|

|

|

|

|

|

|

|

Growth Projections |

| By Jeffrey H. Walker, MAI, CHME, April 2004

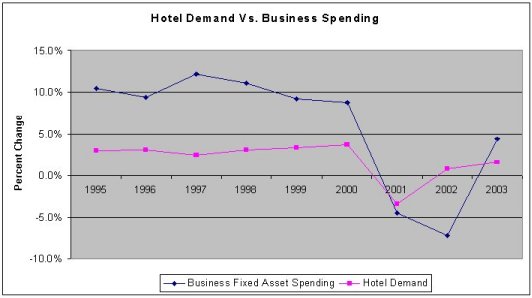

Within the hotel community, there is finally a sense that demand may be turning the corner. But the optimism is still somewhat cautious, as several previous predictions of increasing demand since 9/11 have failed to fully materialize. To get a clearer picture of future trends, USRC has analyzed historical hotel demand increases in relation to historical levels of business fixed asset investment, as tracked by the U.S. Bureau of Economic Analysis. In general, during periods of economic recession, corporations cut costs in order to protect bottom-line profits in a weakening sales environment. Historically, corporate travel, including travel to conventions and corporate meetings, is one of the first expenses cut in a slowing economy. During an expanding economy, corporations invest in future profits by increasing sales, marketing, and training, which includes increased business travel. Similarly, corporations have similar spending habits on long-term fixed investments in such items as computers, software, infrastructure, and buildings. Thus, the demand for corporate travel, as well as group and convention demand for hotels often mirrors the statistical data on corporate fixed investment. The following chart presents the historical change in business fixed

investment. As presented, during a period of rapid increases in full-service

hotel demand (the late 1990�s) corporate fixed investment saw very strong

growth. Similarly, during one of the worst downturns in the hotel industry

for groups and conventions, corporate investment shrunk.

The following chart graphically demonstrates the relationship between historical demand changes, according to Smith Travel Research, and the above business fixed asset investment changes.

In general, hotel demand has closely tracked trends in business fixed asset investment, with hotel demand experiencing more moderate fluctuations. In 2002, hotel demand recovered somewhat quicker than fixed asset investment, but the trend returned to normal in 2003. The historical business investment picture becomes clearer when looking

at the historical data on a quarterly basis. As demonstrated in the chart

below, despite only modest growth in 2003 on a calendar year basis, business

investment dramatically increased throughout 2003, after negative trends

in 2002.

The advantage of establishing this relationship is the availability

of projections for changes in business fixed asset investment. The following

table presents projected changes to business asset spending for the next

two years by quarter, according to the Mortgage Bankers Association.

As indicated, the association projects double-digit growth in business fixed asset investment for the next five quarters, rivaling or exceeding the growth experienced during the hotel expansion years of 1995-1998. If the relationship holds true, hotel demand should be "pulled up" by the dramatic rise in business investment, and hotel demand increases in the late 1990�s range of 3.0 � 5.0% should be achievable for the next 12 � 18 months. Coupled with the projected slower increase in supply, these demand increases provide a strong indicator of an environment of increased occupancy and, with increased compression in many markets, increasing ADR. As hotels continue to focus on expense control, this improving top-line environment should lead to strong flow-through to the bottom line, with a result of healthy improvement in hotel profitability. Jeffrey H. Walker, MAI, CHME, is Director of Hospitality Services for US Realty Consultants� corporate office in Columbus, Ohio. The company has offices in Chicago, Atlanta, and Cleveland, and will soon be expanding to West Palm Beach. He can be reached at 614-221-9494 (ext. 127), or at [email protected]. |

Jeffrey H. Walker, MAI, CHME Director of Hospitality/Appraisal Services US Realty Consultants, Inc. Corporate Headquarters 492 South High Street, Suite 200 Columbus, Ohio 43215 614-221-9494 ext. 127 (phone) 614-221-9941 (fax) [email protected] http://www.usrc.com |

| Also See | Hotel Capitalization Rates Drop Again / David J. Sangree, MAI, CPA, ISHC / April 2004 |

| Hotel Capitalization Rates Drop / David J. Sangree, MAI, CPA, ISHC / February 2003 | |

| Appraisal and Financing of Indoor Waterpark Resorts / David J. Sangree / October 2003 | |

| The Effect on Capitalization Rates and Discount Factors After September 11 / Canadian Lodging Outlook / Dec 2001 | |

| Will Hotel NOIs and Property Prices Follow Revenues in Their Downward Spiral? / John (Jack) B. Corgel, Ph.D / Hospitality Research Group of PKF Consulting / June 2002 |