An insightful exploration into how certain business strategies can enhance the flexibility of companies while simultaneously increasing their financial reporting complexity.

The COVID-19 pandemic and the recent invasion of Ukraine are two prime examples of unanticipated shocks that have placed intense strain on companies’ financials. These events generated uncertainty and highlighted the importance of managing risks and being flexible. Financial flexibility can be achieved through retaining adequate cash reserves to handle any unforeseen obligation or constraint, or adopting a cost structure that allows the firm to withstand a sudden decrease in revenues without incurring hefty accounting losses.

Asset-light and free-orientated strategies

From a strategic standpoint, certain business models provide extra cash flows without necessitating large capital investments, leading to improved financial flexibility. A prominent illustration of this is found in the hospitality industry, where many firms have implemented asset-light and fee-oriented (ALFO) strategies over the past two decades.

This approach separates intellectual capital ownership from property ownership, allowing the company to concentrate on management contracts and franchising. For instance, Marriott was a pioneer in this field when it revealed in 1993 that its real estate would be spun off into a REIT (Real Estate Investment Trust). As per its 2021 annual report, 99% of Marriott’s properties are not owned. Similarly, it is estimated that around 93% of McDonald’s restaurants are owned by independent owners across the world.

Combination strategy

These ALFO strategies have clear advantages, such as outsourcing real estate risk (you no longer own the properties), enabling faster growth with fewer capital needs, and stabilizing cash flows. However, from a financial reporting perspective, the impact of adopting such strategies remains an open question. Indeed, in most cases, companies opt for what is known as a “plural form.” In other words, companies that employ an ALFO business model are seldom completely asset-light (i.e., pure form), and instead focus on a combination of strategies: ownership of their properties, property management, and franchising.

Financial reporting complexity

In a recent study, researchers from EHL Hospitality Business School and Grenoble Alpes University set out to explore the connection between the adoption of ALFO strategies and financial reporting complexity. The underlying idea was that adopting ALFO strategies may add a layer of complexity to the firm’s existing ownership-oriented business model.

In a first step, the authors ran interviews to gain insight into audit experts’ views on the matter. The study identified factors that may lead to additional complexity and potentially make auditors’ work more complex and arduous:

- The adoption of a new business model requires additional auditor expertise.

- ALFO-related contractual agreements are complex from both a legal and accounting perspective.

- There might be a lack of centralization within a given group.

- Revenue recognition becomes a key audit risk.

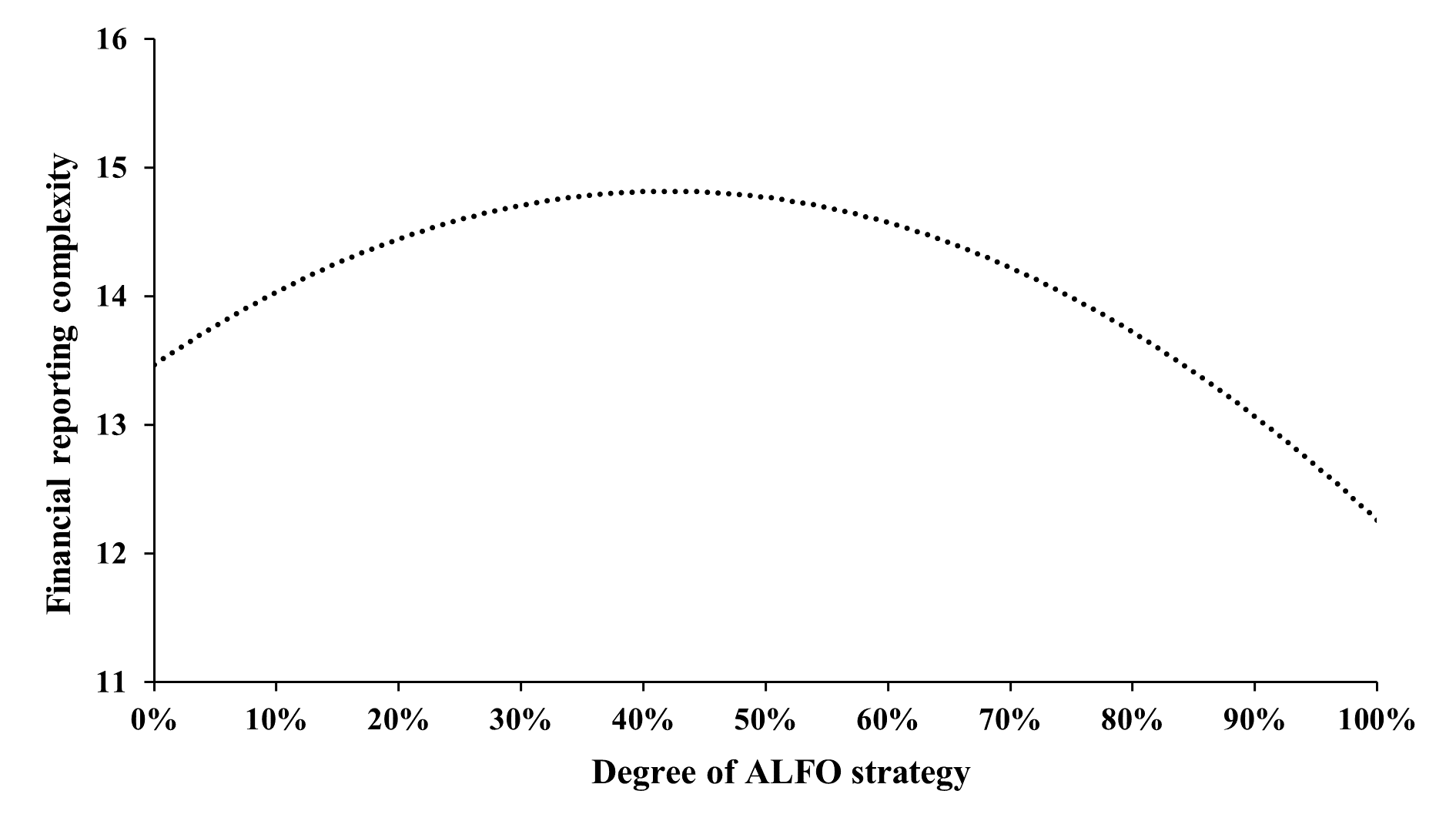

In a second step, the authors verified auditors’ expectations through an empirical investigation. Using a sample of listed hospitality companies in Europe and North America, their results show that financial reporting complexity increases with the implementation of ALFO strategies, up to a certain threshold. Beyond that threshold, the more prevalent the ALFO strategies, the lower the complexity, as the firm moves closer to the “pure form.”

Overall, as shown in the figure below, the association between financial reporting complexity and ALFO strategies follows an inverted U-shaped relationship.

Figure 1

Figure 1

Note: Financial reporting complexity is proxied by the natural logarithm of audit fees. The degree of ALFO strategy is the fee-income ratio, calculated as (franchise fees + management fees)/total revenue. Adapted from Poretti et al. (2023).

Maintaining high quality information

To conclude, ALFO strategies provide firms with greater flexibility, enabling them to reduce their vulnerability to economic downturns. However, the related costs should not be overlooked. The incremental financial reporting complexity induced by the pursuit of ALFO strategies must be taken seriously, as greater complexity may lead to lower transparency. From an investor standpoint, having access to accurate and reliable information is crucial, meaning that, when complexity increases, the responsibility falls on auditors to ensure that financial information is indeed accurate and reliable.