By Mark Woodworth & Jamie Lane

For the past four years, there has been much to be happy about for most industry participants as the U.S. lodging industry recovered from the troughs of the Great Recession. As we enter the initial months of the New Year, there are many reasons to believe that 2015 will be another great year for most industry participants. We will likely see a record occupancy level achieved in the U.S. this year and conditions in the vast majority of markets will support aggressive pricing strategies. This should lead to the 5th consecutive year of significant room rate increases for most and contribute to another year of double-digit profit growth for the average U.S. hotel.

We at PKF Hospitality Research (“PKF-HR”), a CBRE Company, have been calling for a strong 2015 since the cows came home. This has been predicated, in part, on the slow, but relatively steady, upward trajectory of the domestic economy. Particularly important to hotels has been the consistent level of job growth over the past six months, and most economists expect greater levels of Gross Domestic Product (“GDP”) expansion this year and next. A new wildcard has surfaced of late: a rapid decline in the price of oil and, as a result, a significant drop in the cost of gas at the pump. Assuming that these conditions are sustained, what does this recent shift portend for U.S. hoteliers in the months ahead? We start our answer with a discussion of the contributing factors behind the lower price of oil.

The Return of Lower Oil Prices

Over the past six months, there has been a 58 percent decline in the price per barrel of West Texas Intermediate crude oil, which ranks as one of the largest oil price contractions in history. Moody’s Analytics attributes the drop in oil prices primarily to four factors:

1. 50 percent of the decline can be attributed to an increase in global supply. There were 1.7 million more barrels of oil per day in 2014 coming from the U.S., Iraq, and Libya alone.

2. 30 percent of the decline can be attributed to lower levels of demand. Importantly, expectations are such that the declining demand for oil in Europe, China, and Russia will persist, thus keeping oil prices lower for longer.

3. 15 percent of the decline is a result of the enhanced value of the U.S. dollar, the benchmark currency for setting oil prices globally.

4. The remaining 5 percent of the decline can be attributed to Geo Political Risk; i.e. ongoing instability in the Middle East.

Taking these factors in to consideration, Moody’s Analytics, in their expected case scenario (the outlook that informs our Hotel Horizons® lodging forecasts, expects that the price of oil will return to $80 per barrel by the end of 2015 and will average around $70 for the year.

Impact On Hotel Demand

History reveals that reduced oil prices will result in economic winners and losers. Generally, oil consumers gain and oil producers realize lower levels of economic activity. On net, however, Moody’s Analytics anticipates that these reduced oil prices will be a significant positive for the U.S. and global economies.

Looking at the impact of low oil prices on U.S. cites, the vast majority of major hotel markets will benefit from the price of oil being low. Conversely, energy dependent cities, most of which are found in the central U.S., will realize lower levels of employment and output growth in 2015. For example, in Houston, 3.9 percent of all jobs are related to the energy industry. While net employment growth in Houston will be positive once again this year, the current Moody’s forecast is half of what it was just 90 days ago. This will most likely cause us to lower our lodging demand forecast for Houston when our next forecasts are released in March 2015.

For most Americans, the effect will be felt at the gas pump, and lower oil prices will allow for reduced expenditures on gasoline. Consumer spending represents a significant portion of GDP and is an important contributor to the change in demand for hotel rooms. Moody’s Analytics estimates that consumer spending on gasoline, expressed as a percentage of GDP, will be approximately one-half of one percent lower in 2015 than in 2014. This savings will be most felt by automobile owners in states that have historically spent a higher percentage of their disposable income on gas than those in other states. Generally speaking, the winners will be those states in which getting from point A to point B requires more fuel. Thus, lower gas cost leads to greater savings and more money to travel. We expect some of these gasoline dollars to show up as an increase in demand for hotel rooms in the majority of the major hotels markets.

Moody’s Analytics current expected case scenario for the U.S. economy, in which oil is forecast to average $70 per barrel in 2015, calls for a 3.8 percent real increase in GDP for this year and another 4.4 percent growth in 2016. Should oil prices persist at an even lower rate, say $60 per barrel, there would be an additional boost from consumer spending on non-oil goods and services. Real GDP growth would average an additional one-half percent this year and next resulting in even higher lodging demand growth. Not all states will see the same benefit though. Nine out of the 50 states would realize lower levels of economic growth under this extended lower-oil price scenario, with one of those states being Texas. Many observers quickly think of Texas and the major cities therein as being particularly vulnerable as oil prices continue to decline. While true at the state level, it should be noted that markets such as Houston, Dallas, and Austin have diversified their economic base significantly over the past 20 years to the point that these potential negative consequences are mitigated.

Impact On Hotel Room Rates

Low oil prices could also affect the lodging industry by putting downward pressure on inflation. Year-over-year nominal changes in Average Daily Room Rates (ADR) are, in part, a function of the level of inflation realized during the period. Therefore, understanding what inflation is likely to be is paramount to the development of accurate ADR forecasts. Results of PKF-HR’s research demonstrate that a 1:1 relationship exists between the change in inflation and ADR during expansionary periods, holding the effect of occupancy constant.

Conclusions

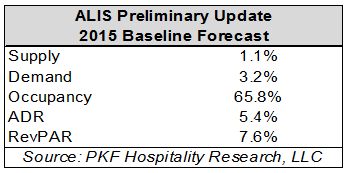

PKF-HR’s preliminary baseline forecast for 2015 (released at the ALIS conference in Los Angeles), which incorporates actual year 2014 data from STR, Inc. and Moody’s Analytics economic outlook as of January 2015, is summarized as follows:

So, if oil, and as a result inflation, stay low for longer, what are the implications on our baseline forecasts?

ADR: Lower oil prices create downward pressure on inflation. This would imply a lowering of nominal ADR growth. However, the higher levels of lodging demand resulting from greater amounts of income and GDP leads to increased scarcity in the market, and upward pressure on room rates. The net effect of lower inflation, combined with rising prices, is no change in the level of nominal ADR growth in our baseline forecast.

Occupancy: Low oil prices will contribute to higher income and GDP levels, which in turn should positively impact demand for hotels. Occupancy levels would be higher because of the greater levels of demand.

RevPAR: Higher expected occupancy levels, plus no change in the outlook for ADR, leads to a slightly greater level of U.S. RevPAR than that called for in our baseline scenario.

In conclusion, with oil prices currently under $50 per barrel, we place a slight positive bias on our current forecasts given the possibility that we could see an extended period of low oil prices and, as a result, lower inflation.