![]()

Will Hotel NOIs and Property Prices Follow

Revenues in Their Downward Spiral?

![]()

Will Hotel NOIs and Property Prices Follow

Revenues in Their Downward Spiral?

| By John (Jack) B. Corgel, Ph.D

Each week the hotel industry anxiously awaits the release from Smith Travel Research of room revenue numbers for thousands of U.S. properties. Interest in these reports reached new highs during recent months as the private and public markets continually monitor industry performance during the recession and following the events of September 11th. Through the fourth quarter of 2001 room revenues remain well below levels achieved during the same weeks of 2000. The availability of timely revenue information represents a large first step toward understanding how hotel property returns have held up under current economic pressures. Nevertheless, these data may be somewhat misleading about the severity of hotel market softness from a capital market perspective. While the share prices of franchise and management giants in the hotel industry (e.g., Marriott International) vary directly with movements the top of hotel property income schedules, equity and debt capital suppliers have more of a steak in the bottom-line incomes and property valuations. Unfortunately, timely information about hotel NOIs and property values is far less available to the capital markets than are the revenue numbers to franchise and management interests. At a minimum, the shortage of information about hotel NOIs and values make hotel capital more expensive than it would be if the risks could be analyzed more completely. In the extreme case, these information problems could lead to an inefficient allocation of capital to hotel property investment. Translating Revenue to Net Income Hotels have known systematic risks. The income elasticity of demand for hotel rooms exceeds 1.0 meaning that hotel rooms trade as luxury goods. With firm and household budgets strained, expenditures on travel will be deferred, reduced, or eliminated. Hotels also have extremely high expense ratios. While the expense ratio of an investment grade office property is less than 50 percent, full service hotels have 70 percent expense ratios. The large and highly complicated expense schedules of hotels, especially full-service hotels, elevates the degree of difficulty in converting changes in revenues to changes in NOI. Translating hotel revenues to net income is meaningful to capital market participants for the following reasons:

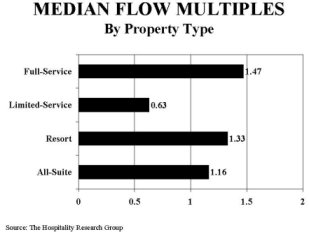

Because many hotel expenses vary with occupancy, falling occupancy reduces expenses along with lower revenues. Some hotel owners and managers during this recession have chosen to exercise their put option to close down floors, sections, and even entire properties in an all-out assault on variable expenses. Hotel NOI generally have been bolstered by lower labor costs which constitute about 40 percent of the expenses in a typical full-service hotel. The late 1990s was an era of strong revenue growth accompanied by employment growth in many hotels. Some of these employees are no longer necessary and thus have received involuntary separation notices. The wage pressures felt by hotel management in recent years have totally disappeared. Also, hotel owners are beginning to challenge property tax assessments in the shadow of the recent declines in revenues. Fixed expenses may actually increase however since saving in property taxes will be more than negated by increasing insurance premiums. Go With the Flow An important performance statistic for analyzing NOI impact from falling revenues is the �flow-through� ratio. As defined below, flow through represent the NOI elasticity with respect to revenues. Flow-Through Ratio = Percent Change in NOI / Percent Change in Revenue Flow-through ratios depend on the relationship between revenue growth and expense growth. Revenue shifts create larger shifts in NOI as revenue growth rates diverge from expense growth rates. The extent of the NOI shifts is determined by the profit margin of the hotel. Full-service hotels with lower profit margins have higher flow-through ratios than limited-service hotels with higher profit margins. Using financial statement data managed by the Hospitality Research Group (HRG) for thousands of hotels during the period 1959 to present, we calculated the median flow-through ratios. The results are as follows:

The conventional wisdom based on barriers-to-entry arguments suggests that limited-service hotels are far riskier than resort and full-service hotels. Historical flow-through ratios indicate that the same percentage change in revenues will produce much larger percentage change in resort, all-suites, and full-service hotel NOIs than limited-service hotel NOIs. Revenue Changes and Property Prices All real estate suffers from the same problem with respect to understanding the dimensions of capital loss due sudden negative shifts in revenues. The problem stems from the non-continuous nature of asset trading. Hotel investors have struggled during recent months to understand how property prices are reacting to the one-two punch of recession and air-travel stigma. The search for answers leads in the following three directions:

Parameters of a capitalization rate forecast model produced by HRG and Torto Wheaton Research indicate that hotel revenue changes are mostly reflected in capitalization rates in six months. Thus, hotel property price effects should begin showing up in transactions during the first two quarters of 2002. Recent hotel transactions have not reflected strong downward movements, although some of these transactions were negotiated prior to September 11th. Final Comments The trend for hotel revenues continues to be negative across most areas of the U.S. and all property types. Revenue declines will translate into lower NOIs and property prices, but by varying magnitudes and with some delay. Resort and full-service hotels in major markets are experiencing the most financial pain during this recession. Revenues have fallen sharply due in part to air travel dependency. Unfortunately, the NOIs of full-service and resort hotels are quite sensitive to revenue changes. Real estate price discounts should begin to appear by mid-2002, especially if the economy does not show signs of recovery during first and second quarters of 2002. John (Jack) B. Corgel, Ph.D is Managing Director of Applied Research for the Hospitality Research Group of PKF Consulting. He is located in the firms' Atlanta office. This article is based on an adaptation of an article that appeared in Real Estate Issues, published by The Counselors of Real Estate, Vol.26, no.4, pp.71-73. Used with permission of Real Estate Issues. |

|

Robert Mandelbaum at the firm: email [email protected] PKF Consulting 3391 Peachtree Road Suite 420 Atlanta, GA 30326 phone (404) 842-1150 fax (404) 842-1165 |