Real estate indicators from HFF managing director Max Comess and director Alexandra Lalos in HFF's Miami office.

Although debatable in terms of the national hotel market, one thing is for certain: We are in the early innings of a new cycle for the South Florida hotel market.

Looking back at history, Miami and its neighboring markets (Broward and Palm Beach over to Naples and down to the Keys) emerged from the Great Recession on the leading edge of the top 25 U.S. hotel markets and have generally been a leader in growth and forward indication of the broader national market this cycle. Miami has emerged as the No. 1 U.S. market for RevPAR growth so far in 2018, when STR data is adjusted for Super Bowl impact.

From January 2010 to December 2015, the Miami market saw RevPAR growth for 68 of 72 months. RevPAR peaked in February 2015 at $227.27, a 28 percent premium over its previous peak of $177.38 in March 2008. Indeed, Miami had transformed over the last cycle from an important national hotel market, comparable to Atlanta, New Orleans and Dallas, to a true global gateway market, comparable to London, Dubai and Hong Kong — in both the eyes of investors as well as hotel guests.

REIT, international and high-net-worth capital poured in to all of Florida, evidenced by our team’s transactions of the LaPlaya Beach Resort in Naples, purchased by Pebblebrook; the Shores Resort in Daytona, purchased by Taiwanese capital; and the Raleigh Miami Beach, purchased by Tommy Hilfiger. Traditional capital seeking more near-term yields migrated to the urban nodes (cities within our cities) like Dadeland, Doral, Aventura, Sunrise and Plantation.

And then, as 2015 came to an end, the music stopped. Miami entered a downturn.

In the first four months of 2016, as the broader U.S. hotel market saw a RevPAR increase of 3.3 percent, Miami saw a decrease of 4.6 percent. At the time, we referred to it as a “plateau” – Miami’s hotel market had reached maturity and the performance was “bouncing around the top” with such volatility to be expected.

However, by the second quarter of 2016, it was becoming evident that there were systemic issues beyond the volatility associated with a heated market.

It was a four-pronged harpoon that took our market down: a strengthening U.S. dollar and divisive political campaign season that chilled international demand, a convention center in Miami Beach that went offline for a long-term renovation and expansion, the black swan event of the Zika virus and a wave of new supply all hit at once.

Currency Dynamics

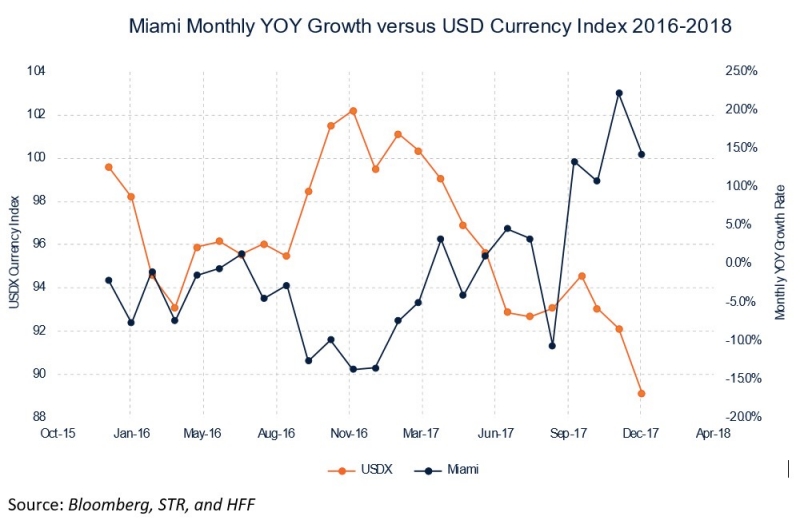

Beginning in April 2016, the U.S. dollar began an eight-month rally increasing more than 10 percent according to the USDX index. This run up in the dollar made Miami’s hotel rooms and luxury condos that much more expensive for foreign visitors, including those from Brazil (Miami’s No. 3 top international feeder market) whose currency declined by 33 percent over roughly the same period, leading to a 26 percent decline in Brazilian arrivals to Miami in 2016. As evidenced in the chart below, Miami’s RevPAR is inversely related to the strength of the USD. As the dollar has weakened in 2017, RevPAR has begun to grow again.

Miami Beach Convention Center

Demand was further chilled by the convention center in Miami Beach going offline for a multi-year $620 million renovation and expansion. When completed in September 2018, Miami Beach will have a truly world-class facility that should position Miami Beach on par with other world-class convention destinations and substantially drive group demand, increasing the market’s already strong base of business and helping drive RevPAR across all hospitality segments. However, the temporary darkening of this antiquated facility certainly did not help in 2016-2017, as much of the convention business was diverted to other cities.

The Zika Virus

The black swan was a pathogenic mosquito-borne illness known as the Zika Virus. What came across as mild flu-like virus to most, Zika had a particular risk to pregnant women and those trying to have children. Although no cases of birth defects are known to have occurred at any point in Florida, horrific images of Zika’s effect on babies in other parts of the world were forefront to the traveling public. Areas where Zika mosquitos had been captured beginning in July 2016 —Wynwood and Miami Beach — became ghost towns with occupancy plummeting. Virtually all demand segments swore off Miami, and many avoided Florida altogether. While it’s very difficult to quantify the economic impact of Zika, some point to a decrease of seven percent in hotel tax collections in Miami-Dade in 2016 as a tell-tale sign of its effect, though it’s impossible to quantify the lost business that didn’t book in the first place.

Supply Growth

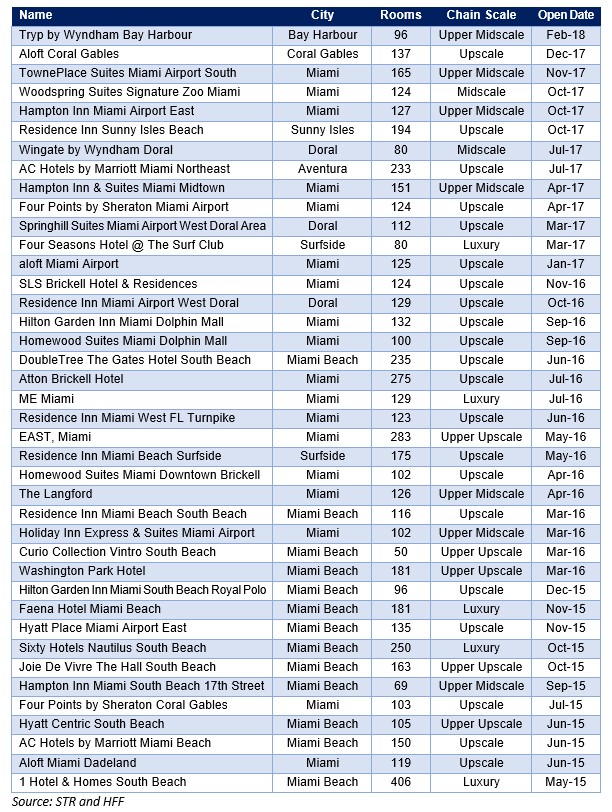

To make matters worse, amid declining demand, South Florida was experiencing its cyclic peak of new supply deliveries. Notably, this new supply was spread across all segments. Supply increased by 3.6 percent and 4.2 percent in 2015 and 2016, respectively, before declining to just 3.2 percent growth in 2017. As evidenced in the following chart, much of the new supply on Miami Beach was delivered in 2015 and early 2016, whereas the remaining new supply was focused in nodes like Brickell, Doral, and the airport market. Additionally, much of the new supply came in the upscale select-service segment which accounted for approximately 3,500 rooms. While some sources forecast supply growth of six percent in 2018, HFF’s research finds that only approximately 2,000 rooms are under construction with 2018 opening dates, which translates to 3.6 percent supply growth in 2018.

Notable New Hotels to Deliver

It was a classic, falling-knife scenario: New hotels were coming online and immediately having to discount rates to try to catch whatever dwindling demand they could. Existing properties had to choose whether to hold the line and lose occupancy or succumb to the strong ADR pressure presented by this new supply and further undercut by aggressive OTAs and AirBnB.

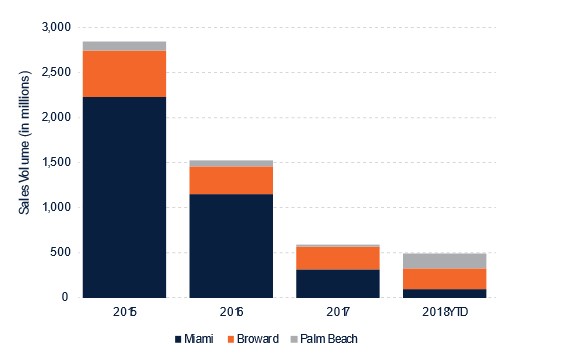

The downturn was felt equally in the transaction and capital markets. Buyers looked elsewhere. For the first time in over a decade, Miami was redlined in many investment committees. Wall Street analysts who a short while ago chastised REITs from not having enough Miami presence were now cautioning the same companies for their “heavy Miami exposure.” Transaction activity plummeted, and sellers withdrew from the market, opting to either hold assets longer term or refinance in lieu of divesting.

South Florida Hotel Sales 2015-2018

Source: Real Capital Analytics (RCA) and HFF Research

Source: Real Capital Analytics (RCA) and HFF Research

The Recovery: Headwinds have become Tailwinds

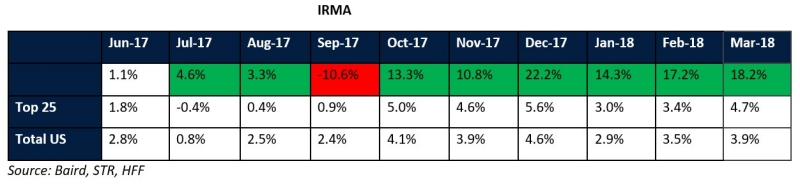

The silver lining to all of this is that the Miami hotel industry is experiencing a strong comeback in response to the headwinds of 2016 and 2017. A comeback that began in July and has exhibited a resurgence since Hurricane Irma. Miami has been one of the top five RevPAR growth markets in the country since July, with the exception of the month of September as a result of Hurricane Irma, and posting double digit RevPAR growth percentages. Many hotels on Miami Beach are reporting a record-high season so far in 2018.

Note that red means that it is in the worst five U.S. markets for decline, with green being the strongest five U.S. markets for gain.

Top Storylines to play out in 2018:

What’s Zika? South Florida is cool (and safe) again. The Zika Virus, in the parlance of our times, turned out to be “fake news.” Luckily, the market has moved on, and visitors seem to be unafraid of visiting South Florida. Thanks to a strong upcoming schedule of events in South Florida, the lodging industry is expected to continue to benefit.

Major additions to infrastructure and airlift continue to position all of South Florida as a Global Gateway. The opening of the Brightline Express Train will connect South Florida in a way we’ve never seen before and allow the tri-county area to experience a “borderless” exchange of tourist and corporate demand. Shifting airport demand between Miami International (MIA) and Fort Lauderdale-Hollywood (FLL) targets new sources of demand, including the Middle East (Emirates to FLL), Israel (El-Al to MIA), Nordic Europe (SAS to MIA) and expansion of domestic and Caribbean routes at both MIA and FLL. In 2017, FLL posted record passenger traffic of 32.5 million, an 11.3 percent increase year-over-year. The traditional borders between teh South Florida hotel markets of Miami, FLL and Palm Beach will continue to “blur,” making the entire South Florida market akin to a “SoCal” or “Bay Area” super MSA.

Strong Q1 performance will drive hotel transactions, benefit of South Florida “exposure” for the entire year. Public and private companies across South Florida are anecdotally noting that their first quarter performance was “the strongest season in a decade.” Pebblebrook’s early earnings memo noted that their “South Florida exposure” was a key reason for their stock’s recent outperformance, a stark contrast to many analyst reports over the past two years that noted South Florida exposure as a negative and not the positive that it is today. With exceptional trailing performance and increasingly positive revised 2018 reforecasts, we anticipate a strong uptick in transaction activity in South Florida. Trades such as the Ritz-Carlton Sarasota, Margaritaville Hollywood and Hilton Marina Fort Lauderdale, along with HFF's pending financings of numerous luxury resorts in South Florida, will add further evidence that the region has once again become a top priority for equity and debt investors.

Hurricanes continue to benefit South Florida. In the wake of the storms' destruction, the resilience of communities that followed is shown in the numbers. With the broader Caribbean markets still in recovery mode, a substantial amount of demand is being re-accommodated throughout South Florida. The strong performance of Miami hotels during and immediately after the hurricane, the replacement of lost revenue through business interruption insurance and the hundreds of hotels currently being renovated and upgraded (particularly in the Keys) are universally leaving the region’s hotel market better off than before the storm. As one local developer noted, “this hurricane [Irma] was really a blessing in disguise for hotel owners,” although we can’t help but acknowledge the devastation to families and their residences. We hope the strong recovery of the hotel sector will help employees as much as owners.

Currency exchange is back in balance and promoting the return of international capital.

Since mid-2017, the dollar has receded to exchange rates last seen in 2015. As reflected in the graph above against the Euro, the current trend has reopened international feeder markets to Miami. Anyone who has traveled to South Florida in the first quarter of 2018 cannot help but notice the abundance of foreign travelers who have been largely absent for the past two seasons.

The message we glean from this research is that it is truly a new cycle for South Florida’s hotel industry. Mirroring the recovery in 2010, South Florida is proving resilient once again and has more sophisticated offerings and amenities to offer travelers than ever before. It is exciting time to invest, reinvest and travel to South Florida.