advertisement

Giving And Taking of Credit at U.S. Hotels

|

News for the Hospitality Executive |

advertisement

Giving And Taking of Credit at U.S. Hotels

|

By:

Robert Mandelbaum and Alvin Minsk

April 20, 2012 From 2008 and 2009, the average U.S. hotel suffered a 13.2 percent decline in occupancy along with a 5.9 percent drop in average daily rate (ADR). During this period, hotel managers were challenged to find tactics that maximized revenue for their hotels. On the sales side, adjusting room rates and experimenting with distribution channels garnered the most attention. However, back in the accounting offices of U.S. hotels, decisions had to be made regarding the offering of credit to potential guests. On the one hand, loosening credit requirements may ease the way for certain groups to stay at a hotel. On the other hand, the risk of default on the credit extended to guests is greater during difficult economic times. To understand how hoteliers balanced the benefits and risks of offering credit during the great recession, PKF Hospitality Research (PKF-HR) analyzed the Provision for Doubtful Accounts and Credit Card Commissions line items reported on the operating statements of 2,200 U.S. hotels during the period 2007 through 2010. This data comes from PKF-HR’s annual Trends® in the Hotel Industry survey. Additional assumptions were made using information from the following sources:

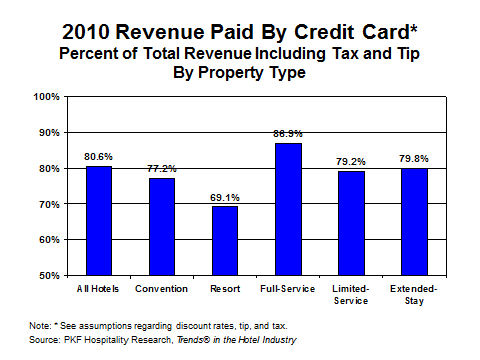

According to the Uniform System of Accounts for the Lodging Industry, Provision for Doubtful Accounts is used to track changes made to provide for the probable loss on accounts and notes receivable. Each month, hotel managers estimate the portion of their property’s receivables that they do not believe will be collectible. Due to the sudden onset of the economic downturn, it appears that hotel managers feared a rise in uncollectable accounts. On average, the hotels in our sample increased their Provision for Doubtful Accounts by a strong 38.7 percent from 2007 to 2008.  As the economy and lodging industry improved in 2010, Provisions for Doubtful Accounts continued to decline, both in terms of dollars and as a percent of total revenue. In fact the $25.37 per-available-room (PAR) average Provision for Doubtful Accounts reported in 2010 is less than the $34.51 PAR allocated to this expense item during the prosperous year of 2007. In general, all property types and chain scales followed the same pattern of annual changes in Provisions for Doubtful Accounts. The exceptions were resort hotels and luxury properties which continued to allocate more to Provision for Doubtful Accounts through 2009. Financial services firms were some of the hardest hit during the initial stages of the recession, and these companies are major demand sources for luxury and resort properties. More Credit Through Plastic Another factor contributing to the lessening of bad debts is the increased use of credit cards. Credit Card Commission payments measured as a percent of total revenue increased each year from 2007 (2.01% of total revenue) to 2010 (2.2%). An increase in this Credit Card Commission ratio was observed across all property types and all chain scales. The lone exception was economy properties which have the highest percentage of cash transactions.

Throughout the analysis period, the greatest percentage of revenue was paid for with credit cards at full-service hotels. Most full-service hotels in the survey sample operate in the upper-upscale and upscale categories and rely on individual corporate and leisure transient business. The credit card payment ratio was consistently the lowest at convention and resort hotels. Convention hotels accommodate large groups that are frequently approved for directly billing. Resort hotels also rely on large groups, as well as incentive travel and travel agents, all of which are frequently direct billed. The Future Looking towards the future, we expect technology to play a role in the management of credit at U.S. hotels. The internet provides greater reach when evaluating the credit risk of a potential client. In addition, direct electronic methods of payments are becoming more prevalent. Managing technology abuses will have to be monitored, and basic credit control practices will need to be followed. However, it should be easier to ensure payment and lower bad debts in the future. This article is copyright protected by Hotel-Online. Reuse by other media or news outlets or organizations is prohibited without permission. Personal use and sharing via social media tools is encouraged.  Robert Mandelbaum, Director of Research Information Services, and Alvin Minsk, Annual Trends® Supervisor, both work in the Atlanta office of PKF-HR (www.pkfc.com). PKF-HR offers reports that allow owners and operators to benchmark the financial performance of a hotel to comparable properties (www.pkfc.com/benchmarker). This article was published in the March 2012 edition of Lodging. |

| Contact:

Robert Mandelbaum |