| Effect of 9/11 on Hotel Industry

The World Trade Center tragedy resulted in the destruction or damage

of four downtown hotels�the Marriott World Trade Center, Marriott World

Financial Center, Millennium Hilton, and Embassy Suites Hotel New York

City. These hotel closings resulted in an instantaneous 3.8% decrease in

Manhattan�s overall room supply. The Marriott World Trade Center was completely

destroyed and plans to rebuild the property have not been announced. Although

reported to be structurally sound, the Millennium Hilton remains closed

and its reopening date is contingent upon the on going cleanup efforts

at Ground Zero. The Marriott Financial Center reopened its 504 rooms in

early January 2002. The new Ritz-Carlton Battery Park City, which postponed

its October 2001 debut, is also slated to open by the end of January 2002.

The Embassy Suites Hotel New York City is scheduled to resume operations

in 2002.

In Midtown, however, hotel opening dates have remained relatively unaffected

by the events of September 11. The W Times Square had already experienced

construction delays throughout the year, but opened on December 27th, 2001,

just in time to ring in the New Year. Serving as the flagship property

for the W chain, the opening of the 509-room property also marks the first

major hotel opening since September 11. Other notable upcoming hotels openings

in Midtown Manhattan in 2002 include the Westin New York at Times Square

and the Ritz-Carlton Central Park South.

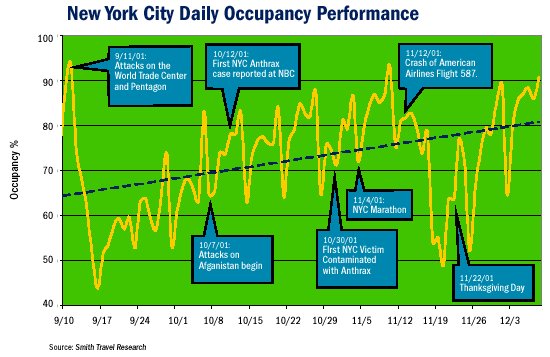

The attacks on the World Trade Center in Lower Manhattan marked a turning

point for the nation�s highest performing lodging market. Due to declining

economic conditions and the attacks of September 11, RevPAR for Manhattan

decreased at a record breaking pace in fourth quarter 2001, primarily due

to relatively low occupancy levels. Occupancy for Manhattan fell to 62.2%

and 70.8% for September and October 2001, respectively, in comparison to

levels of 89% and 87% during the corresponding months in 2000.

According to a study commissioned by NYC & Company, New York City�s

convention and visitors bureau, RevPAR losses after September 11 were estimated

to total approximately $400 million in hotel revenue for fourth quarter

2001 alone. Historically, room revenue earned in the last third of the

year represents approximately 40% of Manhattan hotels� annual room revenue,

further reinforcing the significance of the last four months of 2001. The

study estimated that the City�s travel and tourism-related sectors will

lose between $7 and $13 billion in total revenue, or between 6.8% and 11.7%

of the $102 billion in tourism spending that was originally projected for

2001 through 2003.

After September 11, the Manhattan market continued to experience sharp

fluctuations in occupancy, ADR, and RevPAR in response to current events.

Despite the decreased tourism and heavy discounting after September 11,

lodging performance indicators did trend upwards during the fourth quarter,

allowing Manhattan to retain its position as the nation�s top performing

lodging market in terms of ADR and RevPAR.

Impact on Demand Generators

Office Space

Approximately 20% of the Downtown Manhattan office market�15.5 million

square feet of space�was directly destroyed as a result of the September

11 attack. Another 12 million square feet of office space was damaged in

the aftermath of the attack due to falling debris, building collapses and

fires. Of the space that was destroyed or damaged, more than 96%, or approximately

26.5 million square feet, had been leased at the time of the attack.

An estimated 81,000 workers had been displaced as a result of the loss

or damage of the nearly 30 million square feet of office space in Lower

Manhattan. The largest companies displaced from Lower Manhattan included

Merrill Lynch (3.1 million SF), Lehman Brothers (1.4 million SF), Morgan

Stanley Dean Witter (1.4 million SF), Solomon Smith Barney (1.4 million

SF), American Express (1.2 million SF), and Bank of New York (800,000 SF).

Although Manhattan contained approximately 25.8 million square feet of

vacant office space at the time of the attack, tenants primarily requiring

large contiguous space relocated to areas outside of Manhattan. Since the

attacks, the Hoboken/Jersey City waterfront has garnered the most interest

for office space outside of Manhattan.

In response to the events of September 11, several Midtown hotels, such

as the Sheraton Manhattan Hotel and the Marriott Marquis in Times Square,

converted all or a portion of its guestrooms into offices for Lehman Brothers

and Deloitte & Touche, respectively. These two conversions alone shrunk

the Manhattan rooms supply by approximately 850 rooms, although they only

represent temporary reductions in rooms supply and the tenants at both

hotels are anticipated to move out in 2002.

By the end of 2001 an estimated 6,000 employees of Merrill Lynch had

moved back to the World Financial Center. American Express and Dow Jones

& Co. also announced that they would begin their return to the World

Financial Center by April 2002. Lehman Brothers, however, will not return

to its Downtown offices as the company will establish its new headquarters

at the recently completed Morgan Stanley tower in Times Square.

Visitation/Air Travel

New York City�s three airports�La Guardia, JFK, and Newark-were completely

shut down from inbound and outbound flights for three days following the

attacks. Since their reopening, major airlines have reduced flights by

as much as 20% nationwide, with New York City experiencing an even larger

reduction of flights. As such, the Port Authority of New York and New Jersey

estimated that passenger traffic at all three airports would decrease by

17.4 million passengers in 2001.

Redevelopment of Downtown�Agencies, Programs & Initiatives

The timing and scope of the redevelopment plans for Lower Manhattan,

particularly the World Trade Center site, were still undetermined at the

close of 2001. Yet, it was widely recognized that the success of Lower

Manhattan was dependent upon the pace of the cleanup efforts and overall

support from the private sector to re-establish Downtown as the world�s

premier financial center.

The two major groups charged with redeveloping Lower Manhattan are the

Downtown Alliance and the newly created Lower Manhattan Redevelopment Corp.

Initiatives undertaken by the Downtown Alliance since September 11 include:

a grant and loan program for retailers, subsidized advertising for local

businesses, and support of tax credit legislation for both businesses and

residents near the World Trade Center site. The Lower Manhattan Redevelopment

Corp., created under Giuliani�s administration, is headed by John Whitehead,

former Co-chairman of Goldman, Sachs & Co. The organization�s primary

purpose is to determine a response to Lower Manhattan�s economic and infrastructure

needs and, more specifically, to develop plans for the World Trade Center

site.

Aid from the Public and Private Sectors

To encourage the return of tourists and business travelers to the Big

Apple, the public and private sectors launched numerous tourism promotion

campaigns. Among NYC & Company�s Fall 2001 promotions was �Paint the

town Red, White, and Blue,� where visitors received a variety of retail

discounts with proceeds being donated to the Twin Towers Fund. NYC &

Company has also undertaken a $12 million advertising campaign, where celebrities

such as Cindy Crawford and Regis Philbin proclaim their devotion to New

York City. This ad campaign also included the heavily aired �I Love New

York� commercial featuring former Mayor Rudolph Giuliani and Governor George

Pataki.

The most publicized support form the private sector came from Delta

Airlines, which launched its �Delta Loves NYC� campaign where the airline

is giving away more than 10,000 air tickets for travel to New York City.

Other symbolic gestures from companies and organizations included relocation

of meetings and conventions from other cities to Manhattan. Organizations

showing this form of support included the American Society of Travel Agents;

American Federation of State, County, and Municipal Employees; Audio Engineering

Society; and Microsoft.

Current Development Activity

in Manhattan

New Headquarters in Midtown

In 2001, office development remained strong in Manhattan with new projects

primarily located in Midtown and, more specifically, Times Square. New

office towers that opened in 2001 included the Reuters headquarters (3

Times Square), an 855,655-square foot-office building at the northeast

corner of 42nd Street and Seventh Avenue, and Morgan Stanley�s 1.6-million-square-foot

office building (recently sold to Lehman Brothers) on Seventh Avenue between

49th and 50th Streets. Other office projects under construction include

Ernst & Young�s headquarters at 5 Times Square (opening in April 2002)

and Arthur Andersen�s headquarters on 42nd Street and Seventh Avenue (opening

in early 2004). Each office tower will feature approximately 1.2 million

square feet. Additionally, the recent announcement of the 2003 groundbreaking

date for the New York Times building (1.5 million square feet), located

opposite the Port Authority Bus Terminal, signifies the continued transformation

of Times Square over the next several years.

Mixed-use Momentum

In recent years, Times Square has been the focus of mixed-use development

with the construction of Forest City Ratner�s retail and hotel development,

comprised of the 444-room Hilton Hotel, 25-screen AMC Empire movie theater,

and Madame Tussaud�s Wax Museum. Across the street, Tishman�s E-Walk complex

will increase activity to the area with the 863-room Westin, which is anticipated

to open in November 2002.

Mixed-use projects are gaining momentum outside of Times Square as the

Related Companies continue construction at 10 Columbus Circle (59th Street

and Central Park South). This project will contain a total of 1.65 million

square feet for its office, hotel, retail and residential uses, including

the AOL Time Warner headquarters and Mandarin Oriental Hotel. The Columbus

Circle project is estimated to open in 2004.

Millennium Partners and Ritz-Carlton have also played a significant

role in defining the mixed-use concept for Manhattan with its two hotel

/ condominium projects � Ritz-Carlton Battery Park City and Ritz-Carlton

Central Park South. Both projects are anticipated to open in 2002.

Most recently, the Trump Organization entered a contract to purchase

the Hotel Delmonico on Park Avenue and 59th Street for $115 million. Trump

is considering plans to convert the property into a mixed-use development,

consisting of luxury condominiums, hotel rooms, and retail space.

Planes, Trains and No Automobiles

On October 21, the AirTrain Newark opened. This new station links the

existing airport monorail system with more than 150 Amtrak and New Jersey

Transit trains. Advertising a 20-minute ride from Manhattan�s Penn Station,

the service exceeded ridership projections during its first month of operations.

Additionally, a $1.5 billion AirTrain project is underway at JFK Airport.

The new system will link many of JFK�s terminal buildings to the Metropolitan

Transit Authority (MTA) subway lines and the Long Island Rail Road (LIRR)

at stations in Jamaica and Howard Beach. The AirTrain at JFK is expected

to alleviate traffic congestion in and around JFK Airport and be fully

completed in 2003.

Our Top 10

Thoughts for 2002 and Beyond

1. New York Rising

Our year-end 2001 RevPAR estimate of $145 for Manhattan is similar to

the market�s performance in 1997 on a RevPAR basis. Manhattan has experienced

its lowest occupancy level since the early 1990s, yet historical trends

and macroeconomic forecasts suggest occupancy will remain stable in 2002.

ADR in 2002 is anticipated to remain constant due to continued room rate

discounts anticipated for the early part of the year. However, beginning

in 2003, occupancy and ADR are anticipated to increase as New York continues

to re-establish itself as the world�s financial and tourism capital.

2. Survival of the Segments

YTD November 2001 RevPAR statistics for the luxury, upscale, and midscale

segments indicate levels similar to those achieved in 1996 and 1997. RevPAR

for the luxury segment dropped at the fastest rate while RevPAR for the

upscale and midscale segments were affected relatively equally through

YTD November 2001. With more than 200 hotels competing for room demand

on the island of Manhattan, each segment will keep a close eye on their

competition when implementing their yield strategies in 2002.

3. Show Me the Money

Despite the Federal Reserve�s recent efforts to inject liquidity into

the capital markets, the hospitality industry is unlikely to follow suit.

Accordingly, several projects in the planning stages for the near term

may not come to fruition. For existing owners, the desire to refinance

at lower interest rates may be hampered by the limited number of willing

lenders and more onerous conditions. Long-term implications are likely

to include lower LTV�s, higher coverage ratios, more expensive mezzanine

financing, and rewards for strong brand affiliation.

4. Caveat Emptor

Despite the few hotel sales transactions in Manhattan for 2001, there

was a flurry of buyers eyeing opportunities to acquire depressed hotel

assets in the wake of September 11 local economy. With the economic downturn

continuing into early 2002, the risk for loan defaults still exists and

hotel investors will be anxious to acquire hotels at the low end of Manhattan�s

lodging cycle to capitalize on the upside potential over the next several

years.

5. Bridge and Tunnel Scene

The booming �90s, coupled with the saturation of Midtown Manhattan,

resulted in hotel development across the bridges and through the tunnels,

into neighborhoods such as Brooklyn, Queens, and Jersey City.

The strength of the Manhattan lodging market caused room demand to spill

over into these non-traditional hotel markets, where availability of land,

public investment, lower development costs and the existence of some base

demand helped to facilitate development opportunities.

However, the success of these neighboring markets is very much tied

to Manhattan�s lodging market performance and hotel developers may need

to reassess their outlook on prospective projects in these outlying locations.

6. The New Face of Lower Manhattan

Plans for the World Trade Center site are under active discussion.

The pace of Lower Manhattan�s commercial redevelopment will be dictated

largely by market demand and it is anticipated that new buildings will

not be built �on spec.� Such rebuilding efforts, stemming from the public

and private sectors� overall commitment to restore activity in Downtown,

will also dictate the pace of future hotel development in Lower Manhattan.

7. bloomberg.com

Mike Bloomberg made his own headlines when he was sworn in as the new

mayor of New York City in January. It is expected that Bloomberg will fill

these big shoes with guidance from former mayor Rudolph Giuliani, who is

anticipated continue lending his valuable leadership and expertise to the

City. As the City is anticipated to receive approximately $12 billion in

federal aid for its redevelopment efforts, leadership at the local level

will be instrumental to the appropriation of these funds and the speed

of Manhattan�s recovery.

8. The Bottom Line

In the wake of a more challenging marketplace, hotel operators and owners

have attempted a number of effective cost-cutting measures to offset increases

in insurance and other operating expenses. Alternative tactics include

financial restructuring, outsourcing, shared services, facility redeployment,

tax minimization, rationalization of human resources and incentive programs,

and improved information technology efficiencies.

9. Meeting Adjourned?

In today�s challenging economic environment and cost-containment mindset

(compounded by increased security issues), aligning travel/communication

and strategic business needs has become even more critical to profitable

operations for Corporate America. Market responses may include changes

to corporate travel policies, such as using a single corporate travel planner,

long-term leasing of hotel rooms and ancillary facilities, renegotiation

of existing hotel contracts, as well as a more structured use of modern,

on-site technologies for meetings, training programs, and other corporate

activities as a means to limit unnecessary off-site travel.

10. Go West

The City has revealed extensive redevelopment plans for an underutilized

section of Manhattan. Far West Midtown, designated as the area west of

9th Avenue between 28th and 42nd Streets, has been highly recognized among

legislators for its proximity to Midtown, small population base, and abundance

of underdeveloped land. Major projects included in the City�s plan include

the expansion of the Javits Center, a western extension of the Number 7

subway line from Times Square, and the possible development of a new stadium

that would serve as the future home of the New York Jets. The spotlight

will shine brighter on Far West Midtown for commercial development and

public infrastructure improvements if New York City is selected to host

the 2012 Summer Olympics. Serving as a catalyst to stimulate development

in Far West Midtown, the Olympic Games would also provide Manhattan an

opportunity to showcase the culmination of its decade of rebuilding efforts

after September 11, 2001.

---

© 2002 Ernst & Young

All Rights Reserved.

The Ernst & Young 2002 Manhattan Lodging Forecast contains an analysis

of data compiled from many sources, with credits identified. The contents

of this report is for reference only, not to be used as business advertisement

or to set standards on policies or actions. |