advertisement

Uneasy Hotel Growth is Forecast

|

News for the Hospitality Executive |

|

Europe, 18 February 2011:

Hotel results in the Middle East & North Africa end 2010 with great

disparity, as some markets post true RevPAR growth and others still

negative.

"MENA is a challenging hotel market to analyse compared to say

Western Europe and the US. The region is not as mature, with countries

at different stages of the hotel cycle, i.e. performing completely

different to each other. Thus, the hotel cycle is a lot more

unpredictable, and erratic behaviour from some can easily overthrow

regional trends," comments Director of Development, MKG Hospitality,

Vanguelis Panayotis.

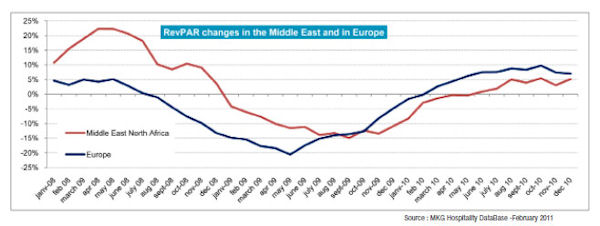

According to MKG Hospitality's market monitoring database HotelCompSet, mass tourism markets in North Africa and the Levant end 2010 on a high, with healthy hotel RevPAR growth. Morocco ends the year with over 20% RevPAR growth, followed by Egypt at 11%, Jordan 8% and Turkey 7%. "These countries are a lot more orientated towards mass tourism and all inclusive packages. This certainly proved to be a decisive factor throughout the year, as key source markets in Europe cut back on travelling expenses and chose to stay closer to home. Many of these countries were also able to draw on intra-regional tourism. explains Panayotis. South Africa also finished positive with a RevPAR increase of over 13%. However, as the sting of the World Cup fades, growth is gradually disappearing. Meanwhile Tunisia records a decline, affected by results in December, a month when civil unrest breaks out. Markets that were severely depressed 12 months earlier such in the GCC are finally turning around, with the decline slowing down. "Since this industry moves along a cycle, we can be quite sure that if conditions remain stable, momentum will continue along a similar line. And as demand continues to grow, hoteliers will be able to increase average prices and boost overall RevPAR. We already saw the same thing happen in more mature markets, such as in Western Europe, who entered the financial downturn approximately 6 months before MENA," continues Panayotis. By year end 2010, the GCC is in a much better position compared to the previous year, fuelled by increased demand. OR in Qatar grows by 9 percentage points, 4.6 in Oman and stabilises in Bahrain, Kuwait and the UAE. Despite OR falling, KSA in the only country to record an increase in ADR (11.7%) and in turn RevPAR growth (7.4%). "MENA is a challenging hotel market to analyse compared to say Western Europe and the US. The region is not as mature, with countries at different stages of the hotel cycle, i.e. performing completely different to each other. Thus, the hotel cycle is a lot more unpredictable, and erratic behaviour from some can easily overthrow regional trends," comments Director of Development, MKG Hospitality, Vanguelis Panayotis. According to MKG Hospitality's market monitoring database HotelCompSet, mass tourism markets in North Africa and the Levant end 2010 on a high, with healthy hotel RevPAR growth. Morocco ends the year with over 20% RevPAR growth, followed by Egypt at 11%, Jordan 8% and Turkey 7%. "These countries are a lot more orientated towards mass tourism and all inclusive packages. This certainly proved to be a decisive factor throughout the year, as key source markets in Europe cut back on travelling expenses and chose to stay closer to home. Many of these countries were also able to draw on intra-regional tourism. explains Panayotis. South Africa also finished positive with a RevPAR increase of over 13%. However, as the sting of the World Cup fades, growth is gradually disappearing. Meanwhile Tunisia records a decline, affected by results in December, a month when civil unrest breaks out. Markets that were severely depressed 12 months earlier such in the GCC are finally turning around, with the decline slowing down. "Since this industry moves along a cycle, we can be quite sure that if conditions remain stable, momentum will continue along a similar line. And as demand continues to grow, hoteliers will be able to increase average prices and boost overall RevPAR. We already saw the same thing happen in more mature markets, such as in Western Europe, who entered the financial downturn approximately 6 months before MENA," continues Panayotis. By year end 2010, the GCC is in a much better position compared to the previous year, fuelled by increased demand. OR in Qatar grows by 9 percentage points, 4.6 in Oman and stabilises in Bahrain, Kuwait and the UAE. Despite OR falling, KSA in the only country to record an increase in ADR (11.7%) and in turn RevPAR growth (7.4%). ABOUT MKG Group Established in 1985 by Georges Panayotis, MKG Group has built a solid reputation for business expertise and substantial European-based know-how in the fields of tourism, lodging and food service. MKG Group meets the needs of each of its clients by providing valuable analytical and decision-making skills necessary for success. www.mkg-group.com |

| For further information , please contact : MKG Group - International Development Department Vanguelis Panayotis T. : +33 (0)1 56 56 87 87 [email protected] MKG Hospitality - Media Contact Michael Komodromou Tel: +44 (0)20 7624 4030 [email protected] Web: www.mkg-hospitality.com

|