Top Ten Thoughts

| 1. Loan Defaults

Uncertain and anxious over the economic downturn and impact of

9/11, hospitality industry lenders have virtually disappeared and hotel

financing has become notably scarce while nationwide delin-quency rates

on hotel loans doubled in the fourth quarter of 2001. Approximately

13% of hotel loans with collateral in the state of Florida were delinquent

at the end of 2001, many of them as a result of 9/11. Orlando in particular,

the largest hotel inventory in the state and second in the country after |

|

Top Ten Thoughts

1. Loan Defaults

2. Airport Expansions and Renovations

3. Convention and Conference Center

Expansions

4. Urban Revitalization

5. Cruise Industry Growth

6. Vacation Ownership

7. Condominium-Hotels

8. Native American Casinos

9. Environment

10. Cuba |

|

Las Vegas, accounts for the largest share of defaults in the nation, approximately

25%. Unlike the early 1990s, however, when hotel lenders consoled themselves

by fore-closing on troubled properties, lenders today are taking a different

approach and are working with borrowers and third party advisors to restructure

their loans and monitor the assets in hopes of reaching a solution. Delinquencies,

nonetheless, should continue in 2002 and are not expected to decline until

mid-year.

2. Airport Expansions and Renovations

To support growing levels of tourism visitation as well as corporate

travel, major airports in Florida are undergoing renovations and expansions

in excess of $4 billion. Despite the decline in passenger traffic across

the nation as a result of 9/11, the state�s airports are still moving forward

with short-term projects and expansion programs already underway. Long-term

projects have not been cancelled but many are under scrutiny and may be

deferred until passenger traffic picks up. A $400 million expansion project

is planned for the Tampa International Airport, $250 million of which is

currently underway with the remainder to be phased out over several years.

Orlando International Airport is currently engaged in a $1.2 billion expansion

including the construction of a fourth runway. Orlando�s passenger traffic

surpassed the 30 million mark in 2000 and its long-term expansion plans

are expected to increase capacity to 75 million passengers upon completion

in 15 to 20 years. Miami International Airport is currently under-going

a nearly $2 billion expansion program, which includes a fourth runway as

well as north and south terminal expansions with total completion anticipated

by mid-2006. The Fort Lauderdale International Airport is also executing

a $655 million expansion through 2004, as it anticipates that its 15.8

million-passenger level in 2000 will surpass 30 million by 2020.

3. Convention and Conference Center Expansions

Florida�s convention centers continue to expand to accommodate an ever-growing

demand for flexible convention space. An expansion of the Broward County

Convention Center, located in Fort Lauderdale, is currently underway, with

an additional 50,000 square feet of exhibit space to be delivered in February

2002. After 10 years of planning, construction of the $75 million, 350,000-square

foot Palm Beach convention center broke ground in June 2001 and is anticipated

to be completed by the fall of 2003. The expansion of the Orange County

Convention Center in Orlando will add approximately one million square

feet of exhibit space to the center by the end of 2003. Although no specific

plans have been announced, Miami is currently scrutinizing its fragmented

inventory and formulating a strategy to increase its competitiveness. Upon

completion of approximately 1.4 million additional square feet of convention

space, Florida should be poised to capture an increasing number of group

room nights during the next few years.

4. Urban Revitalization

As Florida�s suburbs become increasingly crowded and urban sprawl continues,

more efforts are being focused on redeveloping the downtown core of major

cities as a center of activity. The revitalization of Florida�s downtown

areas is drawing both tourists and businesses, as demonstrated by the success

of Las Olas Boulevard in Fort Lauderdale and Clematis Street and City Place

in West Palm Beach. In Jacksonville, the 966-room Adam�s Mark Hotel

is expected to serve as a catalyst for new development while in Daytona

Beach, the $250 million Ocean Walk Village redevelopment project is anticipated

to further enhance the destination. In Miami, the Heat�s American

Airlines arena has led the way for new real estate development including

the $334 million Performing Arts Center for the Miami Ballet, Opera, and

Symphony, to be built proximate to the Arena. Plans for a new baseball

stadium for the Florida Marlins are still under consideration despite initial

funding problems. Several other significant downtown mixed-use projects

are currently underway, including the Four Seasons Hotel & Tower, Espirito

Santo Plaza and the $1 billion Miami One development. Upon completion of

these developments, hotels planned for Florida�s downtown areas hope to

benefit from their location within walking distance of financial centers

during the day and supporting retail/entertainment establishments at night.

5. Cruise Industry Growth

In 2000 alone, passenger demand grew by 16.8% to a total of 6.9

million passengers, driven in part by an 11% increase in the number of

berths in state-of-the-art cruise ships. Moreover, the cruise industry

is anticipated to add approximately 50% additional capacity to the North

American market over the next five years. 2001, however, proved to be a

disappointing year for the industry as Port Canaveral�s passenger traffic

was down approximately 8% through August compared to the same period in

2000. The Port of Miami, on the other hand, experienced a

moderate 0.8% increase in passenger traffic during its 2001 fiscal

year, ended September 30. During September and October, however, the port

began experiencing signs of weakening passenger traffic compared to 2000,

posting declines of 12.5% and 17.6%, respectively. The decline was attributed

not only to weakening consumer demand but also to the loss of several cruise

liners seized by creditors. Although discounting techniques to lure back

passengers have resulted in bookings at or above the prior year levels,

they have cut into corporate revenues. Fortunately, the 2001 holiday season

experienced strong demand with bookings at or near 2000 levels in response

to lower rates. The rerouting of itineraries to leave from domestic ports

within easy driving distance from several markets also helped to bolster

demand post 9/11. Despite the failure of Ft. Lauderdale-based Renaissance

Cruises and the bankruptcy of Miami-based American Classic Voyages, a possible

merger of Royal Caribbean and P&O Princess Cruises would solidify South

Florida�s title as the world�s cruise capital, controlling approx-imately

80% of the world�s cruise capacity. Cruise industry professionals are bullish

on the globalization of the industry and key demand growth indicators.

As such, cruise demand is anticipated to gain momentum by late 2002 and

early 2003. Although the cruise industry lends minimal impact on the overall

lodging industry, it may present a direct threat to the leisure segment

and draw more guests away from resort destinations and theme parks.

6. Vacation Ownership

Vacation ownership companies continue to diversify into new products

and market segments. The industry has evolved from fixed weeks to floating

weeks and diverse point-based programs, offering greater flexibility to

owners. More affluent buyers also have their own selection of fractional

products, including independent and brand-affiliated resorts. Following

state-wide lodging trends, vacation ownership properties have experienced

lower occupancies after 9/11 and sales have declined during 2001 in response

to the recession and a decline in travel, which has impacted the level

of prospective consumers visiting properties. Orlando remains the timeshare

capital of the United States and Marriott�s Horizons mid-level product

is one of the latest additions to the city�s timeshare market. The Villas

at Disney�s Wilderness Lodge, a new themed product, opened this past winter

and Disney has already announced another vacation ownership resort, Disney�s

Beach Club Villas, scheduled to open in the fall of 2002, as well as plans

to convert a portion of the Disney Institute�s rooms to vacation ownership.

As major leisure markets in the United States become highly developed with

timeshare projects, it is possible that long-term cannibalization of hotel

products may occur.

7. Condominium-Hotels

Condominium-hotels, which many of us remember as a bold new concept

of the early 1980s, have resurfaced as a hot new development trend in Florida.

Particularly prominent in traditionally seasonal resort areas, this interesting

hybrid between investment and second home properties is becoming increasingly

popular from Miami Beach to the Florida Panhandle. These projects are expected

to remain attractive for developers seeking instant financing and to buyers

seeking help to defray mortgage costs for vacation properties. Conflicting

interests between developers and hotel operators, however, remain an ongoing

challenge. Condominium developers typically seek to minimize public space

and maximize living space, while hotel operators seek the opposite. Often,

developers focus on selling units and give little attention or regard to

the needs of the hotel operation. These conflicting interests result

in challenging development, marketing, and operating issues.

8. Native American Casinos

Floridians have repeatedly voiced their opposition towards legalizing

casino gambling in Florida. Their efforts, though, have not prevented the

Seminoles and Miccosukees, two Native American tribes, from establishing

as many as six gambling ventures in South Florida. The state, however,

considers their casinos to be illegal and infringing upon Florida Law,

as the tribes have not obtained a "compact," a license from the federal

government to open a casino on tribal land, to establish their operations.

While the issues remain unresolved, the Seminoles have partnered with the

Cordish Company to develop a $300 million, 750-room Hard Rock Hotel and

Resort in Hollywood anticipated to open by fall of 2003. In Tampa, a 250-room

Hard Rock Hotel and Casino is also anticipated to open by late fall of

2003, with a cost of more than $130 million. The purchase of a $28.7 million,

1,124-acre parcel in Osceola County in 2001 is yet another indication of

the tribe�s intent to establish another significant venture in the state.

9. Environment

The protection of the environment and the adverse impact that new and

existing development may have on Florida�s ecosystems are matters of concern

for officials and residents throughout the state. Fears of unplanned and

disorganized development, as well as new construction that may result in

regional ecological imbalances has led city executives to issue moratoriums

in Naples and The Keys to control urban sprawl. The Bush administration

is also using caution as it considers oil-drilling opportunities off the

Panhandle; Vice President Dick Cheney has suggested that the administration

would try to keep any new drilling about 100 miles from the state�s coast.

Florida also recently obtained an important win by having a $43.4 million

budget for beach restoration projects along the eastern shore approved

by the House of Representatives; the budget is $34.5 million more than

what was originally proposed by President Bush. Seasonal wild fires continue

to impact visitation to and within the state, as smoke from the blazes

force officials to close interstate highways and detour traffic to alternate

roads. Tampa�s Busch Gardens, for example, suspended operations of its

tour buses from Orlando in late February 2001 due to closed sections of

Interstate 4. Droughts throughout Central and South Florida may also adversely

impact tourism to the region as The Everglades become particularly dry,

diminishing the amount of observable wildlife and attractiveness of the

area.

10. Cuba

Despite former President Clinton�s efforts to loosen policy on Cuba,

further changes are not expected under the Bush Administration. The novelty

of a new and exotic destination that is 12 times as large as Puerto Rico,

has 4,000 keys, 100 miles of beaches and is only 90 miles away from Key

West is attracting many curious Americans and many more value-seeking European

tourists. Cuba, however, faces numerous challenges, including weak infrastructure

and a lack of hotel and airlift capacity relative to well-established destinations

in Florida and the Caribbean. Furthermore, a history of human rights issues,

labor practice violations, a communist controlled economy and a lack of

hard currency suggest that this island nation still has a long way to go

to position itself as a competitive Caribbean destination.

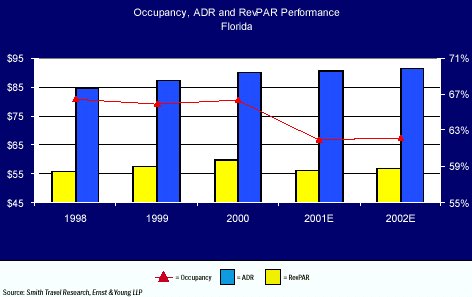

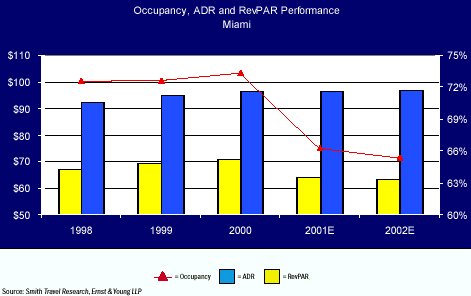

While the Miami area exhibited positive rate growth in 2001 due to an

increasing presence of luxury hotels, annual occupancy reached a 10 year

low as a result of oversupply combined with poor performance over the last

four months of the year. A weakening of the national and Latin American

economies, fear of flying and a surge in new hotel development are anticipated

to result in further declines in occupancy and average daily rate for 2002,

with a possible rebound by early 2003.

Major Demand Changes

The horrific events of 9/11 compounded by the U.S. recession and political

and economic crises in Latin America sent the Miami tourism industry into

a tailspin. Given the area�s dependence on the Latin American commercial

and banking sector coupled with an overwhelming majority of visitors arriving

by air, the speed of recovery for Miami is expected to lag the overall

state and U.S. lodging markets.

Despite recent events, the city remains focused on servicing the needs

of an increasingly sophisticated leisure and business traveler as well

as providing the proper environment for local business to thrive. A rapid

transformation is occurring and numerous projects are expected to reshape

the Miami skyline over the next several years. Several mixed-use projects,

which are expected to impact the office and residential markets, include

the Espirito Santo Plaza and the Four Seasons Hotel and Tower, which are

currently under construction, and the $1 billion Miami One mixed-use development.

Revitalization of the area north of downtown along Biscayne Boulevard is

another major focus. The city is planning a $334 million Performing Arts

Center on Biscayne Boulevard within walking distance of the Arena, which

is expected to help transform Miami into an important cultural center.

The structure is expected to occupy 570,000 square feet and house the ballet

opera house, concert hall, and studio theater. Upon its completion in 2005,

the center is expected to have an estimated economic impact of $690 million.

In the long term, the center should help reverse a decline in property

values in the currently depressed surrounding neighbor-hoods and spur significant

commercial and residential development.

Furthermore, the development and renovation of several cultural attractions

including the $10 million Patricia and Phillip Frost Museum of Art, the

$6.5 million renovation of the Actor�s Playhouse and the $5 million refurbishment

of the historic Seminole Theater are also expected to enhance the area.

Discussions to build the $385 million, retractable-roof stadium for

the Florida Marlins have progressed, although the final location and source

of funds have yet to be determined. In addition, the redevelopment of existing

attractions such as the $46 million relocation of Parrot Jungle and Gardens

to Watson Island and the $3 million renovation of Miami Metrozoo should

provide more attractive alternatives for Miami visitors. Miami will continue

to serve as a haven for international shoppers as more high-end retailers

further enhance Miami�s image. In West Miami, the $270 million, 1.4 million

square-foot Dolphin Mall opened in 2001 and includes 150 shopping, dining,

and entertainment outlets anchored by a 400,000 square-foot entertainment

center. In Coconut Grove, an additional $7 million office and retail expansion

of Cocowalk is currently underway and expected to be completed by late

2002. In Coral Gables, the Village of Merrick Park, an 850,000 square-foot

landmark mixed-use project anticipated to open in September 2002, is currently

being developed by The Rouse Company and is expected to include office

and residential components.

Current projections indicate that the Miami International Airport (MIA)

will handle more than 40 million passengers in the next several years.

In an effort to accommodate the anticipated increase in demand, MIA is

undergoing a nearly $2 billion expansion program, which includes a fourth

runway as well as north and south terminal expansions with total completion

anticipated by mid 2006. The 8,600-square foot runway is expected to increase

airfield capacity by 22% and is scheduled for completion in 2003. It is

anticipated that the plan will maintain MIA�s competitiveness with other

airports, alleviate congestion and facilitate passenger traffic through

the airport. Additional large-scale capital improvement plans for the Miami

International Airport are planned but may be deferred in response to a

decline in passenger traffic following 9/11.

In order to relieve congestion in MIA�s terminal roadways, as well as

increase curb capacity, there are plans to restrict access to the terminal

curb for all vehicles other than private automobiles and taxis. The Miami

Intermodal Center (MIC), therefore, is proposed to serve as a regional

transportation hub as well as an extension of MIA�s ground transportation

network. The MIC will accommodate courtesy vans, buses and limousines previously

destined for MIA�s terminal curb, thereby relieving approximately 30% of

MIA�s curb-front traffic. The MIC will also serve as an intermodal hub

for Amtrak, Tri-Rail, Metrorail, a proposed East-West rail line, buses,

taxis, and private automobiles. All modes will be connected to MIA via

an automated, fixed guideway transit system, the MIC/MIA Connector. The

MIC will also house selected airport landslide terminal functions, such

as ticketing and baggage service, and will accommodate the Airport/Seaport

Connector, providing premium rail service between MIA and the Port

of Miami.

Major Supply Changes

Given the amount of luxury hotel projects entering the Miami market,

many are concerned about Miami�s ability to absorb so many four-and five-star

rooms. Although developers expect that distinct sub-markets and unique

positioning will differentiate their products, it is more likely that such

increases in supply will have a dampening effect on the market. Furthermore,

luxury and first-class properties will be increasingly challenged due to

recent additions to supply, a greater inflexibility in minimizing overhead

to maintain service levels and the effect of consumers trading-down to

upscale and midscale hotels to decrease spending.

Among the most recent luxury developments in the Downtown Miami/Brickell

submarket are the $80 million, 300-room J.W. Marriott (October 2000), the

$100 million, 329-room Mandarin Oriental (December 2000) and the $34 million

renovation of the 639-room Inter-Continental Hotel. A $350 million Four

Seasons hotel is expected to open in late 2003. With 222 rooms, 176 condo

units and 84 condominium-hotel units, the property is being co-developed

by Millennium Partners and Terremark Group and is anticipated to be the

tallest building south of Atlanta and the tallest residential complex south

of New York City. In addition, the existing apartment complex of Dupont

Plaza Center, in the downtown area, is expected to be converted into a

146-unit Residence Inn by summer 2002. Plans are also underway to upgrade

the office component of Dupont Plaza as Class B and reposition and re-brand

the existing 297 hotel rooms. Lionstone Hotels and Resorts, the current

owners, plan to develop a travel and trade center in the renovated complex

that would centralize foreign consulates, chambers of commerce and trade

shows.

On nearby Watson Island, opposite Parrot Jungle�s new home, plans for

a $281 million upscale mixed-use development are underway. The project

is anticipated to include two luxury hotels, a marina, an open-air fish

market and ancillary restaurant and retail facilities.

The $176 million, 352-room Ritz-Carlton located on Key Biscayne opened

in July 2001 complementing the 188-unit condominium-hotel, while the 115-room

Ritz-Carlton in Coconut Grove is anticipated to open in April 2002 along

with the Residences at Ritz-Carlton, a 175-unit luxury condominium project.

The condominium-hotel niche has proven to be a popular concept for the

Coconut Grove area, with the luxury $70 million, 224-condominium-hotel

Sonesta Mutiny Park anticipated to open in April 2002.

As a result of the airport expansion and development of the Miami Intermodal

Center, several hotel properties were acquired and permanently closed,

resulting in a decline of approximately 830 rooms in hotel inventory. While

the airport area has experienced a surge in limited service and extended

stay hotel developments in recent years, several full-service hotel projects

are in early development stages. Starwood Hotels & Resorts has been

in discussions with developers since early 1999 to develop a hotel in the

airport area. Reportedly, Starwood and HI Development were in discussions

to convert the existing 260-room Miami International Airport Hotel to a

Sheraton property. The project is expected to include an additional tower

containing 200 rooms; formal plans, however, are still on hold. In addition,

a possible hotel site near the Marriott Complex on Le Jeune Road for a

450-room Sheraton is rumored.

Political/Economic/Legal Changes

The Elian Gonzalez saga put Miami in the world spotlight for a five-month

period in 2000 and revived local friction over the Cuba ordinance � a legislation

that bars county support for companies that have involvement with Cuba.

The resulting turmoil at city hall was one of the factors that led to the

lost opportunity to host the inaugural Latin Grammy�s music awards to the

city of Los Angeles in 2000. A strong lobbying campaign by influential

activists brought the Latin Grammy�s to Miami in 2001, only to learn three

weeks before the event that the organizers decided to take the venue back

to L.A. due to safety concerns for attendees and performers. This major

blow to Miami was estimated to have a direct impact on the economy of approximately

$35 million, while the loss of 15,000 visitors and transmission to over

800 million viewers in over 120 countries may have wider repercussions

for the local lodging industry.

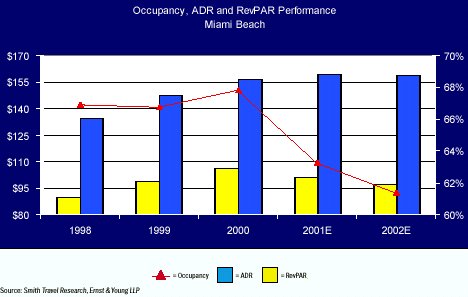

Hotels in Miami Beach are still finding themselves in an emergency mode

in the short term, leading to slashed rates of over 50% to entice Florida

residents to take a vacation close to home. Given the area�s heavy reliance

on tourism and convention activity, as well as high levels of international

visitors, the lodging market�s recovery in 2002 may move at a slightly

slower pace as compared with the overall state and U.S. lodging markets.

Major Demand Changes

With approximately 96% of the area�s visitors arriving by air, Miami

Beach�s lodging industry has continued to fare well below state and U.S.

levels in the wake of 9/11. The Greater Miami Convention and Visitors Bureau

("GMCVB") estimates a loss of approximately $750 million in tourism-related

business through November 2001 as a direct result of the terrorist attacks,

despite aggressive marketing campaigns. The GMCVB recorded seven major

meeting cancellations after 9/11, resulting in a loss of approximately

$3.9 million in revenues; these seven events have not been rebooked. The

cancellation of a leading international art show, Art Basel, which hosts

over 1,000 artists from 150 galleries worldwide, presented a major loss

for the area in December 2001. Fortunately, the show has been rescheduled

for December 2002. While the outlook for convention bookings remains cautiously

optimistic for 2002, attrition rates are expected to range from 10% to

20%. The county is also currently scrutinizing its fragmented inventory

of convention space and formulating a strategy to become more competitive,

although no specific plans have been announced.

In response to the recent terrorist attacks, the GMCVB is attempting

to entice travelers by appealing to them on an emotional level with the

roll out of the $2.2 million �What Makes You Happy� campaign, offering

special hotel rates and encouraging nearby drive-to markets to vacation

close to home. Severe drops in domestic and international air travel due

to a combination of corporate belt-tightening and fear of flying will continue

to pose threats to the tourism campaign. Overall visitation is expected

to decline between 12% and 15% in the first quarter of 2002, the peak of

Miami Beach�s tourist season.

Despite these events, the revitalization of South Beach continues to

be a major focus and numerous luxury hotel and residential projects are

underway, as well as supporting retail and office developments. While

Miami Beach has primarily been a leisure destination, it has attracted

several information technology companies in recent years. Despite several

Internet companies going bust, South Beach, which has been referred to

as Silicon Beach, remains an e-commerce hub for Internet companies serving

the Americas, including YupiMSN.com and Fiera.com. The area is also becoming

increasingly popular for entertainment companies focusing on Latin America,

as well as art-based tourism and conventions.

Major Supply Changes

Although the Miami Beach lodging market commands a $60 average daily

rate premium over Miami, the area is concerned about the depth of demand

willing to pay high prices given the wave of luxury hotel projects entering

the market. No one knows for sure how dramatic the impact will be in the

near term, particularly during the summer months when every hotelier slashes

rates to capture visitors; however, the surge of upscale commercial, retail

and recreational development bodes well for the area�s overall lodging

demand in the long term.

Among the most recent upscale developments in Miami Beach are the 324-room

Shore Club (July 2001), the 385-room Ritz-Carlton, the planned 200-room

W Hotel by Starwood and the 90-room Setai. These projects involve extensive

redevelopment efforts to blend the extravagance of luxury hotels with the

sleek art-deco style of South Beach. Another proposed entry to the South

Beach luxury set, The Victor, a historic Art-Deco style hotel, is currently

in the planning stages by ZOM properties to be developed into a luxury

hotel adjacent to Gianni Versace�s former mansion. Casa Casaurina, as the

mansion is known, will also have its share of renovations. Plans are to

make the building more public by turning it into a 15-suite, �six-star�

hotel or fractional ownership property. Following a $100 million renovation

and expansion of the DiLido Hotel, originally constructed in 1953, the

Ritz-Carlton, located on the same block of Collins Avenue as the stylish

Delano Hotel, is scheduled to open in August 2002. Within one block of

the Ritz-Carlton, a joint venture between Starwood Hotels and Resorts and

Ritz Plaza Associates will develop a 200-room W Hotel, also opening in

late 2002. Just a few blocks north of The Shore Club is The Setai, a $120

million, 90-room, all-suite resort, being developed by Adrian Zecha,

founder of Aman Resorts, expected to open in early 2003.

Other well-established hotel chains are also finding Miami Beach a desirable

market. In October 2000, Marriott opened its first resort in South Beach

along Ocean Drive. In addition, the 422-room Royal Palm Crowne Plaza, located

adjacent to the Loews Miami Beach, is anticipated to open in February 2002,

despite numerous construction delays.

The Westin Diplomat Resort & Spa in nearby Hollywood is expected

to present a

possible threat to several group hotels on Miami Beach. Featuring

998 rooms and over 200,000 square feet of meeting space, the property opened

in January 2002. In order to maintain their competitive posture in the

midst of significant new supply, existing properties in Miami Beach have

completed major renovations. The historic landmark Eden Roc Resort &

Spa underwent a $26 million upgrade and repositioning as a Renaissance

property. Sheraton Bal Harbour Beach Resort also completed an $11 million

renovation while the Turnberry Isle Resort & Club recently added a

25,000-square foot spa with a $10 million price tag. Furthermore, Roney

Palace Resort and Spa completed a $25 million renovation and redevelopment

of its 5.5 acre site.

In addition to these large-scale and chain-affiliated projects, independent

boutique hotels are flourishing in South Beach and are contributing to

the supply increase in the area. Given the high barriers to entry in this

market, these properties are typically adaptive reuses.

Recent reopenings of boutique hotels within the past few years include

the Townhouse, Whitelaw, Mercury, Abbey, Wave, and Crescent. The

242-room, boutique style Miami Beach Ocean Resort also underwent a $5 million

renovation and converted to The Palms in late 2001. In addition, The Arden

Group recently purchased the Savoy Hotel for $18 million; the property

is expected to be redeveloped and operated by S&S Hotel Management.

The Fontainebleau Hilton and Turnberry Associates recently announced plans

to build The Tower Residences at the Fontainebleau, a condo-minium-hotel

on the south end of the 18-acre property. The new $200 million, 36-story

project will feature 464 residences and is scheduled to open in December

2004. In South Beach, the 109-unit Bentley Beach condominium-hotel is anticipated

to open in June 2002. Another South Beach development, the De Soleil South

Beach, an 80-unit project located on Ocean Drive between 14th and 15th

Street, is expected to open in the spring of 2003. Condominium-hotel projects

are also being developed in Sunny Isles, including the 166-unit Ocean Point

(January 2001) and the 381-unit Trump International Beach Resort, managed

by Sonesta International Hotels, anticipated to open in September 2003.

In addition, Acqualina Ocean Resort & Residences, a 50-unit luxury

condominium-hotel and 65-room hotel to be managed by Rosewood, is anticipated

to open in late 2003.

Political/Economic/Legal Changes

Despite the revitalization efforts in Miami Beach, the city is struggling

to keep up with the growth in the immediate area. Traffic congestion and

lack of parking continue to be problems for both locals and incoming tourists.

As visitation and new developments along the skyline are expected to increase

in the coming years, these issues are expected to aggravate and negatively

impact the quality of life of residents. In addition, the city�s inability

to control and comfortably accommodate visitor attendance during large

celebrations deserve particular attention by city officials. Furthermore,

the results of recent mayoral elections in Miami Beach may limit prospects

for new development.

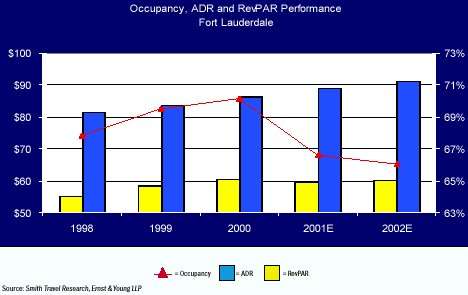

The events of 9/11 contributed to declines of approximately 16% in occupied

room nights and 4% in average daily rate for Fort Lauderdale during the

last quarter of 2001 when compared to the same period in 2000, as leisure

and group demand diminished. Despite this tough period, the city

remains committed to undergo a dramatic facelift to enhance its image as

a vibrant commercial city and upscale South Florida vacation destination.

Upcoming commercial, infrastructure and recreational developments in Fort

Lauderdale are expected to contribute to healthy lodging demand in the

future, although an estimated 6% increase in new supply in 2002 is anticipated

to negatively impact occupancies.

Major Demand Changes

Following the sudden drop of tourism traffic in the wake of the 9/11

attacks, hospitality and political leaders responded by launching multi-million

dollar marketing programs. The Greater Ft. Lauderdale Convention &

Visitors Bureau initiated a multi-faceted marketing initiative directed

primarily at Florida encouraging people within driving distance to vacation

in South Florida.

Despite monthly declines in passenger traffic of 26%, 17% and 15% between

September and November 2001 respectively, year to date figures through

November at Fort Lauderdale/Hollywood International Airport indicated a

5% increase in demand relative to the same period in 2000. An increase

in airlift capacity by Continental, JetBlue, Northwest and Spirit contributed

to the rise in demand, bringing the total number of passengers through

November to nearly 15.1 million. Domestic traffic exhibited positive growth

of 6%, while international passenger traffic declined approximately 3%

over the prior year. The city�s airport continues to succeed as a convenient

and often less expensive alternative to the more congested Miami International

Airport. The heavy presence of low-cost carriers, which capture more than

25% of the market, also makes this area popular among domestic tourists.

Fort Lauderdale/Hollywood International Airport is in the midst of a $655

million expansion program, which includes additional gates within the terminal

complex, an extension of the runway, two additional parking garages, as

well as access improvements. An additional nine-gate concourse in the new

terminal is expected to be completed by late 2002.

An expansion of 50,000 square feet of exhibit space at the Broward County

Convention Center (BCCC) is currently underway, bringing total exhibit

space to 230,000 square feet. With an expected delivery date of February

2002, the increase in meeting capacity is expected to enable the city to

compete more effectively among other destinations for trade show and association

group demand.

Major Supply Changes

Similar to its neighbor to the south, Fort Lauderdale is anticipated

to experience a surge in new luxury hotel supply over the next few years.

Ground was broken for Florida�s first St. Regis Hotel & Residences

in January 2002 along Ft. Lauderdale Beach Boulevard. This $135 million,

197-unit beachfront project is scheduled for com-pletion in late 2003 and

will also include penthouse residences and vacation ownership units. Directly

to the north of The St. Regis, at Terramar Street, a 124-unit luxury condominium-hotel,

The Atlantic, is currently planned and is expected to begin construction

in June 2002 and be completed in late 2003. Plans for a proposed Club Regent,

a 34-unit luxury fractional ownership property located to the south of

The St. Regis, on Seabreeze Boulevard, were canceled. The developer

is planning to develop an 81-unit luxury condominium-hotel and is expected

to begin construction in April 2002, with completion set for late 2003.

On North Atlantic Boulevard, the $100 million Costa Dorada, a 278-unit

condominium hotel, is slated to begin construction in September 2002 and

is expected to open in early 2004. Plans have also been unveiled for The

Capri, a $150 million resort, which is scheduled to commence construction

in late 2002 with completion in early 2004. The 346-room resort, which

is also expected to include an additional 171 timeshare units, is reportedly

in management negotiations with Regent Hotels.

In conjunction with the BCCC expansion, Peebles Atlantic Development

Corporation formed a partnership with Wyndham International to develop

the $70 million, 506-unit Wyndham Fort Lauderdale Hotel. Disagreements

between the development company and Broward County officials over the terms

of the ground lease, however, terminated negotiations between the two parties

and forced Wyndham to withdraw its support for the project. Located within

two blocks of the BCCC is the $37 million, 233-room Renaissance Fort Lauderdale,

which opened in June 2001. In downtown Fort Lauderdale, a new $15 million,

156-room Hampton Inn opened in January 2002. The area will also welcome

the expansion of the landmark Riverside Hotel with an additional 116 rooms,

increasing the hotel�s inventory to 217 rooms by March 2002.

Two major resort projects are currently underway in nearby Hollywood.

After experiencing construction delays and management turnover, the 998-room

Westin Diplomat Resort & Spa opened in January 2002. With more than

200,000 square feet of meeting space, golf facilities, retail outlets and

spa, the Diplomat is expected to compete with South Florida�s premier destination

resorts. Its sister property, the Diplomat Country Club & Spa, opened

in March 2000 just across the street from the Westin and became a member

of Starwood�s Luxury Collection. The second Hollywood project is the Seminole

Hard Rock Hotel & Resort, which is located on tribal land and currently

under construction. The $300 million complex is expected to include a 750-room

hotel, a health spa, extensive lakeside beach club, gaming facilities,

retail/entertainment complex and a Hard Rock Café restaurant.

Completion is scheduled for late 2003.

A surge in full-service hotel development within Fort Lauderdale�s suburbs

is also occurring. The newest addition to the market is a 250-room Crowne

Plaza Hotel in Sunrise, which opened in December 2001 while the 250-room

Renaissance Hotel Plantation is expected to open in September 2002. Marriott�s

second hotel in Plantation, the 250-room Marriott at Sawgrass, located

near the National Car Rental Center and Sawgrass Mills, began construction

in June 2001 and is scheduled for completion in early 2003.

In order to maintain their competitive posture during significant supply

additions, existing properties are undergoing major renovations. The Holiday

Inn Plantation/Sawgrass completed a $5 million renovation in April 2001.

The Marriott Fort Lauderdale North recently upgraded amenities, improved

guest services, and refurbished guestrooms and meeting space at a cost

of $8.5 million. In Fort Lauderdale Beach, the Radisson Bahia Mar Beach

Resort underwent a major renovation of its rooms in February 2001 while

the Marriott Harbor Beach Resort recently completed the second phase of

a $36 million refurbishment project. The resort�s new $8 million, 22,000-square

foot spa opened in June 2001. The Pelican Beach Resort, located in North

Fort Lauderdale Beach, is expected to demolish eight of its nine aging

buildings to make way for a new 168-room oceanfront hotel. Construction

is scheduled for August 2002 and inauguration planned for late 2003. Other

hotels, such as the Sunrise Hilton, which built a professional soccer field

20 yards from its main entrance, expect to maintain their competitiveness

by capitalizing on niche markets.

Political/Economic/Legal Changes

Growth in western Broward has boomed throughout the 1990s, as businesses

and residents have flocked to the new suburbs, setting off a construction

boom that has helped drive the metro area�s gains. The Eastward Ho! Regional

Planning Movement is attempting to reduce sprawl, preserve rapidly vanishing

green space and protect the Everglades by encouraging high-density development

in urban areas. Fort Lauderdale�s downtown area continues to undergo a

major transformation to an urban center for residents to live, work, and

play. The success of Las Olas Boulevard started the current development

scramble and has encouraged developers of other projects to move forward.

With a surge of high-rise, upscale residential projects under construction,

the lack of mass transit options for the area � the cornerstone for urban

revitalization � remains a concern.

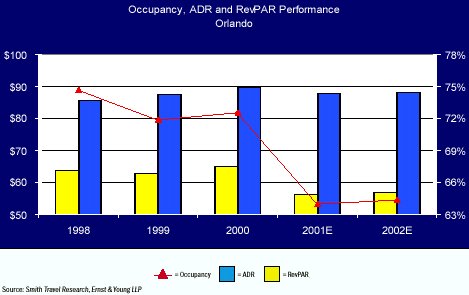

Orlando�s position as a successful leisure and convention destination,

with one of the largest hotel inventories in the nation, was significantly

challenged by the 9/11 events, lower consumer spending and cuts in corporate

travel during the latter portion of 2001. Occupancy in Orlando plummeted

by 24% in October and November 2001, compared to the same period in 2000,

while Disney park attendance reportedly dropped by 25%. Given recent signs

of positive improvement in the U.S. economy, however, hoteliers are predicting

slow but continued recovery of Orlando�s lodging industry in 2002.

Major Demand Changes

Airport passenger traffic was down a slim 5% for the year through August

2001, but in September and October these figures dropped significantly

to 32% and 23%, respectively. In response to lower levels of visitation

and occupancy declines of 24% during the latter part of the year, theme

parks and lodging facilities began regional marketing campaigns to attract

visitors within driving distance of Orlando in hopes

of combating the decline in air travel. These campaigns helped boost

visitation levels during the month of December. Since then, passenger traffic

and hotel occupancy declines have become less severe �occupancies declined

by 18% and 9% during the last two weeks of December compared to the same

time in 2000.

After breaking ground in March 2000, the $748 million expansion of the

Orange County Convention Center (the OCCC) is anticipated to add approximately

one million square feet of exhibit space, increasing the facility�s size

to 2.1 million square feet by October 2003. The expansion site is located

across International Drive and both buildings will be connected through

an enclosed, air-conditioned walkway with a people-mover. Despite declines

in convention attendance of approximately 3% pre 9/11 and 16% post 9/11,

the OCCC�s expansion plans continue as scheduled. It is anticipated that

in 2005, the first full calendar year following the completion of the OCCC�s

expansion, attendance will increase by 56% over 2002 levels, according

to the OCCC. The OCCC estimates that convention attendance will be down

by 15% during the first quarter of 2002, improving gradually throughout

the remainder of the year.

Disney World�s year long celebration of the 100th anniversary of Walt

Disney�s birth started in October of 2001 and will include special events,

new attractions and live entertainment. These special events and attractions

are anticipated to generate increased media awareness for the parks to

boost demand. In fact, two of its parks, Magic Kingdom and EPCOT Center,

reached maximum capacity during the December 2001 holiday season.

Disney World will be adding a new attraction in 2003. The Space Pavilion

at EPCOT Center will feature a series of interactive exhibits and space

exploration-themed shows. The motion-simulator ride will be based on the

equipment that NASA astronauts use to prepare for space flights. Details

of the project are still being finalized but Disney is moving forward with

the $200 million project and has already begun preliminary work inside

the Horizons Pavilion at Epcot.

Plans are still underway to build a World Expo Center in Osceola County,

with an estimated opening date of 2005. After the original developer was

unable to move forward with the project, the county re-bid the project

and the developers of the Gaylord Palms Hotel, Xentury City, plan to place

a bid. Once built, the World Expo Center is anticipated to generate additional

convention and group demand for the Orlando area.

Major Supply Changes

Prior to 9/11, the Orlando lodging sector responded to increasing room

demand by aggressively adding hotel rooms, and observed inventory increases

of approximately 26% between 1995 and 2000.

Approximately 3,400 additional rooms were added in 2001 for a total

of 105,800 rooms, a 3% increase over 2000. Between 2002 and 2005, approximately

10,800 rooms are anticipated to enter the market, bringing Orlando�s supply

to 116,600 rooms, a 10% increase. Limited-service hotels comprise 14% of

this pipeline, which does not include hotel projects placed on hold or

rumored.

In Kissimmee, the Gaylord Palms Hotel, formerly known as the Opryland

Florida, located two miles from the proposed World Expo Center, opened

its doors ahead of schedule in January 2002. The $450 million hotel features

1,406 rooms on 68 acres and approximately 400,000 square feet of meeting

space, including a 178,000-square foot exhibition hall. Developers expect

occupancy in the first year to reach approximately 60%, largely comprised

of convention and group business. A third Loews property at Universal Studios,

the 1,000-room Royal Pacific Resort, is anticipated to open in July 2002.

Orlando�s Grand Lakes Resort, along John Young Parkway, is under construction

and will feature a 584-room Ritz-Carlton Hotel and a 1,000-room JW Marriott

Hotel, both of which are expected to open in July 2003. Four Seasons is

reportedly also looking to make an entry in the local market.

The $700 million, 1,200-acre Champions Gate master-planned resort development

adjacent to Celebration, including a 730-room Omni Hotel, was delayed due

to slower economic trends. The Omni Hotel will reportedly feature 80,000

square feet of meeting space and is now expected to open in early 2004.

Another major planned community, the Reunion Resort and Club, has plans

for up to 3,000 hotel rooms on its 2,300-acre site, in addition to 5,000

resort homes, three golf courses, an equestrian center and other recreational

facilities to be delivered in 2003.

Hyatt Hotels acquired land in the vicinity of the OCCC for a 1,500-room

hotel with a tentative opening date in 2005. Also adjacent to the Center,

Hilton Hotels Corporation has plans to build a 1,200-room hotel on land

it purchased from Universal Orlando. The proposed Hilton expects to offer

100,000 square feet of meeting space. Construction was expected to commence

in early 2002, however, the project was placed on hold as a result of unfavorable

market conditions.

Hotelier Harris Rosen acquired from Universal Studios a $30 million,

230-acre site near the Bee Line Expressway, to build a 1,500-room convention

hotel, with a golf course and 250,000 square feet of meeting space. Construction

is expected to start in early 2003, with the hotel opening in 2005. Development

of Disney�s 5,760-room economy-style Pop Century Hotel was indefinitely

postponed following the events of 9/11.

The 2,267-room Swan and Dolphin hotels are undergoing a $75 million

expansion and enhancement project to be completed in the fall of 2002,

which includes the addition of 79,000 square feet of meeting space to the

Swan property. The two hotels� exhibition space will also be expanded from

61,000 to 111,000 square feet, and the properties are upgrading their facilities

to become more competitive with

new group and convention-oriented hotel supply anticipated to come

on line in the next three years.

Political/Economic/Legal Changes

Despite recent declines in lodging industry performance, the majority

of Orlando�s service industry jobs have been saved and local county governments

as well as tourism-related entities have approved millions of dollars for

emergency marketing spending. Recent economic changes, however, indicate

that Orange and Osceola counties are especially vulnerable to declines

in this tourism-based economy. Walt Disney World cut 4,000 jobs and reduced

work schedules for 40,000 employees.

There are discussions taking place regarding possible increases in

the tourist bed tax and a change in Florida State law to use a portion

of the tax proceeds to spur economic development and to further diversify

the local economy.

A mid-term solution to traffic congestion is becoming increasingly important.

New transportation improvement projects, totaling over $3 billion, are

currently being discussed and involve the widening of Interstate 4 through

Orange, Seminole, and Osceola counties, the addition of high-occupancy

vehicle and possibly toll lanes, as well as a new rail system. Passenger

traffic at the Orlando International Airport

surpassed the 30 million mark in 2000 and the airport is now completing

a $1.2 billion expansion program. Despite the recent impact of 9/11 events

on the aviation industry, airlift capacity improvements are crucial to

sustain long-term tourism and business growth.

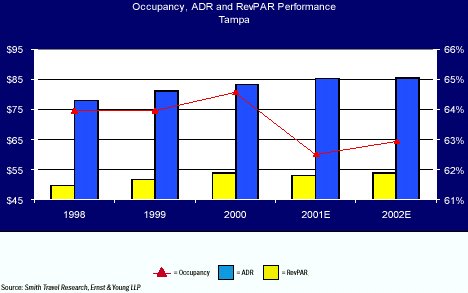

While hotel demand growth outpaced supply growth in 2000, the events

of 9/11 resulted in declines in hotel demand during the latter portion

of 2001, while supply remained relatively stable. Compared to lodging activity

in other Florida markets, however, Tampa was not as adversely impacted

during the 2001 calendar year. More than 5,000 new hotel rooms are in the

pipeline for the next three years; the majority of projects are rumored

or in the early planning stages. Hotel occupancies are anticipated to improve

in the third quarter of 2002 and newly built shopping malls and entertainment

complexes are expected to contribute to an increase in areawide lodging

demand.

Major Demand Changes

Tampa has observed a recent boom in shopping mall, retail and entertainment

complex construction. Local hoteliers expect new shopping and entertainment

centers to increase local hotel demand from tourists extending their stay

in Central Florida to shop after trips to Disney World and the west coast

beaches. In Ybor City, Steiner & Associates opened Centro Ybor, a $45

million, 210,000-square foot

retail and entertainment complex with upscale shops, restaurants, a

20- screen Muvico Movie Theater, Game Works and a comedy club. The company

expects the new mall to receive three million visitors per year, including

non-regional tourists in the area visiting other attractions.

The Tampa Convention Center re-adapted its 600,000 square foot facility

to accommodate 36 breakout rooms, from the existing 18, through the reconfiguration

of storage and office space. Following the $6 million renovation project,

completed in October 2001, the Center now offers 200,000 square feet of

exhibit space and 85,000 square feet of meeting space. The increase in

the number of breakout rooms is

expected to improve the Convention Center�s ability to accommodate

smaller groups, therefore generating more convention activity to the area.

In 2000, Tampa hosted 108,000 convention delegates, while in 2001, convention

attendance increased by 80% to 194,000, as a result of the Super Bowl.

Annual passenger traffic at the Port of Tampa reached 519,000 in 2001,

up 13% from 2000, as a result, in part, of two new cruise ships, the Royal

Caribbean Rhapsody and the Celebrity Venus, which began sailing in the

latter part of the year. Passenger volume in 2002 is expected to further

increase to approximately 600,000, according to the Port Authority. As

most cruise line visitors require overnight accommodation prior to departure,

hotel demand is expected to be positively affected.

Major Supply Changes

A number of full-service hotels are currently underway in the Greater

Tampa area. Westin Hotels & Resorts unveiled plans for a 300-room luxury

hotel scheduled to open in mid-2004 at Tampa Bay I, a $200 million office

and retail center planned for Interstate 275 and Dale Mabry Highway. Despite

the events of 9/11, the upscale 1.2 million-square foot International Plaza

shopping mall in the Westshore business district opened in mid-September

2001. The $200 million project was developed by a Michigan-based REIT and

is anticipated to further include a four-star hotel with approximately

300 rooms and a target opening date in 2003. Negotiations are still underway

to select a hotel operator. In the meantime, the mall has been attracting

out of town visitors and offering hotel packages on its Internet site.

The Tampa Port Authority has a master-plan development to enhance dockside

attractions for visitors and the local community. The Shops at Channelside,

comprising the first phase of the plan, are a joint development of the

Hogan Group and Orix Corporation and opened in the spring of 2001. The

urban entertainment center is a 230,000 square foot, $35 million complex,

adjacent to the Florida Aquarium and cruise terminal. The open mall includes

a nine-theater movie

complex, a number of specialty restaurants, and retail. The master

plan further includes the addition of three more cruise terminals (including

Cruise Terminal 3 which is already under construction), an expansion of

the Tampa Florida Aquarium and a hotel with up to 1,000 rooms and meeting

space. According to the Port Authority, there are no significant negotiations

taking place between the Port and a possible developer for the hotel site

at this time. The entire plan for the area will take five to 10 years to

implement.

The Tampa Bay area�s newest hotel is the $130 million, 266-room luxury

waterfront Ritz-Carlton in Sarasota, which opened in November 2001. The

hotel features 18,000 square feet of meeting space and $48 million condominium

units. The hotel development triggered $1 billion in real estate and infrastructure

construction and redevelopment in downtown Sarasota and along the waterfront.

The hotel plans to further add a 15,000-square foot spa and private beach

club in the fall of 2002.

A second luxury hotel is proposed as part of an $80 million redevelopment

project including a 17-story luxury condominium tower, upscale retail and

an 86-room luxury hotel at the intersection of Drew Street and Osceola

Avenue, in Clearwater. Construction may start in 2003, depending on economic

conditions at the time.

Additional new supply in the Greater Tampa area includes a 160-suite

Residence Inn by the McKibbon Brothers, which opened in the Westshore business

district across from the International Plaza mall in November 2001. Furthermore,

a 205-room Radisson Hotel and Conference Center in St. Petersburg and a

115-room Hilton Garden Inn in the Sarasota-Brandenton International Airport

also opened in December 2001.

In addition to the proposed full-service hotel supply, several Microtel

Inn & Suites, Holiday Inn Express & Suites, Bradbury Suites, Marriott

limited-service products, Wingate Inn and Hilton Garden Inn properties

are proposed in the Greater Tampa area to be developed in the next three

years. In the all-suite segment, Matrix Lodging plans to launch a new hotel

concept, eSuites, in 2002. One of nine initial 150-unit technology-oriented

eSuite hotels is expected to be built in Tampa.

Political/Economic/Legal Changes

Tampa is one of the top cyber cities in the country and ranks fifth

among the top cities in the nation for high-tech jobs. It is estimated

that approximately 1,600 high-tech businesses have settled in the Tampa

Bay area. Although at a slower pace than in past years, high-tech companies

continued to relocate to Tampa and expand existing facilities in 2001.

Tampa�s recognition as the heart of the state�s high-tech

corridor significantly contributes to the immediate area�s overall

economic development.

Tampa International Airport is a fast growing airport handling more

than 16 million passengers per year. Prior to 9/11, airport passenger activity

was up by 5% in 2001 compared to the prior year. Following the terrorist

events, however, the number of enplaned and deplaned passengers experienced

declines ranging anywhere from 13% to 27% for the period between September

and December 2001. Despite the

recent decline in passenger activity, Tampa International Airport is

undergoing a five-year, $400 million expansion project to accommodate an

increasing number of passengers in the mid- to long-term, which includes

the renovation and expansion of two airside terminals, the addition of

aircraft parking, the refurbishment of ticketing areas, the construction

of a 2,100-car passenger parking lot, the upgrade of the monorail system

and a $7 million renovation of the Airport Marriott Hotel. Local airport

authorities expect the expanded airport to be capable of supporting growing

passenger traffic resulting from increased business and tourism travel

to the area. It is anticipated that construction and renovations will be

completed by 2005.

Daytona Beach

Traditionally known as the premier racing destination along Florida�s

east coast, Daytona is undergoing the biggest tourism expansion in its

history and was fortunate enough to be one of the few markets throughout

the state to be only marginally impacted by the events of 9/11. According

to Mid-Florida Marketing and Research, Inc., occupancy in September following

the attacks dropped approximately five points to 48% compared to the same

period during the prior year. While occupancy remained fairly stable

for the remainder of 2001, average room rates surprisingly increased by

as much as 9%. ADRs in November, for example, increased from $64 in 2000

to approximately $70 in 2001.

This stellar performance -relative to other destinations in Florida

and considering the impact of 9/11 throughout the state- was largely attributed

to the drive-in nature of this market. It is estimated that approximately

85% of visitors drive to Daytona, a figure that is expected to remain stable

in the near term due to limited airlift to the city � the only airline

carrier to now service Daytona is Delta Airlines, after Continental Airlines

decided to cancel its flights in mid-2001. Another factor that helped Daytona

post better-than-anticipated performance in 2001 was that hotel owners

avoided heavy rate discounting by attracting higher paying visitors who

would normally fly to other destinations but opted to drive to Daytona

as a result of

9/11 events. For 2002, general managers and other lodging professionals

expect occupancy in Daytona to recover within the first six months and

room rates to show positive growth throughout the year.

Daytona observed in 2001 the construction of the $250 million Ocean

Walk Village redevelopment project, which includes upscale hotels, boutiques,

restaurants, and shopping. The project is expected to reshape the city

as an attractive convention destination and a more upscale leisure alternative.

The 300-room Ocean Walk Resort at the Village, which opened in mid-2001,

is Daytona�s newest oceanfront condominium-hotel. Significant renovations

underway include the $37 million refurbishment of the Plaza Resort and

Spa, which will include the renovation of its 322 rooms and public areas

and an increase of 32,000 square feet in meeting space, anticipated to

be completed in early 2002. Another important project, the $53 million,

310-room expansion of the Adam�s Mark Hotel, planned for early 2002,

is expected to add 35,000 feet of new meeting space and increase the hotel�s

inventory from 436 to 746 guestrooms. Plans are also underway to break

ground on a second phase of the Ocean Walk Resort in 2002, which will feature

264 additional units in a $40 million tower.

Greater Naples and Marco Island

With the most golf holes per capita and ranking among the Top 25 art

markets in the nation, Collier County is recognized as one of the premier

resort destinations on the Gulf Coast of Florida, boasting renowned hotels

such as the 463-room, five-star, five-diamond Ritz-Carlton Naples and the

474-room Registry Resort. Given that the area is a high-end golf and leisure

destination comprised mostly of affluent, fly-in visitors with substantial

discretionary income, this market was significantly impacted by the events

of 9/11, as its customer base dramatically cancelled its travel plans after

the attacks. According to Research Data Services, occupancy in Collier

County for September 2001 declined significantly to 39% from 59% the previous

year while direct visitor expenditures were just over $8 million, a 36%

drop compared to 2000 levels. Hotel owners are concerned that warmer weather

in the Northeast, a shorter winter season due to Easter Holidays occurring

earlier this year in late March and a slower booking pace from Canadian

and European visitors may further delay the area�s recovery in 2002.

In terms of development, Naples is yet another city in the state to

be placed under a moratorium on new construction as a result of fears of

unmanaged growth. Officials are concerned that the area may grow in a disorganized

fashion and have issued restrictions on land use in Naples, including hotel

projects, to allow time for officials to dialogue with landowners, developers,

and environmental groups and identify

better ways to control urban sprawl and preserve agriculture and the

environment. This measure, however, only impacts future projects and is

not expected to affect several hotels that are already under construction.

In 2001, Naples welcomed the

456-room Hyatt Regency Coconut Point, which opened in October and a

51,000 square foot spa at the Ritz-Carlton Naples. Several renovations

were also completed such as the refurbishment of 63 suites at the Edgewater

Beach Hotel and the redecoration of 256 rooms at the Naples Beach Hotel

and Golf Club. Neighboring Marco Island also welcomed the luxurious Marco

Beach Ocean Resort in December, which features 103 one- and two-bedroom

suites, a full-service spa and approximately 12,000 square feet of meeting

space.

Major developments for 2002 include the opening of the $75 million Ritz-Carlton

Golf Resort, which features 295 rooms overlooking a 36-hole, Greg Norman

golf course and a signature 18-hole putting green, the $45 million renovation

of the 189-room La Playa Beach and Golf Resort and the introduction of

a 124-room Four Points Sheraton in downtown Naples. The Marco Island Marriott

Resort and Golf Club is expected to launch a major $43 million refurbishment

project to be completed by mid-2003, which will include renovating all

of its guestrooms, adding a full service spa, 10,000 square feet of meeting

space and renovating its 18-hole golf course. In Naples, the Inn on Fifth

will also undergo a $700,000 renovation project to upgrade its guestrooms

and public areas.

Although September is typically considered a slow period for hotel owners

in the Florida Keys (The Keys), the events of 9/11 impacted visitation

to the region causing occupancy to decrease by as much as 10% for the same

period during the prior year. Lodging performance was further affected

in November 2001 due to concerns that Hurricane Michelle could hit The

Keys, forcing city officials to order a mandatory

evacuation and to postpone the final race of the Powerboat World Championship.

Although the lodging sector showed some signs of recovery during the last

two weeks of the year � posting occupancies in the high eighties � this

demand came at a high price to hoteliers, as they were required to deeply

discount room rates to lure drive-in visitors.

Given the drive-in nature of The Keys� market, lodging professionals

are banking on increased levels of in-state visitors to help support occupancy

levels in 2002, although this demand is anticipated to come in at reduced

rates. Recent meetings between OPEC members, however, are signaling a possible

nationwide increase in gasoline prices, which may have a negative impact

in the area as Floridians may decrease vacation travel within the state.

In general, 2002 is expected to be a challenging year for The Keys. Hotel

owners hope that increasing consumer confidence as a result of improvements

in the economy and last-minute bookings will improve the sector�s performance

by third-quarter 2002.

Fortunately for The Keys, the area has only experienced a limited amount

of new development in recent years � preventing occupancies from further

decreasing � as a result of a construction moratorium imposed by authorities

due to their concerns about the appropriateness of evacuation routes should

a natural disaster strike.

The last major new hotel development in the area was the construction

of the 216-room full-service Grand Key Resort in August 2000. That same

year in March, the 74-room Hampton Inn in Marathon Key opened its doors

and in July, the Econolodge in Key West was repositioned as a Radisson

Hotel. Other recent additions to the area include the development of 247

villa units at Hawks Cay Resort,

which has been phased over the past three years. The resort also added

15,000 square feet of meeting space in 2001 and now features one of the

largest ballrooms in the region. Cheeca Lodge, a 203-room property built

in 1946 and affiliated with Small Luxury Hotels of the World, also recently

completed a 5,200 square-foot spa.

Given the moratorium on new construction, The Keys experienced a wave

of repositionings and limited new development in 2001. The Holiday Inn

La Concha, for example, was repositioned as a Crowne Plaza in January.

The Howard Johnson, which remained closed for over two years, became the

64-room Courtyard Key West Waterfront in May after extensive renovations,

while the Ramada Hotel was also repositioned as the 104-room Courtyard

Key West By-the-Sea. The pipeline for 2002

looks narrow, as the only major development in the region is a rumored

timeshare development by Spottswood Companies. The lack of significant

new supply is anticipated to accelerate the speed of recovery for The Keys.

Jacksonville�s $2.8 billion tourism economy was particularly affected

by the events of 9/11. For the past few years, the city has worked hard

to change its image and become a more attractive convention destination.

This stronger reliance on the group and meetings segment and the heavy

cancellations that occurred post 9/11, however, resulted in losses of as

much as $28 million according to the Convention and Visitors Bureau. Suffering

from a retraction in corporate travel expenditures, the

events of 9/11 further exacerbated declining occupancies due to the

city�s dependence on the group and meeting segment. In 2002, hotel owners

expect the booking pace to pick up and meeting planners to rebook meetings

and conventions. Overall, the city is expected to observe some signs of

recovery by mid-2002.

For the past three decades, Jacksonville has not experienced major hotel

developments in or around downtown. This trend, however, is being reversed

as the city welcomed a 966-room Adam�s Mark Hotel in February 2001. The

$126 million project is one of the largest meeting hotels in Northeast

Florida and should become the center-piece for the city�s plans to attract

larger conventions and become known as a meetings destination. The new

development is also expected to serve as the catalyst for several new construction

projects and corporate relocations to the downtown area. According

to the Convention and Visitors Bureau, in addition to the Adam�s Mark project,

the city observed the development of approximately 605 hotel rooms in 2001,

driven primarily by limited service and midscale properties. This new inventory,

however, is not expected to help the city in its efforts to generate additional

convention business, as these facilities feature limited meeting space.

As such, officials are being forced to reconsider the future of the Prime

Osborn Convention Center and its implications on the local economy. Two

alternatives being analyzed are the development of a new 150,000 square

feet facility with an attached hotel or the expansion of the existing infrastructure.

--

The Ernst & Young 2002 Florida Lodging Forecast contains an analysis

of data compiled from many sources, with credits identified. The contents

of this report is for reference only, not to be used as business advertisement

or to set standards on

policies or actions.

For additional information on the topics contained in the 2002 Florida

Lodging Forecast, or for information about services provided by the Ernst

& Young Real Estate Advisory Services Group, please contact any of

the following individuals:

© 2002 Ernst & Young

All Rights Reserved.

Ernst & Young is a registered trademark. |