![]()

advertisement

For Q1 2010, the Total Hotel Construction Pipeline for

the Americas Stands

at 590 projects, a Decline of 38% Since the Q1 2008 Peak

Development Concentrated in Canada, Brazil and Mexico

|

News for the Hospitality Executive |

![]()

advertisement

For Q1 2010, the Total Hotel Construction Pipeline for

the Americas Stands

at 590 projects, a Decline of 38% Since the Q1 2008 Peak

Development Concentrated in Canada, Brazil and Mexico

|

May 17, 2010 - Total

projects in the Construction Pipeline for the Americas have decreased further,

as the breadth of economic declines and difficulties in sourcing lending

continue to weigh on lodging development. The total Pipeline is now at

590 projects/93,313 rooms at the end of Q1 2010, down 38% by projects and

42% by rooms from the peak in Q1 2008.

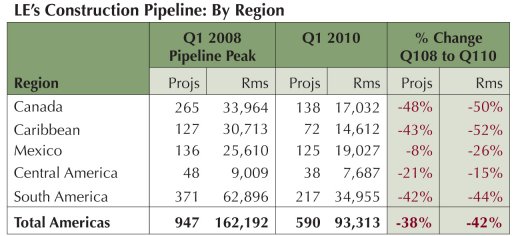

Because New Project Announcements (NPAs) into the Pipeline are likely to remain in a cyclical trough, overall Pipeline counts are expected to fall further. The continued high number of projects exiting the Pipeline as New Openings through 2010 and 2011 are another contributor to future Pipeline declines. The rate of New Openings is expected to decrease substantially in 2012 and remain depleted through mid-decade, allowing time for the industry to absorb the wave of new supply additions from this cycle and ensuring a quicker and more complete recovery for industry-wide operating performance. Development in the Americas is highly concentrated in countries that have larger and more fully developed economies. Canada, Brazil and Mexico combine for 66% of all Pipeline projects in the Americas. With the addition of the next seven leading countries (Argentina, Columbia, Panama, Dominican Republic, Costa Rica, Venezuela, and Puerto Rico), the percentage rises to 87%. The remaining 32 countries account for the final 13% of all hotel construction activity.

REGIONAL NOTES In Canada, the total Construction Pipeline has 138 projects/17,032 rooms. At 60 projects/7,834 rooms, Under Construction totals are at a level not seen since H1 2006. While rates and terms are favorable, financing is still difficult to acquire, hampering project migration up the Pipeline toward construction. The result is that Constructions Starts for projects already in the Pipeline are at a five-year low. Also, NPAs into the Pipeline are already low and are expected to remain so for the near-term. The Caribbean, with a total Pipeline of 72 projects/14,612 rooms, continues to be affected by the lack of institutional financing for the large, resort projects typical of the region. Cancellations/Postponements are decreasing, as the less feasible projects have mostly been cleansed from the Pipeline over the last two years. As a sign of renewed investor interest, five projects previously on hold have been reactivated and returned to the Pipeline, three being larger-sized luxury projects. In the Luxury segment, demand declines are thought to have nearly halted and recent room rate improvements have shown surprising strength.

With 125 projects/19,027 rooms, Mexico�s Pipeline has not declined as substantially as in other parts of the Americas. However, Pipeline counts will continue to decline modestly over the next two years, as NPAs stay at reduced numbers until lending becomes more available and the hotel recovery sees more significant improvement. Luxury development continues in the beachfront resort areas but at a lesser pace. The most recent activity is with globally branded, smaller midmarket hotels that are spreading throughout the secondary and tertiary markets, as it is easier to acquire financing for properties of this size. The Midscale without Food & Beverage segment makes up half of the branded Pipeline, with 54 projects/5,744 rooms. Central America has 38 projects/7,687 rooms in its Construction Pipeline. Half of those projects are in Panama, most of which are in the capital, Panama City. 42% of all Pipeline projects are currently Under Construction. South America�s Pipeline, at 217 projects/34,955 rooms, is set to unfold later than other regions in the Americas, as a very high 61% of all projects are currently Under Construction. Much of this is in Brazil, which has 126 projects/21,454 rooms in its Pipeline, or 58% of all projects in South America. Like other regions in the Americas, Pipeline counts are expected to tail off significantly, as the availability of lending continues to stifle the number of NPAs into the Pipeline. Cyclical high New Openings through 2012 will also contribute substantially to the Pipeline�s decline as this cycle draws to a close.

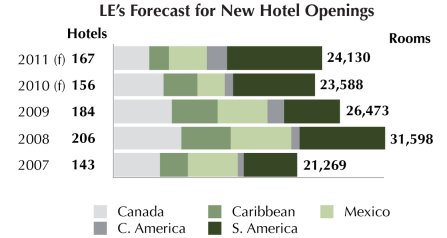

LE�S FORECAST FOR NEW HOTEL OPENINGS New Hotel Openings in Canada peaked in 2008 and have been trending downward since. In 2010, LE expects 46 hotels/5,741 rooms to open, with 31 hotels/3,953 to open in 2011. In the Caribbean, New Openings will remain sizeable in 2010, when 49 hotels/8,313 rooms will enter as new supply, then fall off substantially to just 14 hotels/2,347 rooms in 2011. For Mexico, New Openings will dip to 22 hotels/3,253 rooms in 2010, then rise slightly to 31 hotels/4,388 rooms in 2011. 6 hotels/991 rooms will open in Central America in 2010, then 10 hotels/2,297 rooms in 2011. LE�s Forecast for South America projects cyclically high New Openings of 61 hotels/9,534 rooms in 2010, then a new high of 81 hotels/11,145 rooms in 2011. With their shrinking Pipelines, all regions in the Americas will see declines in New Openings from 2012 to mid-decade. LODGING ECONOMETRICS CREATES TWO NEW PROGRAMS TO BOLSTER HOTEL ACQUISITION INITIATIVES Distressed Hotel Assets � With details for every hotel publicly announced as being distressed over the last 18 months, these reports include all property facts and complete contact information for the ownership group and lead lender. Halted Construction Projects � Receive records for all projects that

have ceased construction prior to completion, with project details and

complete contact information for the principals. In most cases, the principal

and lender of the property are anxious to continue construction, and would

welcome new investment into the project.

|

| Contact:

LE

|