![]()

advertisement

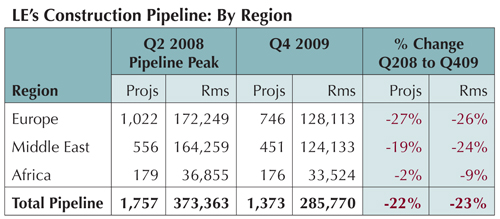

For Q4 2009, the Total Hotel Construction Pipeline for

Europ,

Middle East and Africa Stands at 1,373 Projects, a

Decline of 22% Since the Q2 2008 Peak

|

News for the Hospitality Executive |

![]()

advertisement

For Q4 2009, the Total Hotel Construction Pipeline for

Europ,

Middle East and Africa Stands at 1,373 Projects, a

Decline of 22% Since the Q2 2008 Peak

| March 5, 2010

Construction Pipeline Overview

Depleted by high cancellations and a late surge in New Openings, total Pipeline counts are in an end-of-cycle contraction. In 2009, total Cancellations/Postponements in EMEA removed nearly 96,000 rooms from the Pipeline. As the lending environment is not expected to rebound any time soon, Cancellations/Postponements will likely remain high for the near-term. New Hotel Openings coming online as additional supply will stay at an elevated rate, particularly in the Middle East and Africa, where New Openings will accelerate through 2011. Meanwhile, New Project Announcements (NPAs) into the Pipeline, which have been in a low channel for four consecutive quarters, are expected to remain at these low levels, which are far from sufficient to offset declining Pipeline trends.

Europe

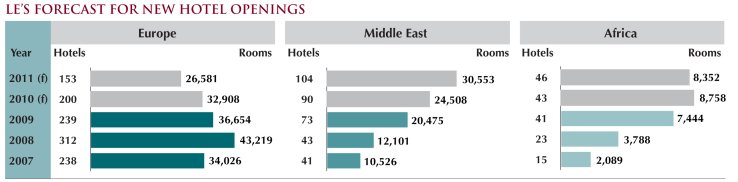

The lack of available financing continues to impact both the rate of project migration up the Pipeline towards construction and the flow of NPAs into the Pipeline. Both Construction Starts and NPAs remain in a low channel in Q4 and will stay that way, as the availability of lending is not expected to change in the near future. Projects that are able to obtain financing are mostly smaller-sized. Construction Starts for the quarter average just 160 rooms. 85% of Construction Starts and 89% of NPAs have already selected a brand, as the marketing and operating benefits of a brand are increasingly compelling to developers and lenders. A total of 239 new hotels/36,654 guest rooms opened in 2009. New Hotel Openings are forecast to remain historically high in 2010 with 200 hotels/32,908 rooms coming online. In 2011, New Openings are projected to decrease to 153 hotels/26,581 rooms, reflecting the ongoing contraction of total Pipeline counts. This downward trend will continue going forward as Pipeline totals decrease further. Middle East

Along with difficulties in sourcing financing, decreases in room demand and even deeper declines in room rates are keeping NPAs in a low channel, accelerating Pipeline count declines and signaling the end of this development cycle. Now nearing the back end of the cycle, projects that are smaller and those associated with a brand are becoming more attractive to developers. 53% of total NPAs in Q4 are 200 rooms or less, with a growing 68% already having chosen a brand. Cancellations and Postponements remain at an elevated rate, particularly for larger projects and those without a brand. 54% of projects cancelled or postponed in Q4 are larger than 250 rooms, with 5 cancelled projects having 600 rooms or more. Over half of Q4�s cancellations/postponements have no brand affiliation. 73 hotels with 20,475 rooms opened in 2009. With 51% of total Pipeline projects and 55% of rooms now Under Construction, New Openings will ramp up through 2011, causing new supply to grow at an increasing rate. 90 new hotels/24,508 rooms are forecast to open in 2010, then 104 hotels/30,553 rooms will enter as new supply in 2011. Thereafter, New Hotel Openings will begin to taper off as a result of the shrinking Pipeline. Africa

ABOUT LODGING ECONOMETRICS

|

| Contact:

Jen Robertson, Marketing Manager

|

| Also See: | LE�s Initial Forecast for 2009 Predicts that 1,354 Hotels with 159,368 Rooms Will Open in the U.S.; Private Equity Makes a Big Splash in the Lodging Industry / July 2007 |