|

Skyrocketing Transaction Volume and Pricing

|

HOSPITALITY RESEARCH + CONSULTING SPECIALISTS |

|

|

|

Skyrocketing Transaction Volume and Pricing

|

HOSPITALITY RESEARCH + CONSULTING SPECIALISTS |

| Winter 2007

The Sky is the Limit

Close to $40 billion in upscale and luxury assets have traded over the

past two years. The low cost of capital, strong operating results,

a highly competitive deal environment, and residential conversion economics

have driven the lodging industry into a new investment era over the past

couple of years. A total of 262 properties traded in 2006, down slightly

from the record 299 assets that traded in 2005.

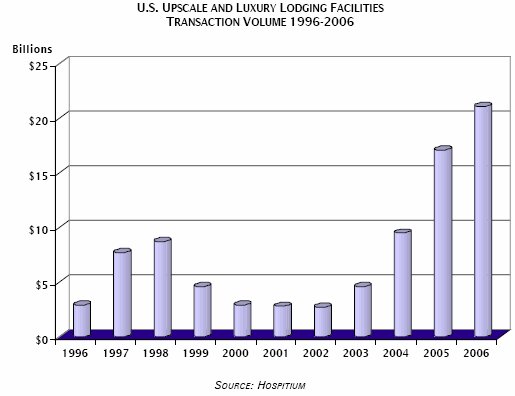

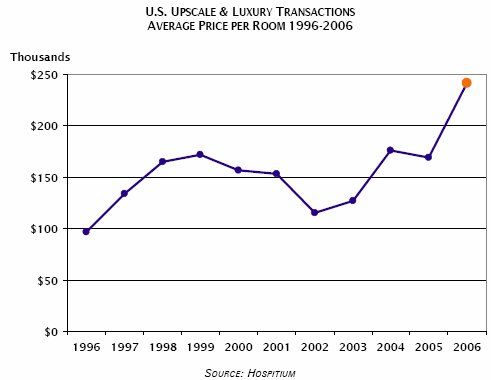

The Fairmont Scottsdale Princess was one of the largest transactions in 2006 Photo Courtesy of Fairmont Raffles Hotels International Nevertheless, more than $21.2 billion in upscale and luxury lodging facilities changed hands last year, up from the $17.1 billion in transactions in 2005. With several deals already in the pipeline for 2007, there does not appear to be any slowdown in the near future. The upscale and luxury transaction environment is anticipated to remain robust for at least the next 12 to 18 months, if not longer. .  With demand for high-quality assets still brimming, prices continue to climb. The investment appetite for upscale and luxury products has pushed pricing into uncharted territory. The average price per room skyrocketed from $169,000 in 2005 to $242,000 in 2006, a record price point. Three years ago, many analysts expressed concern about overpriced assets and unjustifiable cap rates. However, many assets that traded hands just a couple years ago look like bargains today. Asset pricing is expected to remain strong over the next two years as the amount of available product on the market is unable to satisfy the mass of capital allocated for upscale and luxury lodging investments. .  .

Price per Room

. The Hotel del Coronado also drew the highest overall sale price at $745

million. The sales of the Drake Swissôtel New York and the Westin

St. Francis in San Francisco tied for second position with each hotel trading

for $440 million. The top ten largest transactions in 2006 accounted for

almost $4 billion in acquisitions, and were evenly split between resort

properties and urban hotels.

Sales Price

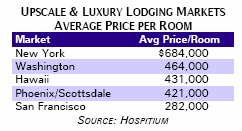

Among the major cities, New York maintained its top price-per-room ranking with transactions averaging $684,000 per unit. Washington DC, Hawaii, and Phoenix/ Scottsdale also posted strong per-room values between $421,000 and $464,000. In comparison, San Francisco hotels appeared to be a bargain at $282,000 per room. While the outstanding performance of the New York hotel market is one factor that has driven pricing upward, the primary factor is the highest and best use. The returns on residential real estate in New York are rather enticing, and many hotels are trading based on non-lodging economics. Consequently, thousands of hotel rooms in the city are being converted to condominiums. Upscale and luxury rooms supply in Manhattan is actually shrinking because of the condo conversion phenomenon.

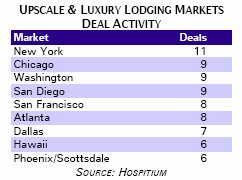

It is no surprise that primary urban and resort locations possessed the most sought-after assets. With funds geared specifically towards core assets that typically retain their inherent real estate value, this trend will continue. New York experienced the most investment activity last year, with eleven properties gaining new owners. Chicago, San Diego, and Washington each had nine properties change ownership. Atlanta and Dallas, two major metropolitan areas that have been slightly behind on the recovery curve, piqued the interest of buyers in 2006 as the lodging markets appeared to exhibit greater upside opportunities. The ever-increasing price tags for lodging assets will naturally cause capital placement to shift from acquisitions to development. As prices reach replacement cost levels, development may become a more attractive opportunity for investors over the long term. However, development is not without its risks. Future market uncertainty, everincreasing construction costs, and the lack of immediate cash-on-cash returns prompt most companies to prefer the cash-flowing assets that are on the market today. Loews Hotels originally planned to build a new $200-million resort at Lake Las Vegas, but opted to buy and convert the Hyatt Regency Lake Las Vegas instead. Photo Courtesy of Loews Hotels. Timing is Everything Shoulda, coulda, woulda. How many hotel investors have looked back on the past few years thinking �If only we had bought that property back in 2002 or 2003�?� The clichés are abundant regarding 20/20 hindsight. A recovery of the lodging industry was predictable following the national recession and the attacks of September 11th, but few, if any, could have predicted the surge in asset values that has occurred over the past five years. The pending sale of CNL Hotels & Resorts� assets is of particular note here. Between 2000 and 2003, CNL was the top buyer of upscale and luxury hotels primarily because they had relatively inexpensive equity compared to most buyers at the time. CNL became the subject of much criticism as their acquisitions appeared to be above market pricing. In 2005, the company was unable to successfully execute an IPO and naysayers touted �I told you so.� However, as the hotel investment market has boomed, so did the value of CNL�s assets. Whether or not CNL overpaid for properties in the early 2000s is now irrelevant. However, the fact that they are now selling their assets for a big gain is a testament to the current state of lodging investments. While CNL is the most obvious owner to have benefited from the current

market dynamics, numerous other companies have flipped assets after only

a short hold period. The annual appreciation of assets is well illustrated

by several property transactions that occurred in 2006.

Short - Term Holds

Lincoln Suites, Westin Chicago Michigan Avenue, Hotel del Coronado, Radisson Suites Marco Island, Pan Pacific San Francisco Conrad Chicago, Hilton Pasadena The 3 R�s of Upside Come at a

Big Price

While the amount of capital spent acquiring assets in 2006 is impressive, the money that new owners need to invest in their new properties is nearly as striking. More than $2.5 billion will be invested in upgrades, renovations, and expansions to the properties that traded in 2006. On average, $30,000 will be spent on each room that changed ownership in 2006. That brings the average per room investment to $272,000 for upscale and luxury lodging assets acquired last year. In our analysis of post-acquisition renovation plans, we discovered that roughly 25% of acquisitions in 2006 required very little additional capital to address deferred maintenance, brand requirements, or on-going renovations. However, some owners are spending as much as $100,000 per key to reposition their hotels. Noble Investment Group and AEW Capital Management teamed on the purchase of the Sheraton Colony Square in Atlanta, Georgia. They plan to spend roughly $107,000 per room to turn it into the W Atlanta Midtown. ING Clarion and Kimpton joined forces to acquire the Holiday Inn Select in Alexandria, Virginia, and are spending approximately $97,000 per room to convert it to the Hotel Monaco Alexandria. Property Improvement Plans (PIPs) usually account for a significant

amount of the capital invested in a new acquisition. Millions of dollars

are typically spent maintaining or upgrading to current brand standards.

For properties that retained their existing brand, new owners invested

$19,500 per room on average for 2006 acquisitions. For hotels converting

to a new brand, the cost averaged roughly $41,000 per key.

JER Partners plans to give the Stanford Court Renaissance in San Francisco a $32 million facelift ($81,500 per room) to be completed by mid-2008. Photo Courtesy of Marriott International. Additional Capital per Room  Sheraton Altanta Midtown Colony Square, Holiday Inn Select Alexandria, Pointe South Mountain, Hyatt Regency Newport, Hyatt Regency Islandia

Hospitium is a hotel consulting firm that specializes in the upscale and luxury sectors of the lodging industry. From the early stages of development or deal negotiation through asset disposition, Hospitium delivers timely and useful research, analysis, and insight that assist the various needs of owners, developers, management companies, and financial institutions. Hospitium provides a wide array of advisory services and products, including feasibility studies, due diligence, underwriting, appraisals, and strategic planning.

Data and information for the Lodging Ledger is collected by Hospitium, LLC. Hospitium, LLC is merely a conduit for the data, and assumes no responsibility or liability for its accuracy, usability, confidentiality, or other matters related to this survey. Information herein is believed to be reliable and has been obtained from sources believed to be reliable, but its accuracy and completeness cannot be guaranteed. Use of the data herein may not be resold, distributed or otherwise utilized for commercial use or profit without the expressed written consent of Hospitium, LLC. |

| Contact:

Hospitium, LLC

|

.

Stephen

Hennis has over thirteen years of experience in the analysis of lodging

investments. Prior to becoming Managing Director of Hospitium, Mr. Hennis

served as Vice President of Hospitality Investments for Lowe Hospitality

Group and Destination Hotels & Resorts. During his tenure at Lowe,

he was involved in the underwriting, negotiation, and acquisition of over

$400 million in luxury hotels and resorts. Mr. Hennis previously served

as Vice President and Director of Research for HVS International where

he specialized in the analysis and valuation of large portfolios for cross-collateralized

securitizations and oversaw the redevelopment of HVS� analytical models.

At HVS, Mr. Hennis appraised and evaluated over 500 lodging facilities.

Mr. Hennis is a graduate of the University of Denver�s School of Hotel,

Restaurant & Tourism Management.

Stephen

Hennis has over thirteen years of experience in the analysis of lodging

investments. Prior to becoming Managing Director of Hospitium, Mr. Hennis

served as Vice President of Hospitality Investments for Lowe Hospitality

Group and Destination Hotels & Resorts. During his tenure at Lowe,

he was involved in the underwriting, negotiation, and acquisition of over

$400 million in luxury hotels and resorts. Mr. Hennis previously served

as Vice President and Director of Research for HVS International where

he specialized in the analysis and valuation of large portfolios for cross-collateralized

securitizations and oversaw the redevelopment of HVS� analytical models.

At HVS, Mr. Hennis appraised and evaluated over 500 lodging facilities.

Mr. Hennis is a graduate of the University of Denver�s School of Hotel,

Restaurant & Tourism Management.