advertisement

Lodging

Asset Values In Recovery

|

News for the Hospitality Executive |

advertisement

Lodging

Asset Values In Recovery

|

By Scott Smith MAI and Bill Morton

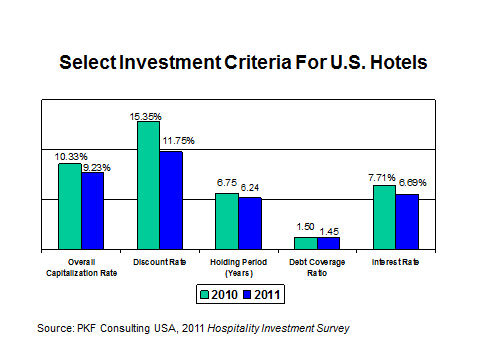

November 2011 Despite inconsistent economic news, increases in lodging demand and property-level net operating income (NOI) have most industry participants feeling optimistic that hotel property values are heading upward. An analysis of the 2011 edition of PKF Consulting USA’s Hospitality Investment Survey (conducted in the spring of 2011) sheds some light on the market and transaction factors that are influencing this line of thinking.  Investment Criteria Overall capitalization rates for all hotels decreased 110 basis points when compared to 2010. This reflects survey respondents’ reaction to the more attractive debt environment, as well as the anticipation that property level NOI will continue to increase. Investors continue to place a premium on the full service segment due to its greater upside, high barriers to entry and the current difficulty to obtain construction financing. Terminal capitalization rates also declined compared to our previous survey, however to a lesser degree. Concurrent with the decline in capitalization rates, discount rates, or un-leveraged IRR’s, for hotels decreased to 11.75 percent. The 253 basis point spread between the overall capitalization rate and discount rate suggests investor yield requirements have lowered when compared to last year, likely due to the decreased level of risk and overall landscape of the current lodging market. Equity yields followed a similar downward trend, though hotel investors continue to expect handsome returns when compared to other forms of investment real estate. Cash-on-cash returns experienced little change compared to what we learned in 2010, and the average holding period indicated by the survey respondents decreased slightly. Mortgage Criteria Debt service coverage ratios also decreased and are now in line with 2008 levels, suggesting that lenders are starting to “loosen up” with regards to their underwriting. This year’s survey indicated that interest rates reached their lowest point in recent history at 6.69 percent, a decrease of 84 basis points when compared to 2010. Loan-to-value ratios increased compared to last year, but remain well below 2007 levels. The 2011 mortgage terms offered by lenders generally indicate better terms are becoming available as the market rebounds. Multiple respondents revealed that the ability to obtain first mortgage financing has substantially improved compared to 2010; however renovation and new construction financing remain difficult to secure. Furthermore, our survey revealed that participants active in the market prior to the recession such as CMBS debt, life insurance companies and commercial banks are beginning to resurface, and are eager to lend to experienced sponsors with solid balance sheets. Overall deal volume, particularly among real estate investment trusts (REITs), has surged since the beginning of 2011. With a lower overall cost of capital and financing flexibility that includes equity along with debt, REITs are aggressively targeting hotel properties in all segments, particularly high quality assets in major markets. Leading the way is Ashford Hospitality, who spent $1.28 billion on the 28-property Highland Hospitality portfolio. Pebblebrook Hotel Trust (spending over $780 million on 10 hotels) and Apple REIT (spending roughly $475.8 million acquiring over 20-hotels) have also been active players. Real World Experience Throughout the year, PKF Consulting USA (PKFC) professionals conduct hundreds of appraisals related to the sale, purchase, construction, and re-financing of lodging properties. In our experience assisting clients with valuations, the actual mortgage and investment criteria we have encountered is consistent with sentiment of hotel owners, investors, and lenders reflected in the survey. Based on our work experience, the following paragraphs summarize what our clients are telling us in 2011:

In summary, based on our firm’s Hotel Horizons® forecast, the property level NOI increases experienced in 2010, and the results of the 2011 Hospitality Investment Survey, we anticipate further increases in asset values over the next few years. Scott Smith, MAI is Senior Vice President in the Atlanta office of PKF Consulting USA. Bill Morton is Senior Consultant in the Indianapolis of PKF Consulting USA. For more information regarding appraisal services, or the 2011 Hospitality Investment Survey, please visit www.pkfc.com. This article was published in the October 2011 edition of Lodging. |

| Contact: Robert Mandelbaum Director of Research Information Services Colliers PKF Hospitality Research 3475 Lenox Road Suite 720 Atlanta, GA 30326 404-842-1150, ext 223 (Direct) 404-842-1165 (Fax) [email protected] www.pkfc.com

|