advertisement

Lodging Econometrics Reports U.S. Q4 2010 Transaction Volume:

2010 Average Selling Price Up 86% From 2009

Indicates Future Transactions to Escalate Through 2014

|

News for the Hospitality Executive |

advertisement

|

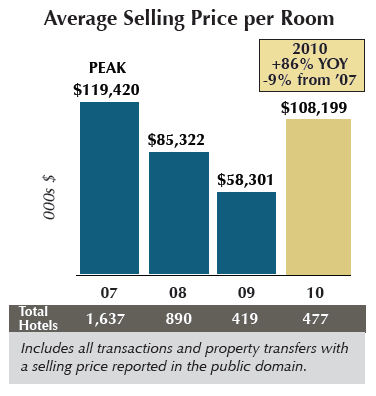

February 8, 2011 - A total of 1,298 hotels were sold or transferred in 2010, up two and a half times from 2009, when only 513 hotels changed hands. The volume increase was largely due to a revived Wall Street, rekindling M&A activity. Individual and Portfolio Transactions increased 19% year-over-year (YoY) from 513 hotels to 608 hotels. An additional 690 hotels were transferred in two separate mergers. Transaction volume is poised to increase over the next three years, with Wall Street banking activity accelerating and a large flow of existing real estate loans coming due. Many of these assets will be distressed, presenting attractive investment opportunities for those able to access funds.  The Average Selling Price Per Room (ASPR) for transactions

with a reported selling price increased an astonishing 86% YoY and just

9% down from the all-time high recorded in 2007. For the 477 hotels

reporting, ASPR rose to $108,199/room compared to $58,301 in 2009. In

2007, ASPR peaked at $$119,420/room. Selling prices will continue to

increase going forward, but at a more modest pace, as a broader mix of

hotel types should soon begin to come to market and as interest rates

creep up. The Average Selling Price Per Room (ASPR) for transactions

with a reported selling price increased an astonishing 86% YoY and just

9% down from the all-time high recorded in 2007. For the 477 hotels

reporting, ASPR rose to $108,199/room compared to $58,301 in 2009. In

2007, ASPR peaked at $$119,420/room. Selling prices will continue to

increase going forward, but at a more modest pace, as a broader mix of

hotel types should soon begin to come to market and as interest rates

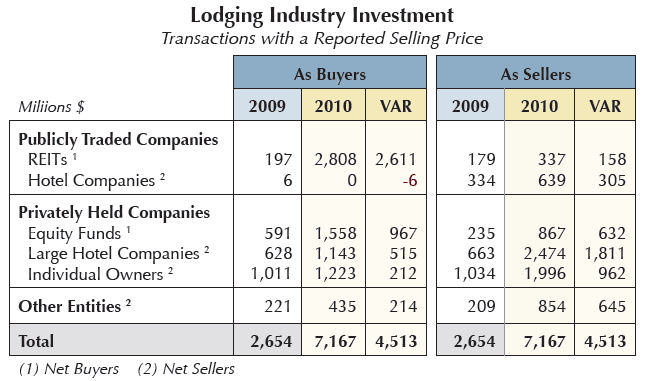

creep up.ASPR can justifiably be described as “frothy.” In 2010, there was not a regular distribution of hotels transacted across all chain scales, brands and locations, as in 2007. Instead, a higher proportion of hotels were of institutional-quality and sizes. As such, these hotels were either newer or classic, older properties. There was a skewed concentration of luxury, upper upscale and select-service hotels in the Top 25 Markets, in CBD’s, key suburban locations, and in destination resorts. In 2010, many select-service hotels sold at or near the selling price highs recorded in 2006-2008. A number also sold at or exceeded their estimated cost of replacement. Among the brands in such high demand included: Residence Inn, Courtyard by Marriott, SpringHill Suites, Hilton Garden Inn, Homewood Suites, and Hampton Inn & Suites. The rapid recovery of investment banking contributed to the strong rebound in selling prices. New REITs were formed and were able to access both equity and debt. Older REITs, publicly traded hotel companies and private equity groups were also able to secure corporate debt at record low interest rates. With so many well-funded investor groups chasing too few investment opportunities, prices were bid higher than usual, as these investors were highly motivated to enter the market as early as possible in the new cycle. 2010 REAL ESTATE INVESTMENT FLOWS NEARLY TRIPLED In 2010, total industry investment flows reached an estimated $13.5 billion, the highest since pre-recession 2007. Of that total, $7.2 billion was from the 477 hotels that reported a selling price, a 270% increase from $2.7 billion in 2009. An estimated $2.1 billion was for all other fee simple transactions, while $4.2 billion was attributed to two mergers. For the 477 transactions with a reported selling price, REITs accounted for 40% of total investment dollars at $2.8 billion for the year, up $2.6 billion from 2009 when they invested just $197 million. These publicly traded entities mainly targeted high-quality individual assets, and often were able to pay premium prices because their equity return requirements are generally lower than privately held companies.  With capital so plentiful, all investor sectors, both publicly traded and privately held companies, accelerated disposition activity in 2010. It was a perfect time to dispose of hotels that could not be sold previously because the capital markets were seized up. Assets that no longer fit their long-term objectives, particularly distressed hotels, were first to be pruned from their portfolios. Originating lenders were frequently involved in “3-corner transactions,” as fresh capital from new investor groups was highly coveted and created the opportunity for all parties to seek resolution. |

| Contact: Lodging Econometrics |