|

Still a Dealmaker�s Paradise The Upper-Upscale Sector Elbows

. |

HOSPITALITY RESEARCH + CONSULTING SPECIALISTS |

|

|

|

Still a Dealmaker�s Paradise The Upper-Upscale Sector Elbows

. |

HOSPITALITY RESEARCH + CONSULTING SPECIALISTS |

| Summer 2007

Deal Pace Remains Strong through

the First Half of 2007

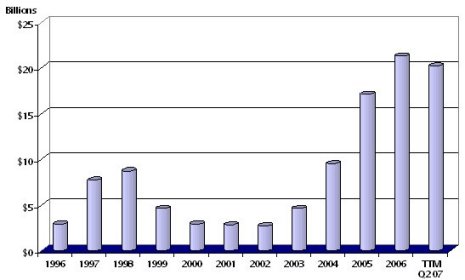

The question inevitably arises during each conference as to which inning the current hotel investment cycle is in. The common answer seems to be �around the sixth or seventh inning� nowadays. Regardless, one thing is for sure: companies are still swinging their bats hard as they compete for new acquisitions. The transaction environment for upscale and luxury hotels and resorts is still highly active through the first half of 2007. In the first and second quarters, 177 properties changed hands, an increase over the 158 transactions that occurred in the first half of 2006. The deal volume over the past twelve months remains just slightly below that of calendar year 2006, but still above 2005 levels. With numerous deals already anticipated for the third quarter, we expect the deal-making landscape to maintain a robust level of activity through the end of 2007. While the number of properties sold has increased year over year, the

dollar volume of transactions declined from $13 billion in the first half

of 2006 to $11.6 billion in the first half of 2007. The volume of transactions

generally is lighter in the second half of the year. Thus, we project upscale

and luxury deal transaction volume to end 2007 just shy of $20 billion.

As we illustrated during the first quarter, the average deal size has returned to a more �normal� level since 2006. The average transaction in early 2007 was $65.5 million, while the average deal in early 2006 was a record $82.3 million. U.S. Upscale & Luxury Lodging Transactions

The average price per room has declined slightly over the past year, but remains well above historical levels. This is largely due to fewer property trades involving residential conversions or developments, which has driven pricing upwards in recent years. The average price per room in the first half of 2007 was $228,000. Average price per room peaked at a record $240,000 in 2006. We anticipate the average price per room to decline slightly over the latter half of 2007, ending the year just above $220,000 per key. U.S. Upscale & Luxury Lodging Facilities

The Battle for Upper-Upscale Domination Much has been said about the growth in the luxury sector, with Mandarin Oriental, Shangri-La, and Trump expanding in major cities and resort destinations, and new brands like 1, Andaz, Capella, and Solis set to enter the stage. However, the sector that is poised for the most growth over the next few years is the upper-upscale tier, properties positioned between the luxury brands of Ritz-Carlton and Four Seasons and the mainstream upscale chains of Hilton, Marriott, and Sheraton. The upper-upscale hotels are positioned as a more refined, somewhat hip alternative to the more traditional upscale brands, without the stuffiness of the high-end luxury hotels. The segment between upscale and luxury has historically been ambiguous,

with Hyatt Regency and Westin, as well as some of the higher quality Hiltons

and Marriotts, filling the gap. Now there are numerous brands catering

to the segment. Over the past few years, InterContinental, JW Marriott,

Omni, Renaissance, Westin, and W have expanded their presence domestically.

Other upper upscale brands, including Le Meridien and Marriott�s new lifestyle

concept, will also spur growth in the segment over the next decade. Below

is a snapshot of the existing upper-upscale supply offering plus new additions

currently in the pipeline. Westin, W, Renaissance, and InterContinental

are each poised for significant growth through 2010.

Source: Hospitium When Select-Service Hotels Hit the City Moderate-Tier Properties Are a Different Animal When They Go Downtown In the suburban areas, select-service hotels are often viewed as ankle-biters by the full-service properties. In most cases, these properties cannot be distinguished from one market to the next. However, in downtown areas, the competitive environment is different. Select-service hotels in downtown locations tend to divert from the homogenous, prototypical designs that dot the suburban landscapes. Most are constructed to a higher standard, and blend in with the surrounding downtown buildings. Over the past several years, many historic buildings have been redeveloped into hotels that fly moderate-tier flags. While for the most part these hotels have the standard in-room amenities, their building structures provide more unique settings that are frequently more appealing to guests than their modern full-service competitors. CSM Lodging, First Hospitality Group, Historic Restorations, Kimberly-Clark, and Sage Hospitality Resources have each been involved in numerous historic conversion projects that include moderate-tier hotels. It is not uncommon for select-service properties in downtown locations to perform as well as, or even outperform, their full-service counterparts in terms of occupancy and average rate. Some select-service hotels have performed so well that they are being repositioned and re-flagged with upscale monikers. The Courtyard Milwaukee Downtown at the Depot recently converted to a Renaissance and the Hampton Inn & Suites Dallas West End is in the process of converting to a Doubletree. Generally, the select-service properties offer most of the same requisite

amenities. Some offer free internet access and complimentary continental

breakfast as well, which are key attractions for price-sensitive or budget-oriented

travelers. And guests still receive their frequent guest points, whether

they stay at the Hilton, the Hilton Garden Inn, or the Hampton Inn.

Four Points Historic Savannah (left) is vastly different from the current Four Points prototype (right). Renderings Courtesy of Startwood Hotels & Resorts Worldwide . As the market segment�s name suggests, focused-service is focused on filling rooms to generate revenue and profits. Certainly, these hotels do not produce the income streams of a full-service property in terms of restaurant, banquet, and other ancillary revenues, but they have several advantages in terms of profitability. With a significant amount of unique local dining options in close proximity

to downtown hotels, a select-service hotel is not disadvantaged by limited

in-house food service. In downtown locations, a restaurant within a hotel

is often overlooked as most clientele prefer to sample the local cuisine

at nearby restaurants. In full-service properties, running a typical three-meal

restaurant can be a drain on resources and profits.

And regardless of the market, prospective clientele will always perceive select-service hotels as good values for accommodations. This is particularly beneficial in during economic downturns. As exhibited between 2001 and 2004, the moderate-tier hotels benefited from the trickledown effect as travelers become more price-sensitive, shifting their preferred accommodations from upscale properties to more value-oriented hotels. Certainly, owning a focused-service hotel may not have the same cachet as owning a full-service property downtown. Nevertheless, there is something to be said for the risk limitations that a strong brand with a rooms-only focus and a high customer appeal can deliver in a primary urban location.

Hospitium is a hotel consulting firm that specializes in the upscale and luxury sectors of the lodging industry. From the early stages of development or deal negotiation through asset disposition, Hospitium delivers timely and useful research, analysis, and insight that assist the various needs of owners, developers, management companies, and financial institutions. Hospitium provides a wide array of advisory services and products, including feasibility studies, due diligence, underwriting, strategic planning, development consulting, and transaction guidance.

Data and information for the Lodging Ledger is collected by Hospitium, LLC. Hospitium, LLC is merely a conduit for the data, and assumes no responsibility or liability for its accuracy, usability, confidentiality, or other matters related to this publication. Information herein is believed to be reliable and has been obtained from sources believed to be reliable, but its accuracy and completeness cannot be guaranteed. Use of the data herein may not be resold, distributed or otherwise utilized for commercial use or profit without the expressed written consent of Hospitium, LLC. |

| Contact:

Hospitium, LLC

|

| Also See: | The Lodging Ledger / Investors Flock to Hotels!!! / The Looming Baby Boomer Impact / Steve Hennis / April 2007 |

| The Lodging Ledger / Skyrocketing Transaction Volume and Pricing / Investment Timing is Key / Steve Hennis / February 2007 | |

| The Lodging Ledger / Hotel Deals Continue to Roll Along, The Allure of Luxury Lodging Assets, The Next Wave of Mega-Resorts / Steve Hennis / October 2006 |

Stephen

Hennis has over thirteen years of experience in the analysis of lodging

investments. He has appraised and evaluated over 500 lodging facilities,

and has been involved in the underwriting, negotiation, and acquisition

of over $400 million in luxury hotels and resorts. Prior to becoming Managing

Director of Hospitium, Mr. Hennis served as Vice President of Hospitality

Investments for Lowe Hospitality Group and Destination Hotels & Resorts

where he was involved with acquisitions, dispositions, and development

projects. Mr. Hennis previously served as Vice President and Director of

Research for HVS International where he specialized in the analysis and

valuation of large portfolios for cross-collateralized securitizations

and oversaw the redevelopment of HVS� analytical models and report templates.

He has also worked for Marriott International and Caesars World. Mr. Hennis

is a graduate of the University of Denver�s School of Hotel, Restaurant

& Tourism Management.

Stephen

Hennis has over thirteen years of experience in the analysis of lodging

investments. He has appraised and evaluated over 500 lodging facilities,

and has been involved in the underwriting, negotiation, and acquisition

of over $400 million in luxury hotels and resorts. Prior to becoming Managing

Director of Hospitium, Mr. Hennis served as Vice President of Hospitality

Investments for Lowe Hospitality Group and Destination Hotels & Resorts

where he was involved with acquisitions, dispositions, and development

projects. Mr. Hennis previously served as Vice President and Director of

Research for HVS International where he specialized in the analysis and

valuation of large portfolios for cross-collateralized securitizations

and oversaw the redevelopment of HVS� analytical models and report templates.

He has also worked for Marriott International and Caesars World. Mr. Hennis

is a graduate of the University of Denver�s School of Hotel, Restaurant

& Tourism Management.