controlled by management, and those that are primarily controlled by ownership as they relate to RevPAR and GOP margin penetration. TABLE 1- REVPAR AND GOP MARGIN PENETRATION

Each hotel, given its location and physical attributes relative to those of the competition, has a natural level of positioning within its market. This positioning should reflect the level of penetration that it would achieve under competent, but average, management. A hotel with superior location, and comparable age and facilities to the rest of its competition should garner a higher level of RevPAR penetration—assuming management of equal skill at all competitive hotels. Let’s assume that its superior location would warrant RevPAR penetration of 105%. Properties with higher RevPARs are naturally more efficient (particularly if the higher RevPAR stems from a higher ADR). Therefore, all other things being equal, this same hotel should garner a GOP margin penetration higher than 105%; let’s assume 107% (the actual figure can be estimated through methodical, but simple, computer modeling). Similarly, a hotel with an inferior location might only be expected to achieve 95% RevPAR penetration and 93% GOP margin penetration. Either way, this is the performance an owner should expect from an average manager. Incentive fees should be paid to exceptional managers that achieve results better than that. Some management contracts introduce some level of recognition of RevPAR penetration in their performance clauses. Such clauses commonly suggest that if RevPAR falls below 90% of the market’s RevPAR, there may be cause for termination. Unfortunately, these clauses have typically been used only to guard against poor management performance, not to set compensation. Furthermore, the 90% level has been picked arbitrarily, without consideration of the subject property’s competitiveness relative to its competitors. Managers have traditionally explained the current structure of incentive fees as a way of sharing risk with owners. However, risk implies potential losses, which management companies distinctly do not share. All they have achieved is sharing the upside with the owner by incorporating into their contracts a call option on hotel performance. The following chart illustrates the payoff to a management company resulting from the typical incentive fee structure. CHART 1- TYPICAL INCENTIVE FEE PAYOFF STRUCTURE  than it would have been with mediocre management). How management fees should be calculated Base management fees should be set so as to compensate managers for their cost of doing business, including overhead and base salaries. This is compensation for showing up to work and should not be a source of profit for management companies, as it generally is now. This implies base management fees of 1.0% to 2.0% of total revenue for most hotels, depending on size, or a duly considered flat fee. The fair levels of RevPAR and GOP margin penetration4 for a hotel should be carefully set by answering the question: What should the property’s fair penetration levels be, given management of average skill, after taking into account all of the hotel’s physical characteristics, and how it fits in within its competitive set. No doubt, this will be a source of debate between owners and operators, but it will be a debate worth having. As properties age, are renovated, competitors go in and out of business, and as demand sources shift, this fair penetration level should be adjusted. An incentive structure should then be set that handsomely rewards managers who achieve or surpass the appropriate benchmarks. For instance, as managers reach 90%, 100%, and beyond, of the fair RevPAR penetration level, that should trigger additional compensation. A suggested structure is presented in the following table. TABLE 2- SAMPLE INCENTIVE MANAGEMENT FEE STRUCTURE—REVPAR PENETRATION

The proposed structure pays managers the typical 3.0% of GRR management fee when they perform at least in line with expectations. It provides upside for outstanding managers to earn higher fees. As managers achieve GOP margin levels beyond those indicated by comparable properties, they should also be rewarded. The aggregate GOP margin of a comparable set of hotels can be obtained from a consulting firm like HVS; or a data consolidator, like STR. The fair GOP margin penetration level in many cases will be substantially different from the RevPAR one. For instance, most full service hotels compete with some of the higher-end select service properties, which have a vastly different cost structure. Hotels with larger room counts tend to be more profitable, as they spread their fixed costs across a larger room base. The extent of catering and other departmental revenue tends to lower overall profitability, as other departments are less profitable than room rentals. Within the same market, the presence of union labor can significantly alter the level of comparability. Properties that are part of large ownership portfolios will tend to benefit from different forms of economies of scale. The proper level of GOP margin penetration should encapsulate all these factors. Reviewing historical performance levels can go a long way to establish what the fair level of penetration should be. Selecting the right level of GOP margin penetration should not be taken lightly, and it will not always be a straight forward process. However, that does not mean that it should not be done, or that this process will not lead to better alignment than picking an arbitrary 8% owner’s return as a benchmark. An alternative approach—when existing data may be too skewed, or data may not be available—would be to select a broader GOP margin comparable set. Such a set may encompass properties from other submarkets, or all properties for an entire city or region, for example. As the set widens, however, it will lose its ability to track GOP margin changes attributable to market changes in the specific location of the subject property. The following table sets forth an example of what an incentive management fee structure based on GOP margin penetration should look like. TABLE 3- SAMPLE INCENTIVE MANAGEMENT FEE STRUCTURE—GOP MARGIN PENETRATION

TABLE 4- GOP PENETRATION LEVELS

If the GOP margin comparable set is, indeed, very comparable, an incentive fee with only a few tranches can be established. If there is less comfort about the level of comparability between the subject and its comparables (for example, for a new hotel, or a newly renovated one), a more gradual scale would be recommended. Such a scale would include more tranches, with easier thresholds and smaller gaps in the incentive percentages for each tranche. The example above suggests that the manager would receive an incentive fee equal to 2.8% of total revenue, roughly doubling a traditional base fee of 3.0%. To the extent that this manager also beat its RevPAR penetration target, as described in our earlier example, it could have earned total compensation between 5.8% and 6.8% of total revenue. This is a high level of compensation, which in this case, would have been well deserved as it would have been benchmarked off directly relevant parameters. It is important to avoid overly-incentivizing a manager for short term performance that potentially harms an asset’s long term value. For example, short-sighted cutting of Sales & Marketing and Repairs & Maintenance expenses can lead to short term boosts of GOP margin, but only to the detriment of future performance and asset value. Thus, any GOP margin goals should take into account sustainable levels of expenses in these categories, which should be tracked separately (in other words, marketing and maintenance expenses below certain levels should raise a red flag to be investigated further). This kind of misplaced short term focus should be monitored closely particularly close to the end of the manager’s contract term. As a way to mitigate this sort of misalignment, an owner could consider shifting more compensation toward RevPAR penetration performance (and away from GOP margin penetration) in the later years of a management contract. Benefits to Operators By shifting compensation to factors that are directly within management’s control, the fee stream due management companies will be much more predictable. Managers will earn incentive fees during both booming and declining markets based on their skill and performance, rather than the vagaries of the market. Decoupling market risk from management fee streams will warrant higher valuation multiples for operating companies. Comparable revenues driven off management performance, combined with a strong management track record, should lead to higher corporate valuations. Implementation While both operators and owners stand to gain from adopting the management fee structure proposed in this article, I anticipate several hurdles before it gains widespread acceptance. As with any change, inertia will initially favor the status quo. Since the present system demands less accountability of management companies, there is likely to be some natural resistance to incorporate the proposed structure into their own management agreements. This is unlikely to change unless competitive forces compel them to; or unless they confidently agree with my thesis that the proposed structure will increase the corporate valuations of strong managers, and they feel confident in their own ability as managers. I also anticipate that lenders will be initially reluctant to the idea of incentive fees that are payable during down markets, particularly during potential foreclosures, when there will be more competition for dollars available for debt service5. A dollar of income that is not lost during a down market due to superior management is even more valuable to a lender than an additional dollar of income that is gained during an up market. In principle, lenders should be quite open to incentivize managers to generate fewer lost dollars during downturns. However, I anticipate psychological reluctance. The key to overcome such reluctance will be to generate confidence in how those fewer lost dollars are counted. Finally, the proposed compensation structure is more complex than the compensation formulas that are in use today. This complexity needs to be well understood by management companies, the hotel general managers—and other executives—whose compensation will undoubtedly be affected by the changes, as well as by hotel owners and lenders before widespread adoption can take place6. Given the hurdles to implementation just described, I think it is likely that changes to the current compensation structure will permeate the industry from the bottom up. Newer and smaller management firms will adopt the new compensation structure first, as an edge to win new contracts based on better alignment of interests with property owners. Medium firms will follow as more owners embrace the concept and negotiate for it. The largest and most established firms will likely be late adopters. Perversely, it is the firms with the most skilled managers and honed-in systems that have the most to gain from implementing a new fee structure based on performance. Frequently, those managers and systems reside at the most established firms, which often are also the larger ones. Of course, there are many exceptions. Conclusion In sum, the current, prevalent incentive management fee structure broadly aligns the interests of management with those of ownership (maximizing cash flow). Unfortunately, it arbitrarily rewards managers primarily based on overall market performance, rather than management effectiveness. Both owners and good managers deserve better. __________________________________ 1 RevPAR

Penetration: measures how a hotel’s RevPAR compares relative to

those of its competitors. A hotel’s RevPAR penetration is calculated by

dividing the combined RevPAR of its competitors by its own RevPAR, and

is expressed as a percentage. A RevPAR penetration index equals RevPAR

penetration X 100.

2 GOP Margin Penetration: measures how a hotel’s GOP compares relative to those of its competitors. A hotel’s GOP margin penetration is calculated by dividing the combined GOP margin of its competitors by its own GOP margin, and is expressed as a percentage. A GOP margin penetration index equals GOP margin penetration X 100. 3 Excerpts from Marriott’s 2009 Q4 earnings call (transcript courtesy of www.seekingalpha.com): “…in North America, only 77 hotels earned incentive fees in 2009 or 11% of our domestic managed portfolio as many managed hotels did not achieve their owner’s priority. By comparison, during the low point of the last cycle in 2003, 22% of our domestic managed hotels earned incentive fees, so this recession has been much worse. …While most markets around the world have been impacted by the recession, some markets are emerging from the downturn faster and their recovery and long term growth should drive [incentive] fees higher” (Arne M. Sorenson, Marriott’s President and COO). Excerpts from Starwood’s 2010 Q4 earnings call (transcript courtesy of www.seekingalpha.com): “…U.S. incentive fees are not a large number because of the newness of some of our management contracts. …As it relates to incentive fees outside the U.S., clearly the management contract structure is linked to first-dollar incentives and those track profits quite well, which is why we've seen such healthy growth in Asia. The only part of the world where incentive fees have not been growing is in the Middle East and Africa, because RevPAR there hasn't grown”.(Vasant Prabhu, Starwood’s Vice Chairman, CFO, and EVP). Note that incentive fees outside North America are typically structured as a percentage of GOP (without a preferred return to the owner). Whether a preferred return is established or not, the primary driver of incentive fees is market RevPAR performance, not management performance (as these comments indicate). Excerpts from Hyatt’s 2011 Q2 earnings call (transcript courtesy of www.seekingalpha.com): “Overall, international fees increased almost 7% in the second quarter of 2010, excluding the impact of currency. Higher incentive management fees as a result of higher revenues and the continued ramp up of hotels added in prior periods were large contributors to the increase” (Harmit Singh, Hyatt’s CFO, Principal Accounting Officer, and EVP). Note, again, that incentive fees are being driven by revenue, which in turn is driven largely by overall market performance, not management performance relative to the competitive market. 4 Fair RevPAR Penetration: A hotel’s expected RevPAR penetration given competent management with average performance. Fair GOP Margin Penetration: A hotel’s expected GOP margin penetration given competent management with average performance. 5 I thank Charles Broun, Vice President – Capital Investments & Transactions – The Americas, at InterContinental Hotels Group for this insight. 6 I thank Yosung Chang, Project Manager – Capital Investments & Transactions – The Americas, at InterContinental Hotels Group for this insight.  About the Author Miguel Rivera is SVP of Asset Management & Advisory at HVS. He advises clients on maximizing real estate value and aligning a property's operations with its investment goals. He has more than 14 years of experience in real estate finance, including asset management, brokerage, financing, credit ratings, and appraisals. Prior to joining HVS, he was SVP at Jones Lang LaSalle Hotels, where he worked on more than $880- million worth of hotel real estate transactions while leading that group’s Latin American operations. He holds an MBA from Yale and a BS in Hotel Administration from Cornell. About HVS HVS is the world’s leading consulting and services organization focused on the hotel, restaurant, shared ownership, gaming, and leisure industries. Established in 1980, the company performs more than 2,000 assignments per year for virtually every major industry participant. HVS principals are regarded as the leading professionals in their respective regions of the globe. Through a worldwide network of 30 offices staffed by 400 seasoned industry professionals, HVS provides an unparalleled range of complementary services for the hospitality industry. For further information regarding our expertise and specifics about our services, please visit www.hvs.com. |

|

Contact: HVS Asset Management & Advisory 100 Bush Street, Suite 750 San Francisco, California 94104 United States of America Tel: +1 (415) 268-0368 Fax: +1 (415) 896-0516 [email protected] |

| Also See: | RevPAR

Adjusted Budgets: The Only Ones Worth Looking At (Part 3 of 3) /

Miguel

Rivera / June 2011 |

| RevPAR

Adjusted Budgets: The Only Ones Worth Looking At (Part 2 of 3) /

Miguel Rivera / June 2011 |

|

| RevPAR

Adjusted Budgets: The Only Ones Worth Looking At (Part 1 of 3) /

Miguel Rivera / June 2011 |