By Nicole Perreten

Another year has passed where the serviced apartment sector was able to consolidate its position in the lodging sector. This year’s article looks at the recent trends, discusses our analysis of the 2017 survey results and recent transaction evidence, and provides an outlook of the coming months in terms of pipeline.

HIGHLIGHTS

We conducted a new survey this year, which analysed a number of different operating characteristics and, while some show a clear commonality across the participants, many vary according to the brand and are therefore heavily driven by the operators’ strategy, were it to target the traditional long-stay market or, contrarily the short-stay market, bearing more characteristics with a hotel operation.

Operators seem to get more creative with their product offering as they grow their portfolio. Recent additions to the sector showed that some have added more common spaces with communal dining areas at the expense of in-room kitchens, marketing them as a more affordable experience (or microapartments).

The branded serviced apartment sector is getting more crowded. Almost every established hotel group now has an extended-stay product and new kids on the block are rapidly appearing such as Base in Switzerland and Cityden in Amsterdam. Other, more distribution-focused groups such as Saco and Bridgestreet are also rapidly increasing their portfolio of managed properties.

Our analysis of Gross Operating Profit (GOP) margins revealed some impressive results. Nevertheless, the bandwith of GOP margins remains broad, confirming that some properties operate less profitably.

The serviced apartment pipeline remains strong and focused on Western Europe. As brands get more traction, new projects increasingly also appear in secondary cities and new markets. Franchising aids expansion; however, only the larger companies have so far relied on this while many groups manage, own or lease their properties. Ascott recently announced its move to franchising in Europe with two contracts for future Citadines in France.

Transaction evidence for serviced apartments exists but remains limited and often with little transparency in terms of the sales price. However, institutional investors are entering the sector, eyeing mostly brands with a solid track record.

We would like to thank all of the survey participants for their generous input into the study. Your opinions and experiences are crucial in facilitating understanding of this thriving sector. We urge more operators in the sector to recognise the value of sharing data to enable serviced apartments to gain more attention from potential investors.

Much has been announced in terms of product and brand expansion in the past year; we take a look at what has actually materialised.

CREATIVE SPACE: INNOVATIONS, OPENINGS, ANNOUNCEMENTS

Bridgestreet opened its first Stüdyo serviced apartment in Paddington, London in March 2017. The affordable brand offers rooms fitted with the essentials and shared common spaces (including kitchen). Later this year, Bridgestreet will open its Stow-Away property in Waterloo consisting of 20 prefabricated modular microapartments.

Saco Apartments rolled out its first Locke properties in Aldgate, East London, in October 2016 and Edinburgh in June 2017. The design-led brand takes inspiration from the local neighbourhood and community.

Visionapartments has become the first serviced apartment provider to accept payment in Bitcoins and, as such, follows a global trend of making the ‘digital currency’ more readily usable. Long-stay travellers (a month and more) can equally benefit from a new partnership with topbonus, Air Berlin’s frequent flyer programme.

Go Native has recently strengthened its position in the private rented sector (PRS) with a series of management contracts secured in London and Manchester. According to Guy Nixon, the brand’s CEO, it is likely to see other serviced apartment brands move into this space, as PRS constitutes an enormous market and has many similarities to the operation of serviced apartments.

NEW BRANDS AND CONCEPTS

Adagio, a comparatively ‘historic’ aparthotel brand, revealed its new look with the opening of the Adagio Edinburgh Royal Mile in November 2016. Not only is the interior design of the units more contemporary, Adagio has also added an open lobby concept, demonstrating that it remains up to date with recent hotel trends.

Ascott has announced its new lifestyle brand lyf (pronounced ‘life’) ‘designed for the millennial market, including technopreneurs, start-ups and individuals from music, media and fashion’. To accurately cater for this segment, lyf properties will be managed by lyf Guards, millennials themselves, acting as community managers, city and food guides, bar keepers and problem solvers. The pipeline will focus on key gateway cities in Australia, France, Germany, Indonesia, Japan, Malaysia, Singapore, Thailand, China (where the pilot property will open in 2018) and the UK, aiming at opening 10,000 units by 2020.

A new concept – Livinghotel – has been implemented in Visionapartments’ newest additions to the portfolio. The apartments in Vienna and Vevey (both former hotels) will not have in-room kitchens, but will offer access to large public spaces with a shared kitchen where tenants can eat together; an interesting move, considering that an in-room kitchen was the original USP for the serviced apartment concept!

SURVEY RESULTS

During May 2017, HVS analysed data from 17 individual serviced apartment providers with a combined total of 17,150 units. The following paragraphs present our analysis of the aggregate data. Wherever there are sufficient data, we have provided more detailed or market-specific results.

Unit Mix

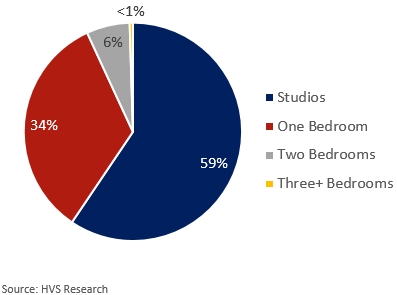

The room mix of a serviced apartment block plays a crucial role in optimising performance results. Some brands have therefore implemented certain ranges of apartment types to standardise their products [1] or to best adapt to their desired market segmentation [2]. Others remain more flexible and adapt to the opportunity and the market. On average, our sample suggests that almost 60% of units are made up of studios and approximately a third are one-bedroom apartments, with the remainder falling into larger unit types. Units with more than two bedrooms are rare and only exist where the appropriate target market is present.

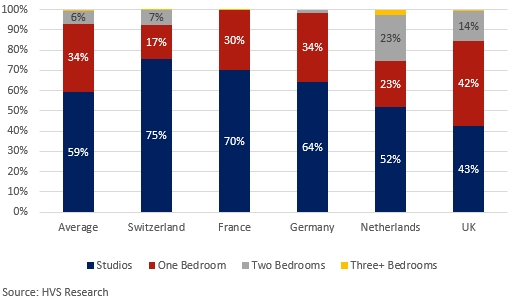

The breakdown by country provides further insights.

CHART 1: SERVICED APARTMENTS UNIT MIX

CHART 2: SERVICED APARTMENTS UNIT MIX BY COUNTRY

While the rooms mix of serviced apartments in France and Germany is broadly in line with the aggregate of the sample, Switzerland has a considerably larger proportion of studios, and serviced apartment units in the UK have a much smaller percentage of studios but a relatively high proportion of one- and two-bedroom apartments. Serviced apartments in the Netherlands (mostly Amsterdam) present the largest proportion of two+ bedroom units.

Minimum Stay Requirements

Serviced apartments were originally conceptualised for extended stay guests, often because of planning restrictions, but this has changed considerably and apartments have become popular with more transient guests as well, if local planning regulations permit it. It is therefore not surprising that more than 90% of our sample is reluctant to introduce minimum-stay requirements. The short-stay business also enables rooms to be filled between longer-staying tenants. Some providers impose a minimum stay of two nights over the weekend; one of our survey respondents, focused on the long-stay market, has a three-night minimum stay at all of its properties. Other, more specialised and upscale providers which cater to the traditional long-stay market require a minimum stay of 90 days.

Average Length of Stay (ALOS)

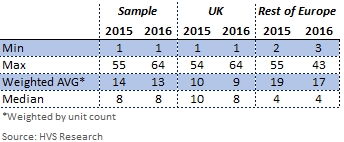

In relation to the minimum stay requirements, we also analysed the average length of stay.

CHART 3: AVERAGE LENGTH OF STAY ANALYSIS

The very low minimum of often one night confirms that certain serviced apartments operate much like a hotel, whereas the maximum of just under two months is more in line with the extended stay market definition and expectations. The following graph displays the distribution of stays across different bands of overnights.

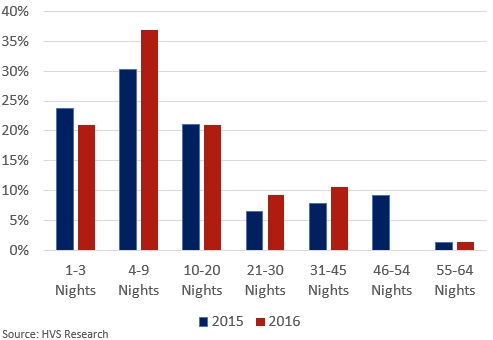

CHART 4: AVERAGE LENGTH OF STAY ANALYSIS

The largest block is made up of stays of between four and nine nights; 75% of the respondents had an ALOS of fewer than 20 nights in 2015 and this proportion increased to 80% in 2016.

It is apparent that vast differences exist in the average length of stay between different providers and locations. It is therefore difficult to conclude what dictates this key performance indicator in a serviced apartment unit. Our data show that certain brands put an increased focus on the short-stay market and therefore operate very much like a hotel. They run the risk of failing to benefit from the economic advantages arising from longer stays.

Staffing

Our data suggest that, on average, 17 guest-facing staff members (full-time employees – FTEs) were employed for every 100 serviced apartment units in 2016. No particular regional differences were apparent in our sample. Budget figures for 2017 indicate a slight increase in the average number of FTEs to 17.8. Staffing at serviced apartments can vary significantly; our sample covers a range of 2.3 to 32.1 staff members per 100 available units. These differences stem mainly from different operating models, such as having a more substantial food and beverage outlet (serving breakfast, for example), as well as a 24-hour manned front desk.

Travel Agent Commission

A substantial portion of serviced apartments, especially smaller, non-branded units and apartments focused on the transient market, are highly dependent on travel agents (including online travel agents – OTAs). On average, the commissions paid by serviced apartments represent 7% of rooms revenue with the majority falling within the 6%-10% range (52%) and the 1%-5% range (37%). We found no meaningful correlation between the commission percentage and the average rate or size of the property, although it is likely that brands with a strong track record or substantial supply are able to negotiate lower percentage commissions than the somewhat punitive 15%-25% paid by some.

Occupancy and Average Rate Performance

The following charts present an overview of the recent occupancy and average rate performance in the UK and the rest of Europe, as provided by our survey respondents [3]

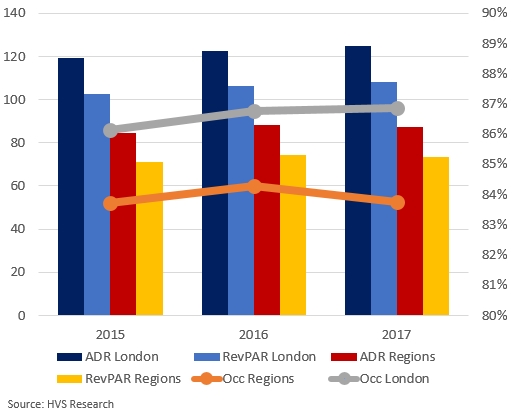

CHART 5: UK PERFORMANCE DATA (£)

Overall, the performance is encouraging in light of recent political events. The UK Regions and London recorded marginal growth in occupancy in 2016 and average rate growth of 3% and 4% for London and the regions, respectively. The devaluation of the pound in H2 2016 may well have helped the average rate, making the UK more affordable to European and US travellers. The outlook, however, remains more modest; flat growth is forecast for the regions and London’s serviced apartments are aiming at another 3% growth in average rate in 2017. The UK’s decision to leave the European Union could affect certain serviced apartments in the longer term, especially those focused on the corporate market, some of which may choose to move away from London eventually. However, it is too early to jump to such conclusions.

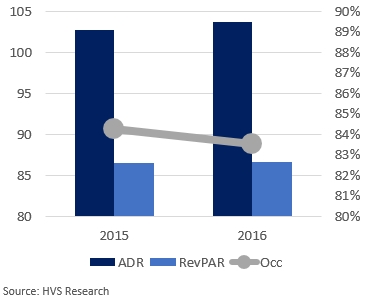

Our European sample has shown less movement; a small drop in occupancy in 2016 was offset by some growth in average rate. The sentiment for 2017 seems to be positive with budgeted growth in both occupancy and average rate.

CHART 6: EUROPE PERFORMANCE DATA (€)

TrevPAR

Unsurprisingly, the difference between TrevPAR [4] and RevPAR is marginal as many serviced apartment providers do not offer significant restaurant and bar options. The difference between TrevPAR and RevPAR (that is, ancillary spend) appears to be slightly higher for the serviced apartments on the Contnent. While we do not have complete figures for 2017, operators seem to budget for a larger spend on other income with a widening gap between RevPAR and TrevPAR. With a growing trend of adding open lobby spaces and flexible food and beverage concepts, this dynamic may well become more significant in the near future.

GOP Margin

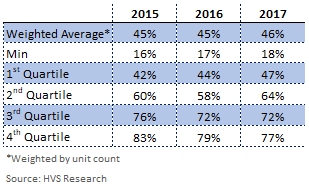

Conventional wisdom suggests that serviced apartments achieve a higher profit margin compared to hotels due to the reduced service offering and often the absence of any food and beverage outlets (and the associated labour cost). Our sample showcases a large range of GOP margins, from the high teens to the low eighties which is somewhat worrying (for the weaker performers). The median of the sample is approximately 60%; the trend in the first and fourth quartile indicate that the bandwith of margins is becoming smaller.

CHART 7: GOP MARGINS

Naturally, the GOP margin is positively correlated with average rate, RevPAR and the average length of stay. We found that the weighted average GOP margin for short stays (<5 nights) is 40%, 57% for stays between 5 and 15 nights and 78% for stays longer than 15 nights, confirming that longer stays make the operation more profitable. A negative correlation was found between the size of the units and staff members which is reasonable as labour costs can be a major expense in certain markets. Unsurprisingly, a strong positive correlation (~80%) was found between RevPAR and GOPPAR; that is, the higher the RevPAR the higher the GOPPAR.

EUROPEAN PIPELINE

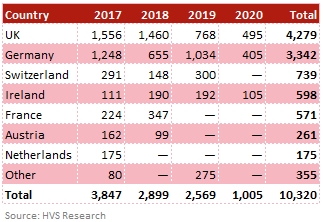

Some 10,000 serviced apartment units are currently in the pipeline in Europe, focused mostly on Western Europe. Eastern Europe, although becoming a hot spot for hotel investment, has so far benefitted little from the rise in serviced apartments. The majority (37%) of the pipeline should materialise in the remainder of 2017, 28% in 2018 and 25% in 2019. The fact that most projects we listed in last year’s article can still be found in this year’s update is reassuring and shows that little speculation exists when it comes to new developments. However, a considerable number of serviced apartments we were aware of last time experienced delays and are now scheduled to open at a later date. The size of the planned projects varies from as little as 18 units to blocks with 300 apartments; the average size is 120 units but the median of 80 suggests that the average might be skewed by larger projects.

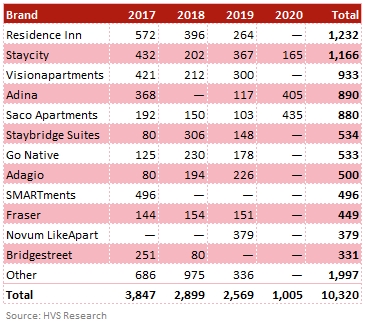

CHART 8: NEW SUPPLY (UNITS) BY COUNTRY

Unsurprisingly, the UK and Germany lead the pack, accounting for 41% and 32% of the pipeline, respectively. While London is the top spot for development in the UK (44% of the UK pipeline), Manchester, Edinburgh and other regional cities will also see openings in the near future. It appears that brands with a large presence in the UK are now venturing into Ireland, where development activity is heating up in Dublin. Germany presents a more balanced spread with Hamburg and Berlin (each at 14% of the German pipeline) representing the top destinations. Further, more hotel groups are jumping on the bandwagon to establish an apartment brand, such as Novum LikeApart by Germany’s fast-growing Novum Hotel Group. Switzerland comes third in the country ranking and the pipeline is almost exclusively driven by Visionapartments, which is already by far the largest serviced apartment provider in the country, but new providers such as Base are also appearing.

CHART 9: NEW SUPPLY (UNITS) BY BRAND

Residence Inn by Marriott currently has the largest pipeline with approximately a dozen hotel projects in Europe. The majority are franchised, allowing more rapid expansion, a contrast to the Marriott Executive Apartments where only a handful exist in Europe. Franchising can also help overcome certain expansion challenges in Europe, such as the fact that every European country has different planning laws (and potentially a different language and currency). With the recent Starwood takeover, Marriott also inherited the sustainability-friendly Element brand (currently only in Frankfurt and Amsterdam), but it remains unclear how its expansion will continue. Staycity is solidifying its position in Dublin, the UK and France while also expanding into Germany. Saco and Bridgestreet are now steadily bringing on stream their own concepts which were announced last year. Quest Apartment Hotels, an established serviced apartment provider in Australasia (recently backed by Ascott), is also eyeing a European expansion, focusing on primary and secondary cities in the UK, although no concrete project has been announced. Some of the more aparthotel-type brands are well suited for dual-brand projects, of which there are a few in the pipeline, especially if they are part of a larger brand portfolio, such as Residence Inn (Marriott) or Staybridge Suites (IHG).

TRANSACTION AND INVESTMENT ACTIVITY

The following table outlines recent, single-asset, serviced apartment transactions in Europe over the last 18 months, which are available in the public domain.

CHART 10: RECENT TRANSACTIONS ACROSS EUROPE (€)

The investor landscape is represented by developers, operators and institutional investors. The initial hesitance from the last towards serviced apartments is fading, especially when collaborating with well established brands with a good track record, as was the case for the Adina transaction in Nuremberg at the beginning of the year. Nevertheless, there is still limited transparency as few of the sales prices (or even the buyer/seller in some cases) remain publicly disclosed. SACO Property Group has secured a number of development sites, such as the Zanzibar nightclub in Dublin, where it plans some 100 units, as well as the Whitworth site in Manchester, subject to a complete refurbishment. Cycas Hospitality continues its expansion with the acquisition of the Staybridge Suites properties it operates in Liverpool in February 2016 and Newcastle in October 2016. On a corporate level, Ares acquired a 70% stake in Go Native in December 2016 for an undisclosed sum. US headquartered Ares is a publicly traded company and, with $100 billion of assets under management, one of the largest alternative asset managers worldwide. Its investment focus lies on three groups: credit, private equity and real estate.

CONCLUSION

The serviced apartment sector is steadily finding its place in the investors’ community as the pipeline is larger than ever and increasingly including secondary and tertiary markets as well as countries where the concept is somewhat novel. Survey results confirm that this product can be operated very efficiently with high GOP margins, a result of low staffing levels and few additional services. Nevertheless, more ‘hotel’ type services, such as open lobby or communal spaces, may become popular in the future. The high profitability, combined with the fact that many guests today recognise the benefit of apartments (in terms of size and pricing) bodes well for the continued growth of the serviced apartment sector.

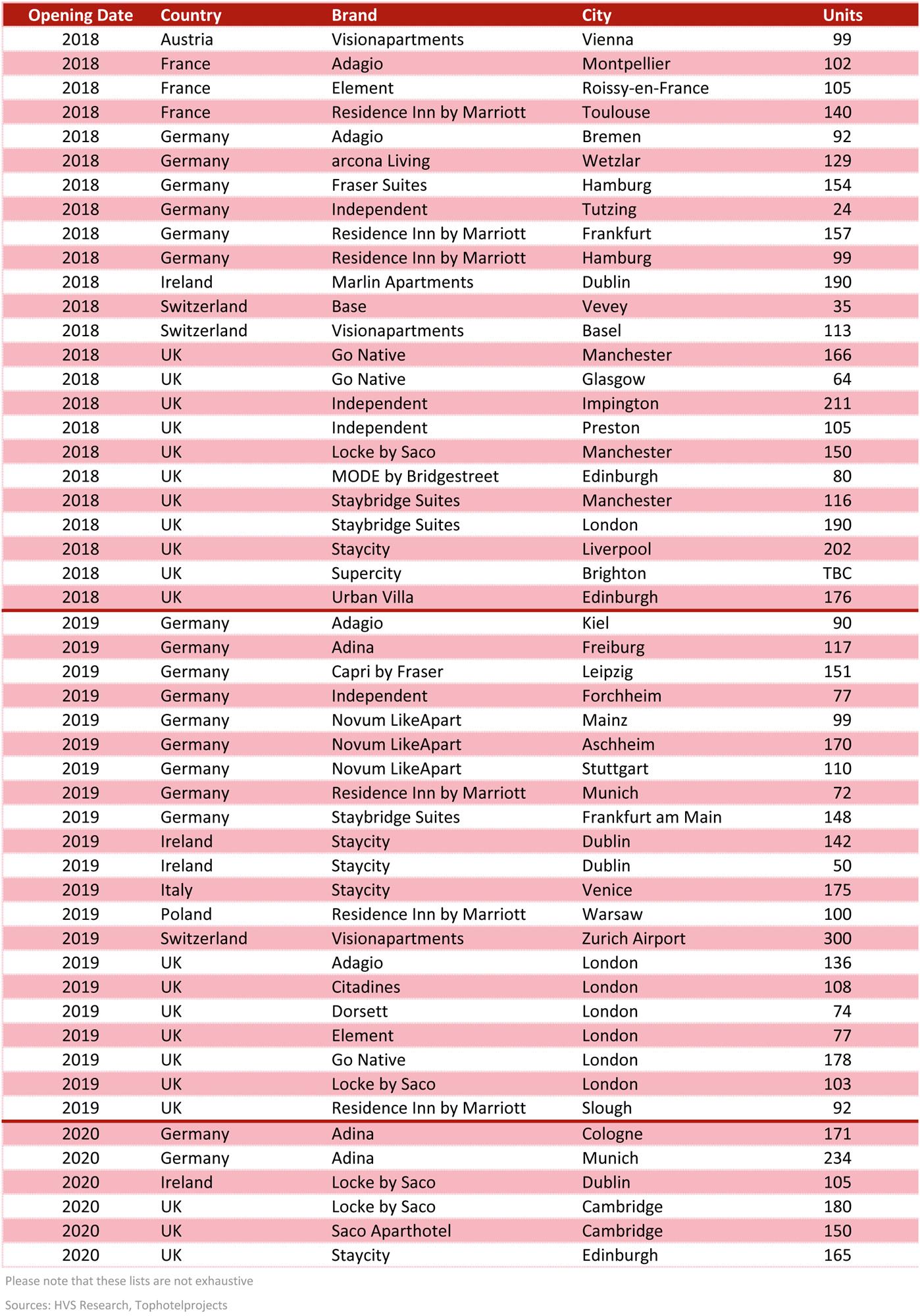

CHART 11: NEW SUPPLY PIPELINE ACROSS EUROPE – 2017 OPENINGS .jpg)

CHART 12: NEW SUPPLY PIPELINE ACROSS EUROPE 2018-2020 OPENINGS

1 Residence Inn’s typical room mix comprises 90% studios and 10% one-bedroom apartments (Source: Brand Factsheet) 2 Adagio assumes approximately 60% Business and 40% Leisure travellers (Source: Brand Factsheet) 3 We recognise differences between our survey’s data and those from STR’s benchmarking services are be due to sample differences. 4 TrevPAR represents total revenue per available room and, compared to RevPAR, can give a more complete view of a hotel’s performance.