advertisement

The Only Ones Worth Looking At (Part 2 of 3)

|

News for the Hospitality Executive |

advertisement

|

by Miguel Rivera, Senior Vice President,

HVS Asset Management & Advisory

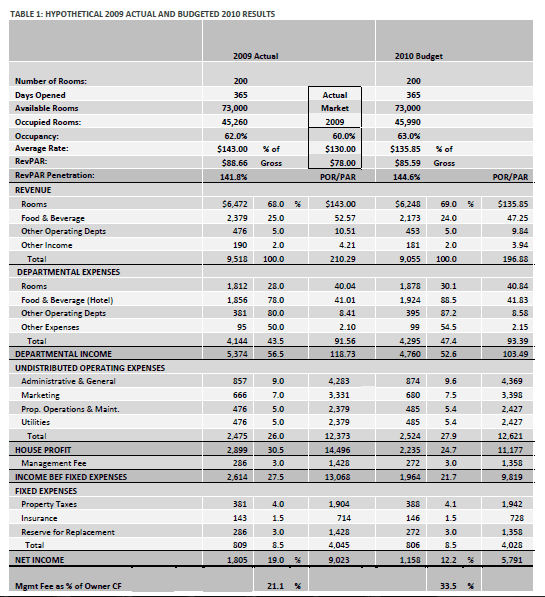

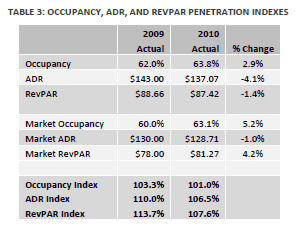

June 2011 Budgets are a good planning tool for hotel operators, owners, and other stakeholders. However, it is inappropriate to use them as benchmarks to measure a manager’s performance. It is intriguing then that so many people in the industry use them as targets to measure and reward performance. Perversely, this very fact makes budgets even less reliable, as it gives everyone involved in the budgeting process strong incentives to sway the numbers to their own advantage. Budgets are, at best, educated guesses of future performance, but they are not a substitute for indicators of actual performance against the rest of the market. One of the best ways to make budgets relevant is to adjust them using actual RevPAR indexes as the year progresses. This article describes a way to make these adjustments. PART II This article is the second of a three-part series that explores the rationale, methodology and results related to RevPAR-adjusted budgets. Adjusting budgets for a market’s RevPAR performance is proposed as a far superior tool to measure management’s performance, compared with unadjusted budgets. This second article introduces an example to illustrate how to perform the necessary RevPAR adjustments. To do so, four steps are identified. The first one is covered in this piece, while the remaining three will be the subject of the third and final part of this series (the link to the first article of this series is http://www.hvs.com/article/5229/revpar-adjusted-budgets-the-only-ones-worth-looking-at) The following table shows what a hypothetical 2009 budget for an upper-upscale hotel in the U.S. may have looked like. It reflects what were fairly typical expectations at the end of 2009 for 2010: occupancy flat to slightly up, ADR down about 5%, operating expenses increasing with inflation (assumed at 2.0%) on a peroccupied- room (POR) basis, and undistributed and fixed expenses increasing with inflation on a peravailable-room (PAR) basis.  The following table shows a summary of the actual results achieved in 2010 for our hypothetical hotel. The assumed market performance is in line with the one generally experienced by upper-upscale hotels nationwide.   While our hotel still attained an

occupancy and ADR higher than the market average in 2010, it became

less competitive than it was in 2009. Its occupancy, ADR, and RevPAR

indexes all declined in 2010. Since the market performed better than

was contemplated by the budget, how can we judge NOI results without

giving management credit for increased NOI that resulted from the more

favorable market performance?

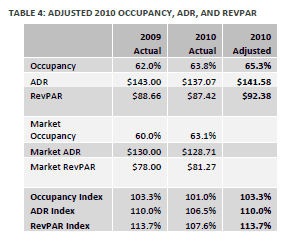

The answer is to restate the budget, adjusting for actual market performance. The following are the steps involved to accomplish that. 1. Adjust the budgeted occupancy and ADR (and, therefore, RevPAR) for actual market performance using penetration indexes. 2. Adjust other departmental revenue based on the revised RevPAR assumptions. 3. Adjust departmental expenses based on new revenue levels. 4. Adjust undistributed operating expenses, and fixed expenses based on adjusted RevPAR. Each step is described in detail in the following paragraphs. Step 1: RevPAR Adjustments The premise behind RevPAR adjustments is simply to restate the budget occupancy and ADR in terms of target penetration indexes. Managers seldom provide market penetration expectations as part of their budgets (in properties HVS asset manages, we always advocate for managers to do so; it encourages operators to focus on maintaining and/or increasing the competitive position of the hotel throughout the year, rather than on meeting an arbitrary budget number). For our example, we will assume a base expectation that penetration levels should remain constant with 2009 levels. We note that there are many factors that may warrant an expectation of changes in penetration levels, such as new competitive hotel openings or closings, major renovations or rebrandings at competitive hotels or the subject property, and major changes in demand generators. The following table shows the 2010 occupancy and ADR that our hypothetical hotel would have needed to maintain in order to keep its penetration indexes stable. This is accomplished by multiplying the market occupancy and ADR in 2010 by the respective 2009 index.  The

final four steps to adjust operating budgets for actual market

performance will be covered in the third and final section of this

three-part series of articles.

About the Author Miguel Rivera is SVP of Asset Management & Advisory at HVS. He advises clients on maximizing real estate value and aligning a property's operations with its investment goals. He has more than 14 years of experience in real estate finance, including asset management, brokerage, financing, credit ratings, and appraisals. Prior to joining HVS, he was SVP at Jones Lang LaSalle Hotels, where he worked on more than $880- million worth of hotel real estate transactions while leading that group’s Latin American operations. He holds an MBA from Yale and a BS in Hotel Administration from Cornell. About HVS HVS is the world’s leading consulting and services organization focused on the hotel, restaurant, shared ownership, gaming, and leisure industries. Established in 1980, the company performs more than 2,000 assignments per year for virtually every major industry participant. HVS principals are regarded as the leading professionals in their respective regions of the globe. Through a worldwide network of 30 offices staffed by 400 seasoned industry professionals, HVS provides an unparalleled range of complementary services for the hospitality industry. For further information regarding our expertise and specifics about our services, please visit www.hvs.com. |

|

Contact: HVS Asset Management & Advisory 100 Bush Street, Suite 750 San Francisco, California 94104 United States of America Tel: +1 (415) 268-0368 Fax: +1 (415) 896-0516 [email protected] |

| Also See: |

RevPAR

Adjusted Budgets: The Only Ones Worth Looking At (Part 1 of 3) /

Miguel Rivera / June 2011 |