advertisement

Lodging Econometrics

Revises its 3rd Quarter Forecast for New Hotel

Openings Downward to 562 Hotels for 2011 & 515 Hotels for 2012

|

News for the Hospitality Executive |

advertisement

Lodging Econometrics

Revises its 3rd Quarter Forecast for New Hotel

Openings Downward to 562 Hotels for 2011 & 515 Hotels for 2012

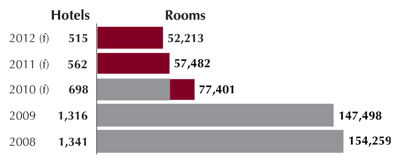

November 2010 - LE has revised its Forecast for New Hotel

Openings downward for 2011 and 2012, as the ongoing banking crisis

continues to curtail the availability of construction financing. In

2011, a revised 562 new hotels/57,482 rooms are now projected to open,

while the Forecast for 2012 has been lowered to 515 hotels/52,213

rooms. 2010 has been adjusted downward only slightly to 698

hotels/77,401 rooms, of which 519 hotels/56,007 rooms have already

opened during Q1-Q3. November 2010 - LE has revised its Forecast for New Hotel

Openings downward for 2011 and 2012, as the ongoing banking crisis

continues to curtail the availability of construction financing. In

2011, a revised 562 new hotels/57,482 rooms are now projected to open,

while the Forecast for 2012 has been lowered to 515 hotels/52,213

rooms. 2010 has been adjusted downward only slightly to 698

hotels/77,401 rooms, of which 519 hotels/56,007 rooms have already

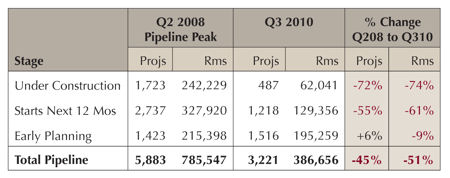

opened during Q1-Q3.The lack of financing will have a profound effect on the number of New Openings over the next three years. Projects that are already in the Pipeline cannot migrate forward to start construction. The actual number of projects that start construction in a given quarter, Construction Starts, reached a cyclical low in Q2. Also, the total number of projects presently Under Construction, at 487 projects/62,041 rooms, is the lowest we’ve ever recorded. Projects Scheduled to Start Construction in the Next 12 Months, at 1,218 projects/129,356 rooms, are at their lowest level since the end of 2004. The result of these bottoming metrics is that hotel openings coming online as New Supply in 2011-2013 will be at rates lower than at any time since the early 1990’s. From an operations perspective, hotel owners and operators consider this excellent news, as the timing of the slowdown in New Openings could not be more perfect. After two and a half years of steady operating declines, the industry began its recovery in earnest in early 2010. Year-over-year (YOY) occupancy turned positive in February, RevPAR and room revenues in March, and room rates in July. Every month since, each operating metric variance has continued positively. In fact, in three of the last four months, room revenue growth has exceeded 10% YOY. These operating improvements are better than expected and should continue trending upward, as there will be few new supply headwinds to overcome for the foreseeable future. In fact, overall YOY demand growth first exceeded YOY supply growth in February and should continue to outpace for the next few years. Recovering from the greatest recession since the mid-1940’s, all operating metrics signal that the rate of industry-wide improvement is greater and faster than originally expected, which truly is good news for owners and operators. Improved room demand, better lodging operating results, gradual improvements in the economy and indications from lenders that financing terms may soon start to loosen are beginning to stir developer sentiment. An early sign is the 70 New Project Announcements that are larger than 150 rooms recorded last quarter. 35 or 50% were previously in the Pipeline, but were cancelled or put on hold. The re-entry of these older, planned projects indicates some improvement in developer sentiment and could be the precursor of a new construction cycle starting sooner than expected. An early start to the next cycle could also be hastened if more distressed hotels are resolved in private, rather than being formally put on the market for sale as foreclosed or otherwise distressed assets. CONSTRUCTION PIPELINE OVERVIEW  The Construction Pipeline is at 3,221 projects/386,656

rooms as of the end of Q3 2010. Pipeline totals continue to decline and

are now at their lowest level since Q3 2005, however the rate of

decline has recently moderated. Under Construction totals, at 487

projects/62,041 rooms, represent just 15% of projects and 16% of rooms,

and are the lowest since the 1990’s. Totals for projects Scheduled to

Start Construction in the Next 12 Months, at 1,218 projects/129,356

rooms, have also continued to decline and are at a low not seen since

Q4 2004. The Construction Pipeline is at 3,221 projects/386,656

rooms as of the end of Q3 2010. Pipeline totals continue to decline and

are now at their lowest level since Q3 2005, however the rate of

decline has recently moderated. Under Construction totals, at 487

projects/62,041 rooms, represent just 15% of projects and 16% of rooms,

and are the lowest since the 1990’s. Totals for projects Scheduled to

Start Construction in the Next 12 Months, at 1,218 projects/129,356

rooms, have also continued to decline and are at a low not seen since

Q4 2004.Totals for Early Planning have remained somewhat constant, as these projects are generally larger, are in both urban centers and resort destinations and sometimes have mixed-use components. Projects of this magnitude have long development timelines from inception through completion, and in that sense bridge across development cycles. For the foreseeable future, the total Construction Pipeline is expected to continue trending downward, albeit at a slower pace.  BUYER & SELLER

ACTIVITY DRAMATICALLY CHANGED

In 2010, REITs have spent $1.87 billion in acquiring 46 high profile properties, a remarkable 10 times the dollar amount invested for the comparable 2009 period. Thus far, the amount invested for acquisitions by REITs is 5½ times that of their divestment totals. Equity Funds have increased their investment to $1.029 billion for 48 transactions this year, up from $330 million, a $700 million increase over 2009. They too are net investors, as their dollar volume of acquisitions is twice the amount of their divestments. Flush with cash, these investor groups have often paid a premium to attract such scarce, high profile properties. They often forgo normal leverage targets and invest larger amounts of cash, sometimes up to 100% of the purchase price, in order to effectuate market entry at the bottom of the cycle. Privately held large hotel companies are the largest net sellers in 2010, divesting $1.745 billion in hotel real estate, up 3½ times from the comparable 2009 period. Individual owners follow at $1.136 billion, up 31% from 2009.

|

| Contact:

Lodging Econometrics

|