advertisement

Lodging Econometrics Report for Europe, Middle East and Africa Shows

Economic and Financing Concerns Impede Pipeline Project Migration

Saudi Arabia Emerging as a Development Hotspot

|

News for the Hospitality Executive |

advertisement

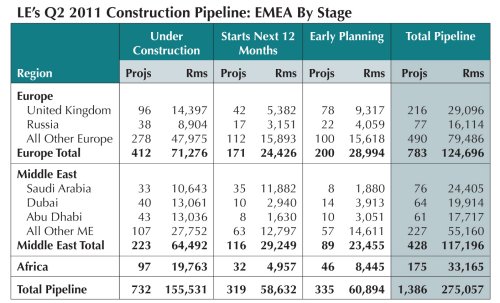

September 2011 - With

783 projects/124,696 rooms at the end of Q2, Europe’s Total

Construction Pipeline continues in a lower plateau.

After falling from their Q2 2008 peaks, most Pipelines in developed

countries

have been in a bottoming formation that started in 2010, where New

Hotel

Openings and Project Cancellations exiting the Pipeline have been

approximately

equal to New Project Announcements (NPAs) into the Pipeline. Sluggish

economies

and escalating sovereign debt problems are likely to more severely

restrict

lending in the months ahead, causing a deceleration in movement of

projects

already in the Pipeline towards construction, as well as creating a

fall-off in

NPAs. September 2011 - With

783 projects/124,696 rooms at the end of Q2, Europe’s Total

Construction Pipeline continues in a lower plateau.

After falling from their Q2 2008 peaks, most Pipelines in developed

countries

have been in a bottoming formation that started in 2010, where New

Hotel

Openings and Project Cancellations exiting the Pipeline have been

approximately

equal to New Project Announcements (NPAs) into the Pipeline. Sluggish

economies

and escalating sovereign debt problems are likely to more severely

restrict

lending in the months ahead, causing a deceleration in movement of

projects

already in the Pipeline towards construction, as well as creating a

fall-off in

NPAs.At 412 projects/71,276 rooms, 53% of Europe’s total projects are currently Under Construction, a high percentage not seen since Q1 2009. As such, New Hotel Openings exiting the Pipeline will remain elevated over the next two years. LE’s Forecast for New Hotel Openings projects 212 hotels/31,085 rooms to open in 2011, then 198 hotels/32,130 rooms in 2012. Then, Pipeline totals are expected to drift lower into mid-decade. After the Pipeline peaked in Q2 2008, the development surge in the Middle East declined rapidly and has settled into a bottoming formation over the last 6 quarters. The region’s Total Pipeline stood at 428 projects/117,196 rooms at the end of Q2. The sovereign debt crises in many countries and the attendant financing problems throughout the region caused a spate of project cancellations and continue to impede the migration of projects already in the Pipeline toward construction and, ultimately, opening. There are prolonged delays for projects already Under Construction and Scheduled to Start Construction in the Next 12 Months, with developers either unable to secure financing or simply not wanting to rush to completion in what has been a slow-to-recover operating environment. Many countries have a high percentage of their Total Pipelines already Under Construction, particularly Abu Dhabi, with an extremely high 74% of its Pipeline rooms Under Construction, and Dubai, with 66%. Despite delays, these projects should eventually open over the next two years. Thereafter, Pipeline totals will trend downward, as NPAs will be in a lower channel while markets work to absorb the next influx of New Supply. Saudi Arabia now has the largest Pipeline in the region, surpassing both Dubai and Abu Dhabi this quarter, with 76 projects/24,405 rooms. The Pipeline has been trending upward for 9 consecutive quarters and is up 49% by projects and 61% by rooms in just the last year alone. Quickly, the country’s Pipeline has become the 6th largest in the world by room count and the 11th largest by project count. In Q2, the Pipeline surged further due to rapidly escalating activity in the holy city of Makkah (for further details, please see the Spotlight section below). Riyadh, Jeddah, Madinah, and al-Khobar are additional hotspots seeing rising interest from developers and franchise/management companies looking to expand the presence of their brands in the country. At 175 projects/33,165 rooms, Africa’s Total Pipeline declined modestly due to an increase in New Openings during Q2. 55% of Africa’s Total Pipeline projects are Under Construction, which will result in rising New Openings over the next two years. LE’s Forecast anticipates a total of 39 new hotels/7,110 rooms to open in 2011, then a new cyclical high of 46 hotels/8,561 rooms in 2012. SPOTLIGHT: THE JABAL OMAR DEVELOPMENT PROJECT IN MAKKAH, SAUDI ARABIA In May, Jabal Omar Development Company signed multi-hotel agreements with three leading franchise companies, bringing a total of 12 new projects and over 6,500 rooms into the Pipeline in Makkah. Three of these projects went immediately Under Construction, while the others are Scheduled to Start Construction in the Next 12 Months. A total of 26 hotels are to be built as part of the massive 2.5 million square foot (230,000 square meters) mixed-use site being developed in the Jabal Omar area around the Grand Mosque. The $5.5 billion mega-project, which includes 39 towers for hotel, commercial and residential units, is reported to be one of the largest in the world in terms of hotel units.

|

| Contact: Lodging Econometrics |