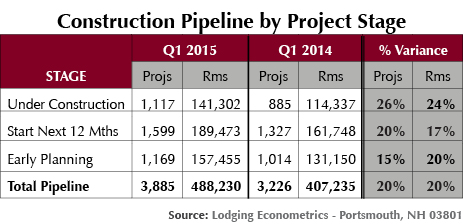

May 19, 2015 – PORTSMOUTH, NH – Now at 3,885 Projects/488,230 Rooms, the Total Construction Pipeline has shown seven consecutive quarters of growth, with the last three quarters posting Year-Over-Year (YOY) gains of 20% or greater.

The Pipeline is approximately half way though the expansion phase of the current real estate cycle but is still a third below the peak of 5,883 Projects/785,547 Rooms established in the first quarter of 2008. The Pipeline has at least two more years of rapid growth ahead before entering the maturity, or “topping out,” phase of the cycle. US Construction Pipeline

Projects Under Construction and those Scheduled to Start in the Next 12 Months, determine the amount of new supply entering the market over the next two years. Under Construction is at 1,117 Projects/141,302 Rooms and is up YOY, 26% and 24% respectively. Starts in the Next 12 months, at 1,599 Projects/189,473 Rooms, is up 20% by projects and 17% by rooms YOY. These stages are growing quickly but the totals remain considerably below the peaks established during the previous cycle.

Barring any exogenous event, everything suggests that there are a few more years of sustained profitability ahead before the flow of New Hotel Openings could possibly become problematic. This creates a significant window of opportunity for the industry considering that in the first quarter guest room demand at a 4.2% growth rate is running four times greater than new supply growth and other operating metrics – Occupancy, Average Daily Room Rate, Revenue Per Available Room and Profitability – are already at modern-day highs.

Interest rates remain low and the Fed’s hints of postponing increases until the fall bodes well for continued mortgage availability. Easy money has helped bolster transaction activity as increased buyer competition for prized assets has pushed up selling prices, making it more attractive for investors to build new projects rather than to buy existing hotels.

These signs guarantee that development will continue to accelerate until later in the decade when the real estate cycle will eventually peak. In a few years, looking backwards, these will be invariably regarded as halcyon days for hotel investors and operators.

UPPER MIDSCALE AND UPSCALE BRANDS ARE DRIVING GROWTH

More than 75% of the 3,846 projects in the Pipeline (not including casinos) are represented by two chain scales: Upper Midscale with 1,676 projects, is up 26% YOY, and Upscale with 1,249 projects, is up 24% YOY. Many of these projects are prototypical designs that enter the Pipeline in the Start in the Next 12 Months stage.

They are generally smaller projects with fewer than 200 rooms and have relatively short permitting and construction timelines that allows them to move quickly through the Pipeline. Upper Midscale and Upscale development will drive Total Pipeline growth through the remainder of the cycle’s expansion phase.

Of all the non-casino projects in the Pipeline, 79% have already made a branding decision. Within Upper Midscale, 22% have selected IHG’s Holiday Inn Express and another 21% have chosen Hilton’s Hampton Inn & Suites. Marriott’s Courtyard and Residence Inns combine to make up 29% of the brands chosen in Upscale while Hilton’s Homewood Suites and Garden InnPipeline Growth Chain Scaless account for a combined 23%.

Although having far fewer projects, Upper Upscale shows the largest YOY percentage growth rate, up 41%. Project counts for Upper Upscale usually start to accelerate after the expansion phase of the cycle is well underway. Projects are generally larger hotels, often part of mixed-use developments, have longer permitting and construction timelines and usually enter the Pipeline in the Early Planning stage.

Taking three or more years from announcement to opening, many Upper Upscale projects open quite late in the cycle, sometimes even after industry-wide operating declines have already set in.