Jeremy Teo and Hok Yean Chee

The Federation of Malaysia, located in Southeast Asia, comprises 13 states and three federal territories covering a total area of 329,847 square kilometres across Peninsula Malaysia and East Malaysia.

The Federation of Malaysia, located in Southeast Asia, comprises 13 states and three federal territories covering a total area of 329,847 square kilometres across Peninsula Malaysia and East Malaysia.

Malaysia’s population is approximately 31.4 million (2017 government estimate) with 62% being of Malay heritage. The country’s diversity is reflected in the share of different ethnic groups, such as Chinese, Indians and Indigenous, in its total population.

According to the World Travel & Tourism Council (WTTC), the direct and total contribution of Travel & Tourism to Malaysia’s Gross Domestic Product (GDP) was 4.9% and 13.4%, respectively of the total GDP in 2017, making tourism one of the key supporting industries by the economy.

In May 2018, Pakatan Harapan (PH) took over the office from the United Malays National Organisation (UMNO) party and its Barison Nasional (BN) coalition government who has been in office since independence in 1957.

The change in government has ushered in a new era filled with optimism but uncertainty about the direction that the country is headed for. As of June 2018, GST has been abolished and several major infrastructural projects are under review as PH demonstrated a stern stance towards fiscal commitment.

Economy Performance & Outlook

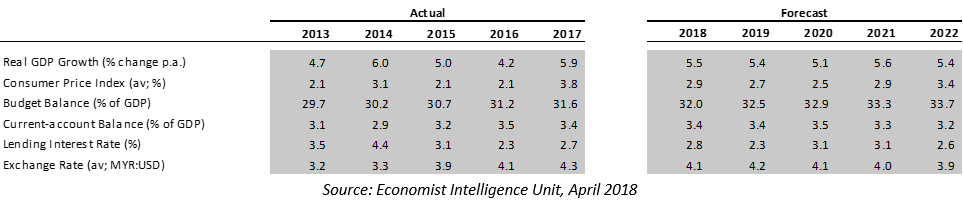

In 2017, Malaysia’s economy rebounded after the decline in 2016 and recorded GDP growth rate of 5.9%, on the back of stronger global economic performances. The growth was driven by the increase in manufacturing and services, as well as rebound in the agriculture sector. Seven states grew at a faster pace than the national growth (5.9%) in 2017 namely Sabah (8.2%), Melaka (8.1%), Pahang (7.8%), WP KL (7.4%), Selangor (7.1%), Johor (6.2%) and WP Labuan (6.1%).

Going forward, real GDP is expected to grow by an annual average of 5.4% from 2018 to 2022 with comparatively subdued demand for electronic and electrical goods, the nation’s largest export category.

Currency Exchange Outlook

Since 2016, a myriad of factors such as weak economic growth, reduce in crude oil prices, depleting foreign exchange reserves and a protracted political crisis over 1MDB has contributed to the weakening of the Malaysia Ringgit (MYR).

However, since the Trump administration assumed control in 2017, the United States (US) dollar has depreciated in an attempt towards reinvigorating the country’s manufacturing and exports. As a result, the US Dollar Index (USDX) declined by 11.2% in 2017. With the slide in greenback, Malaysian ringgit recovered from the 19-year low of 4.5 MYR:USD in January 2017 and ended the year with 4.3 MYR:USD.

International Relations

Malaysia’s relations with Singapore improved in recent years, particularly in the area of economic ties. The Johor Bahru-Singapore Rapid Transit System (RTS) Link Bilateral Agreement was signed in early 2018 and joint development projects such as Marina One project at Marina South and the DUO project at Ophir-Rochor were completed and met with great success.

In 2017, Malaysia strengthened relationship with US with both nations pledging to improve defense ties, including in the areas of maritime security, counterterrorism, and information sharing between security forces. China remains Malaysia’s largest trading partner since 2009.

Following the election held in May 2018, Malaysia underwent a change in government and the outlook for international relations is uncertain as it remains to be seen whether the incumbent government will take a different approach.

Figure 1: Key Economic Indicators

Outlook

Since taking over office, the ruling Pakatan Harapan (PH) coalition has abolished goods and services tax (GST) and reviewed spending pledges. Various infrastructural projects are under scrutiny with some possibly facing abandonment.

With the elimination of the MYR21 billion revenue expected to be generated by GST in 2018, the economy could be left overly reliant on the recovering global oil prices, a major source of revenue for the nation through petroleum tax and royalties.

Tourism Market Overview

In 2017, Malaysia remained the second most-visited South East Asian country after Thailand despite decreasing tourist arrivals. Travel and tourism directly contributed MYR66 billion to the country’s GDP, an increase from the MYR62 billion the year before, and equaled to the equivalent of 4.8% of the nation’s total GDP, according to the World Travel and Tourism Council’s data.

International Arrivals

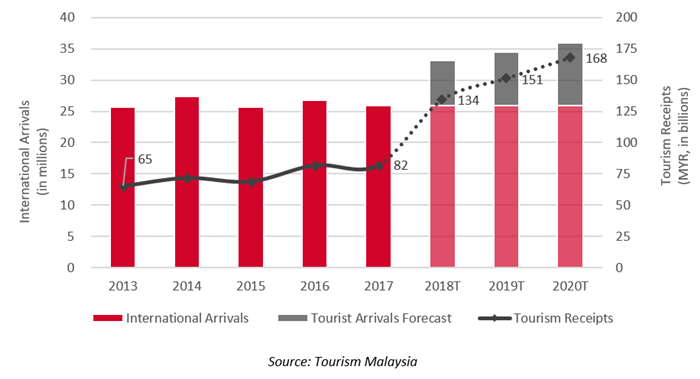

Despite a weak ringgit that was perceived to boost inbound tourism and having hosted the Southeast Asia Games, international arrivals in 2017 decreased by 3.0% year-on-year to 25.9 million, short of the 31 million target set for the year. The decline could be attributed to a lack of advertising and promotional activities, as reflected by the lower budget allocated for 2016 and 2017.

Going forward, the Tourism Malaysia Integrated Promotional Plan 2018-2020 has been formulated to tackle existing challenges and to improve Malaysia’s tourism performance. The plan highlights six strategies which includes optimising the use of techonology, leverage on upcoming major events, synergising with development of mega projects, enhancing initiatives made under the NKEA, maximising integrated marketing campaigns and promotion Malaysia as a filming destination.

Tourist Receipts

Despite a decrease in total tourist arrivals, tourist expenditure increased marginally by 0.1% in 2017 to reach MYR82.2 billion.

Along with the increase in total tourist receipts in 2017, average per capita expenditure increased by 3.2% to reach MYR3,166.

While the average length of stay decreased from 5.9 nights (2016) to 5.7 nights (2017), average spent per diem increased by 6.9% to reach MYR556 in 2017.

Going forward, Tourism Malaysia (“TM”) has set ambitious targets of MYR134 billion in tourist receipts for 2018, MYR151 billion in 2019 and MYR168 billion for 2020. In order to achieve 2020 target of MYR168 billion, tourism receipts must increase by 104.5% from the MYR82 billion achieved in 2017.

Figure 2: Total International Tourist Arrivals and Tourist Receipts

International Source Markets in 2017

Figure 3: Top Five Feeder Markets in 2017 (% share)

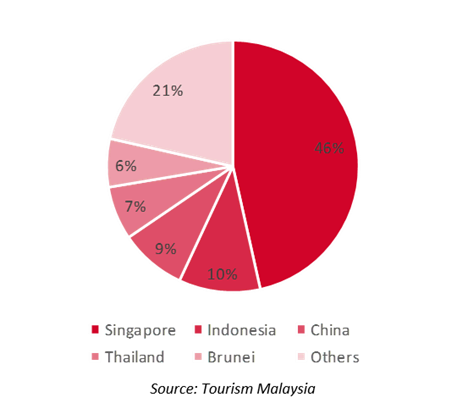

- Asian countries account for 92% of international arrivals

- Top five source markets account for 79% of international arrivals in 2017

- Changes to Top 10 source markets:

- Highest 2017 Y-o-Y increase: Brunei with 19.4%

- Highest 2017 Y-o-Y decrease: India with 13.4%, decrease for the third consecutive year

- UK is the strongest European country with 359,000 arrivals, representing 1.3% of total arrivals

- Singapore and Indonesia, the top two source markets, both recorded Y-o-Y decline in 2017

2020 Tourism Target

- Welcoming 36 million international passengers (expected 38.7% increase from 2017)

- Increasing arrivals from China to 8 million, a 300% increase from 2017

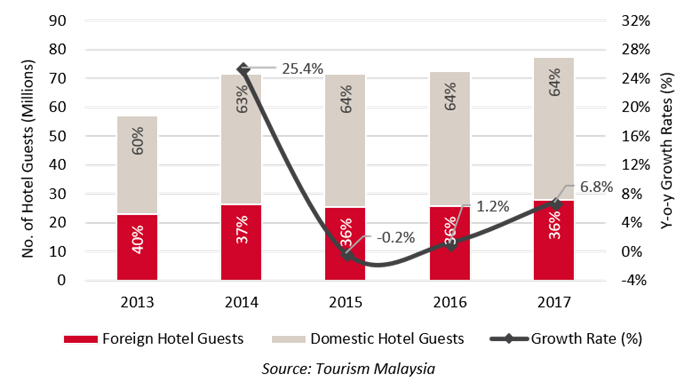

Hotel Guests and Tourism Promotion

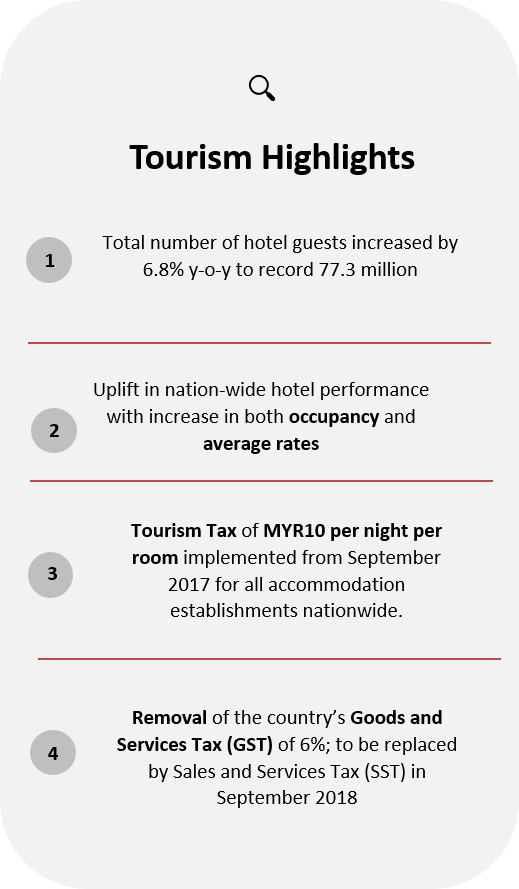

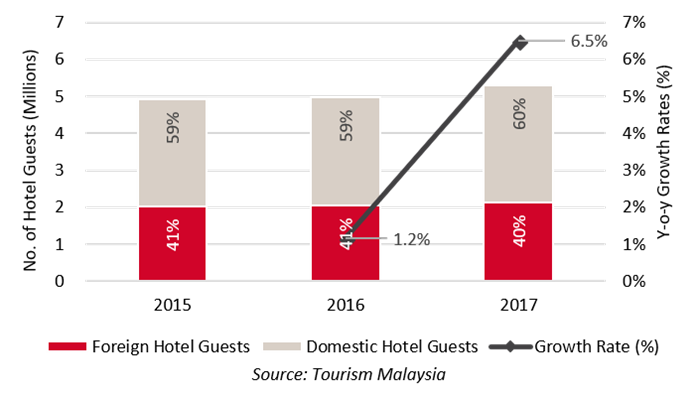

Although international arrivals decreased in 2017, total hotel guests in Malaysia increased by 6.8% y-o-y to 77.3 million from 72.3 million in 2016. Of the total 4.9 million increase in hotel guests, 2.1 million are increase in foreign hotel guests while 2.8 million are increase in domestic hotel guests. Historically, domestic hotel guests have always accounted for majority of the total guests and continue to do so in 2017 with 49.2 million, 64% of total hotel guests.

Figure 4: Hotel Guests in Malaysia (2013-2017)

Hotel Supply

From 2016 to 2017, hotel supply in Malaysia increased by 19 classified hotels to reach 4,980 hotels and 325,700 rooms.

To accommodate the estimated growth in tourist demand projected for the upcoming years (as highlighted in Figure 1), a significant number of hotel projects is expected to enter the market.

As of May 2018, an addition of 100 hotels, with 25,589 classified rooms have been publicly announced for the period of 2018-2022.

Figure 5: Existing tourism accommodation and future classified** hotel supply in Malaysia (2016-2022)

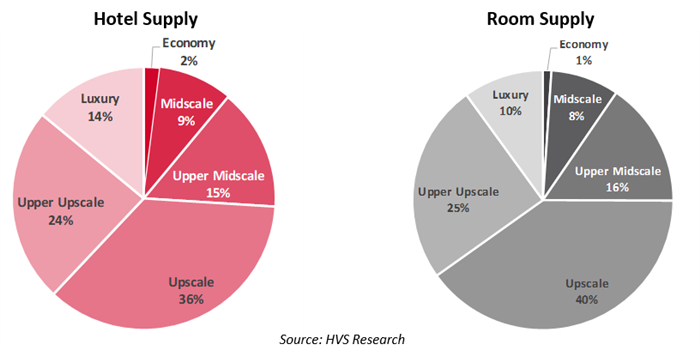

Classified Hotel Supply by Segment

Of the 100 hotels that will commence operation in Malaysia by 2022, majority belongs to the Upscale segment. Both Upscale and Upper Upscale hotels accounts for 62% of total additional hotel supply, amounting to a total of approximately 16,600 rooms.

While new luxury supply are only limited to 14 hotels, these includes debut for international brands such as Banyan Tree and W Hotels. Economy supply makes up the minority of new supply with two hotels, 270 rooms.

Figure 6: Future classified Hotel Supply by Segment (2018-2022)

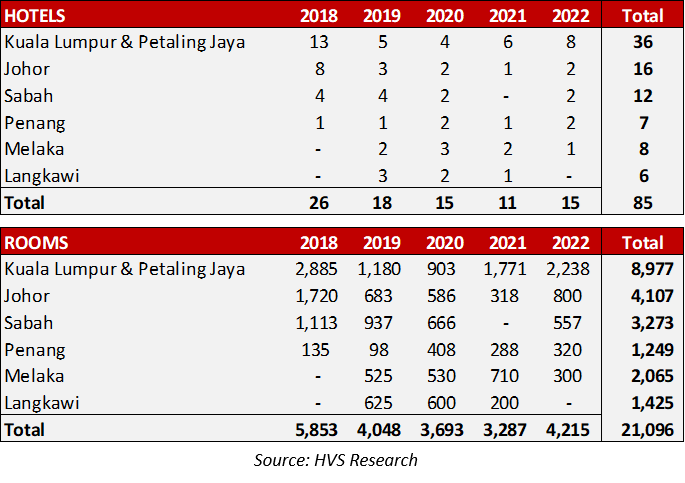

Classified Hotel Supply by State

In order to set the focus on regional highlights by State, the following tables highlight the six States with the most upcoming supply, accounting for 85% of total future hotel supply and 54% of new room supply.

Figure 7: Future classified Hotel Openings by State (2018-2022)

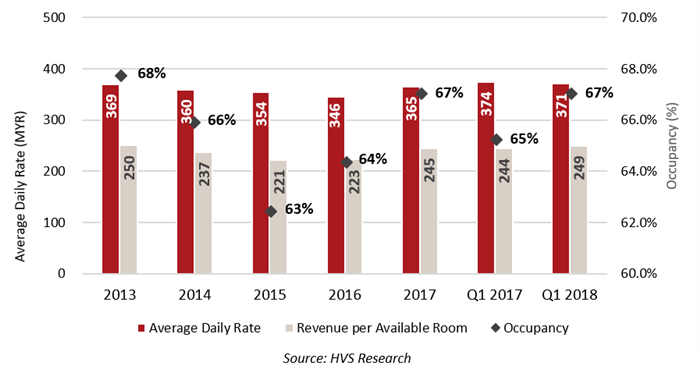

Hotel Performance

Despite the decrease in international arrivals in 2017, the increase in hotel guests to Malaysia translated into higher demand for tourist accommodations. As a result of accommodating the 77.3 million hotel guests with limited growth in supply (20 classified hotels in 2017), occupancy increased from 64% to 67% with average daily rates of hotels increasing by 5.4% y-o-y to MYR 365.

As of the first quarter of 2018, demand has remained strong with occupancy increasing by 21 basis point and average rate 0.7% higher y-o-y. Looking ahead, with main bulk of the supply coming on board in the second half of 2018, it remains to be seen if the demand will continue outweighing supply for the year.

Figure 8: Malaysia Overall Hotel Performance (2013-2017)

Destination Highlights – Johor Bahru

Johor Bahru is the capital of the Malaysian state of Johor located on the southern tip of Peninsular Malaysia. Acting as the Southern Gateway to Malaysia. With a land area of 1,064 km2 and population of approximately 1.33 million, the Johor Bahru district is famed for its rich culture and diversity in food. In terms of accessibility, Johor Bahru is well connected with Senai International Airport providing connection to 11 domestic cities in Malaysia and eight international cities in the Asia region.

Johor Bahru is the capital of the Malaysian state of Johor located on the southern tip of Peninsular Malaysia. Acting as the Southern Gateway to Malaysia. With a land area of 1,064 km2 and population of approximately 1.33 million, the Johor Bahru district is famed for its rich culture and diversity in food. In terms of accessibility, Johor Bahru is well connected with Senai International Airport providing connection to 11 domestic cities in Malaysia and eight international cities in the Asia region.

Hotel Guests

In 2017, total hotel guests in Johor Bahru increased by a 6.5% y-o-y, recording 5.3 million in 2017. Johor Bahru hotel guests are predominantly driven by the domestic market which accounts for 60% of total share, and represents 245,000 of the 324,000 increase in hotel guests in 2017.

Figure 9: Hotel Guests in Johor Bahru (2015-2017)

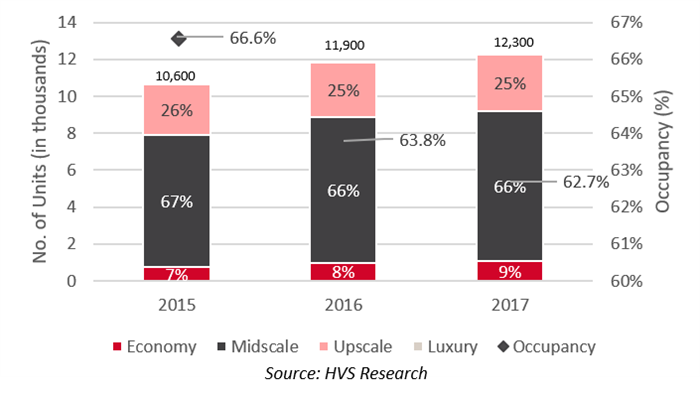

Classified Hotel Supply and Hotel Performance

From 2015 to 2017, total classified hotel supply in Johor Bahru increased by 15.2% to approximately 12,300 rooms. Most of the existing hotel supply are in the midscale segment with 66% share, while there is still no luxury supply in Johor Bahru. Occupancy in Johor Bahru decreased from 66.6% to 62.7% with the influx of new supply.

Figure 10: Classified Hotel Supply in Johor Bahru (2015-2017)

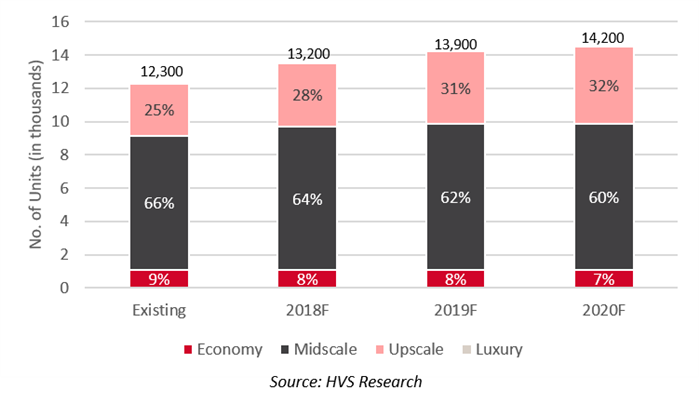

Supply Pipeline

With an increase in visitations to Johor Bahru translating to the increase in hotel guests, more international operators are also set to enter the region as they identify the rising demand for accommodation. Within the next three years, hotel brands such as Melia, Shama, Pan Pacific, Novotel, Hilton Garden Inn, Citadines, Holiday Inn and ibis Styles are set to debut in Johor Bahru.

Figure 11: Pipeline Classified Hotel Supply in Johor Bahru (Existing – 2020F)

Infrastructural Projects

Two key infrastructural projects that will provide a boost to the destination have been highlighted below:

Malaysia-Singapore Rapid Transit System (RTS)

- MYR4 billion investment

- Reduce congestion at border crossings between Singapore and Malaysia

- Slated to complete by 2024

Iskandar Malaysia Bus Rapid Transit (IMBRT)

- MYR2.6 billion investment

- Improve connectivity from Johor Bahru to Skudai, Johor Jaya and Nusajaya

- Phase 1 slated to complete by 2021

Outlook

Destination Highlights – Kuala Lumpur

Kuala Lumpur is the national capital of the Malaysia and is located centrally in the state of Selangor. With a land area of 243 km2 and population of approximately 1.79 million, Kuala Lumpur is often considered the cultural centre of Peninsular Malaysia. In terms of accessibility, Kuala Lumpur is accessible via Kuala Lumpur International Airport which is located 50 metres south of the capital and caters for 49 different international airlines.

Kuala Lumpur is the national capital of the Malaysia and is located centrally in the state of Selangor. With a land area of 243 km2 and population of approximately 1.79 million, Kuala Lumpur is often considered the cultural centre of Peninsular Malaysia. In terms of accessibility, Kuala Lumpur is accessible via Kuala Lumpur International Airport which is located 50 metres south of the capital and caters for 49 different international airlines.

Hotel Guests

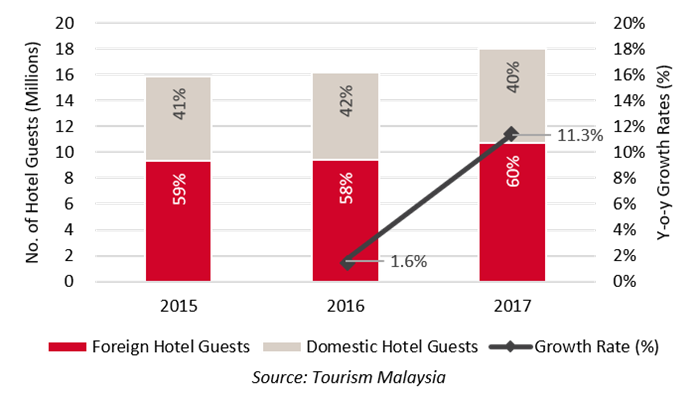

As the national capital, Kuala Lumpur is also the state with the most hotel guests in the nation. In 2017, total hotel guests increased by a 11.3% y-o-y, recording 18 million in 2017. Kuala Lumpur is the only state in Malaysia that has more foreign hotel guests than domestic hotel guests.

Figure 12: Hotel Guests in Kuala Lumpur (2015-2017)

Classified Hotel Supply and Hotel Performance

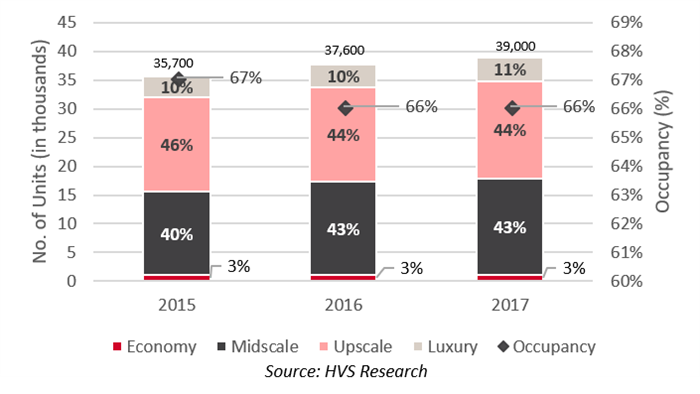

From 2015 to 2017, total classified hotel supply in Kuala Lumpur increased by 9.2% to approximately 39,000 rooms. Majority of the existing hotel supply are in the upscale and midscale segment with 44% and 43% share respectively. Occupancy in Kuala Lumpur decreased from 67.1% to 66.1% with the influx of new supply.

Figure 13: Classified Hotel Supply in Kuala Lumpur (2015-2017)

Supply Pipeline

The hotel industry in Kuala Lumpur is set to increase in competitiveness as existing hotels undergo renovations to remain competitive and new internationally-branded hotels enter the market. Within the next three years, four thousand additional rooms are set to be added, and the capital will welcome its first Park Hyatt, Four Seasons, Banyan Tree and W hotels.

Figure 14: Pipeline Classified Hotel Supply in Kuala Lumpur (Existing – 2020F)

Infrastructural Projects

Two key infrastructural projects that will provide a boost to the destination have been highlighted below:

High Speed Railway (HSR) Project*

- MYR65 billion investment

- Reduce travel time between Singapore and Kuala Lumpur to 1.5 hours

- Slated to complete by 2026

*Under review post May 2018 election.

Mass Rapid Transit (MRT) 2

- MYR32 billion investment

- Improve chronic traffic congestion in Kuala Lumpur

- Slated to complete by 2022

- MRT 3 scrapped after election

Outlook

Destination Highlights – Langkawi

Langkawi, the Jewel of Kedah, is a district and an archipelago of more than a hundred islands that is located west of the northern tip of Peninsular Malaysia. With a land area of 479 km2 and population of approximately 86,000, Langkawi is a tropical paradise that is recognized for its natural beauty and is Southeast Asia’s first UNESCO World Geopark. Langkawi is accessible via Langkawi International Airport which is currently served by six international and one domestic airlines.

Langkawi, the Jewel of Kedah, is a district and an archipelago of more than a hundred islands that is located west of the northern tip of Peninsular Malaysia. With a land area of 479 km2 and population of approximately 86,000, Langkawi is a tropical paradise that is recognized for its natural beauty and is Southeast Asia’s first UNESCO World Geopark. Langkawi is accessible via Langkawi International Airport which is currently served by six international and one domestic airlines.

Hotel Guests

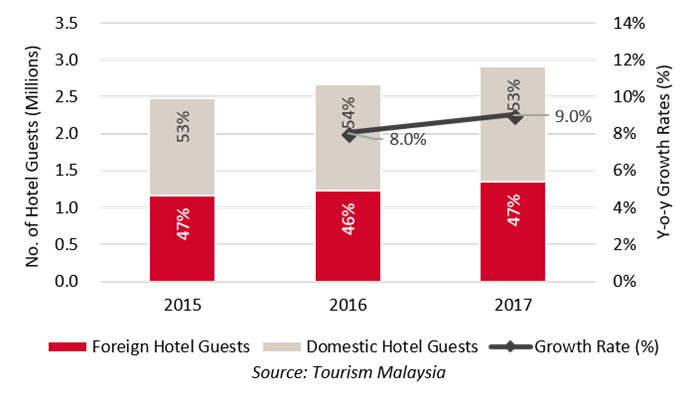

Besides Kuala Lumpur, Langkawi is the region with the second highest increase in hotel guests in 2017. The distribution of foreign and domestic hotel guests have remained at similar proportions since 2015 with both segments experiencing the similar level of growth throughout this period.

Figure 15: Hotel Guests in Langkawi (2015-2017

Classified Hotel Supply and Hotel Performance

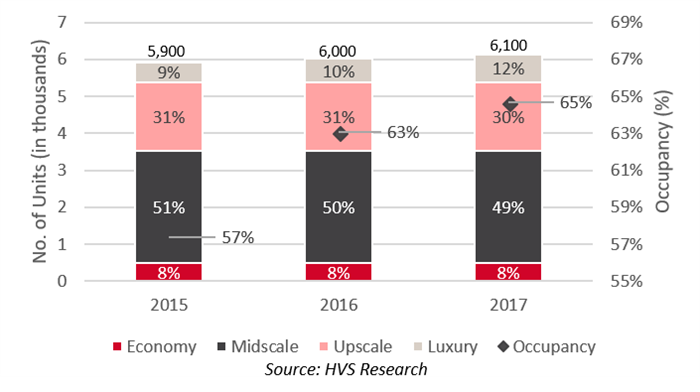

Approximately half of total classified hotel supply in Langkawi are from the midscale segments, which comprises mainly of independent branded hotels located in Kuah and Cenang vicinity. In 2017, Ritz-Carlton opened and increased luxury supply with 119 units. Over the last three years, occupancy has increased from 57% to 65%, indicating increasing demand for accommodation supply in Langkawi.

Figure 16: Classified Hotel Supply in Langkawi (2015-2017)

Supply Pipeline

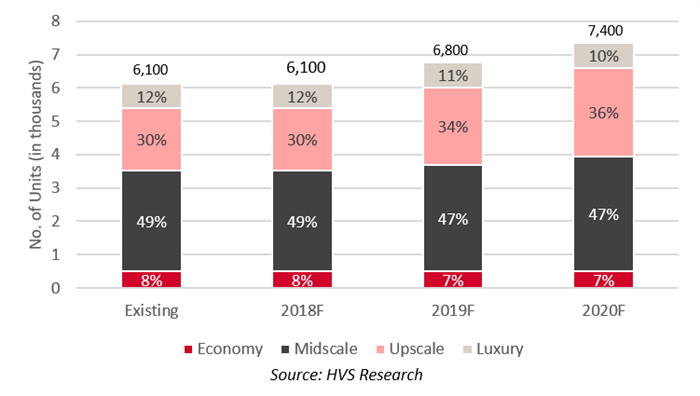

Over the next three years, total classified hotel supply in Langkawi will increase by 20% to 7,400 units. These include the additions of PARKROYAL, aloft, ibis Styles, Wanda and Mercure which will further expand on both the upscale and midscale hotel supply. As of now, no new luxury supply is expected to enter into Langkawi for the foreseeable future.

Figure 17: Pipeline Classified Hotel Supply in Langkawi (Existing – 2020F)

Infrastructural Projects

Two key infrastructural projects that will provide a boost to the destination have been highlighted below:

Langkawi International Airport Expansion Phase 1

- MYR89 million investment

- Expansion of the parking area

- To be completed in 2018

- Phase 2 to include construction of aerobridge

Tropicana Cenang

- MYR1.94 billion gross development value

- 1,102 residences and 350 hotel rooms with retail components

- Slated for 2023 completion

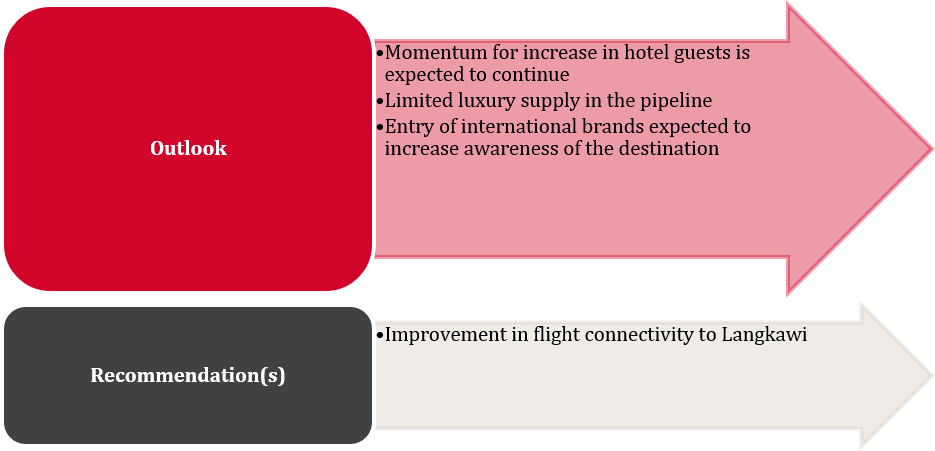

Outlook

Destination Highlights – Penang

The state of Penang is situated on the northwest coast of Peninsular Malaysia. The region comprises of Penang Island, where capital city George Town is located, and Seberang Perai. With a land area of approximately 1,048 km2 and a population of 1.75 million, Penang is renowned for its diversity in ethnicity, culture, language and religion. In terms of accessibility, Penang International Airport provides direct access with 18 international airlines.

The state of Penang is situated on the northwest coast of Peninsular Malaysia. The region comprises of Penang Island, where capital city George Town is located, and Seberang Perai. With a land area of approximately 1,048 km2 and a population of 1.75 million, Penang is renowned for its diversity in ethnicity, culture, language and religion. In terms of accessibility, Penang International Airport provides direct access with 18 international airlines.

Hotel Guests

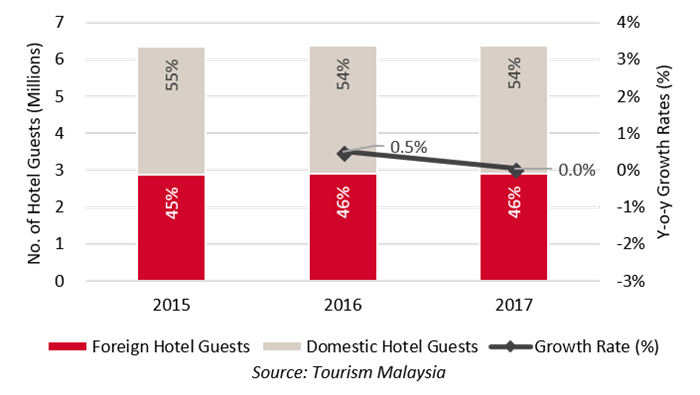

Hotel guests in Penang has experienced limited growth from 2015 to 2017. The state has approximately 2.9 million foreign hotel guests and 3.5 million domestic hotel guests throughout all three years.

Figure 18: Hotel Guests in Penang (2015-2017)

Classified Hotel Supply and Hotel Performance

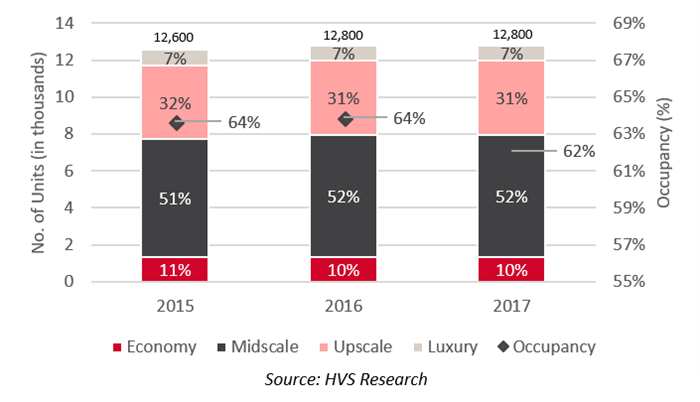

Along with the stagnation in hotel guests in Penang, classified hotel supply has remained fairly stable from 2015 to 2017. Over the three years, the addition to supply are the 10-key Jawi Peranakan Mansion and the 222-key Lexis Suites Penang. Market-wide occupancy decreased from 64% in 2016 to 62% in 2017 to reflect the lack of demand growth and the increase in supply.

Figure 19: Classified Hotel Supply in Penang (2015-2017)

Supply Pipeline

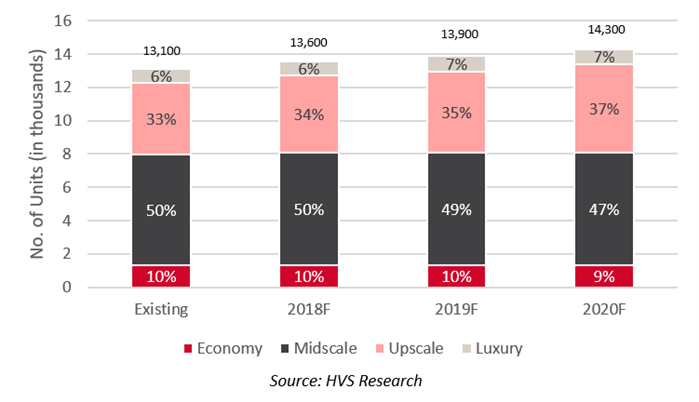

The Penang hotel market will receive a boost from the additions of several internationally-branded hotel supply over the next three years. These include brands such as Doubletree Resort by Hilton, OZO, Angsana, Courtyard, Citadines and Capri by Fraser. As of 2017, approximately 60% of total existing supply are operated by non-international operators.

Figure 20: Pipeline Classified Hotel Supply in Penang (Existing – 2020F)

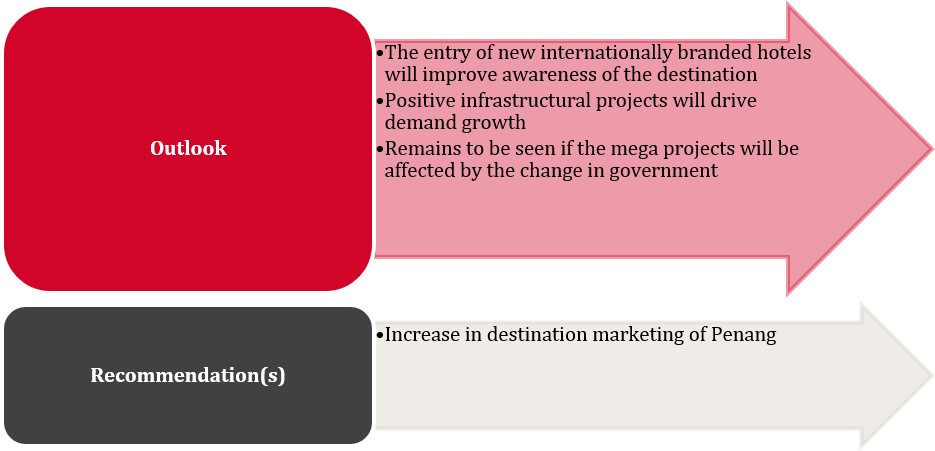

Infrastructural Projects

Two key infrastructural projects that will provide a boost to the destination have been highlighted below:

Penang’s mega projects

- MYR46 billion investments

- Construction of underwater tunnel, three major highways, Southern Penang reclamation projects, Penang Sky Cab and Light Rail Transit (LRT)

Penang International Airport Expansion

- MYR700 million investment

- Double capacity to 12 million passengers

- All three phases to complete by 2029

Outlook

Investment

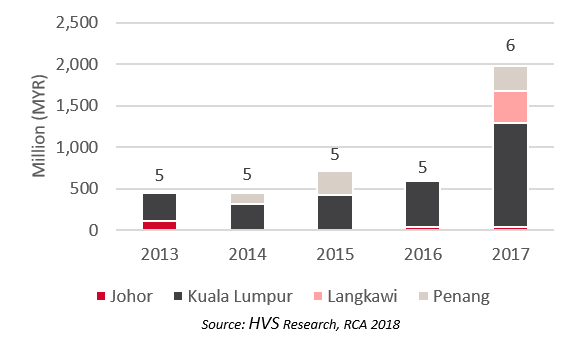

In 2017, total volume hotel investments across Malaysia recorded a new high of approximately MYR1,974 million. The sale of the Renaissance Kuala Lumpur for MYR765 million accounted for 38.8% of the total amount. All 6 publicly available hotel transactions in the year took place across the four regions covered in our destination highlights, possibly indicating investors’ interest in these area.

The most noteworthy findings in 2017:

Four Seasons Resort Langkawi

- First Langkawi transaction in 5 years

- MYR4,224,000 per key, highest per key value historically

Transactions in Penang

- Most number of transactions in a state

- Transaction average MYR892,000 per key, higher than the MYR831,000 per key for Renaissance Kuala Lumpur

Figure 21: Publicly Available Hotel Transactions Across Four Selected Regions (2013-2017)

(Number of transactions per year)

Outlook

Despite recording a slide in international tourist arrivals to 25.9 million in 2017, the Malaysia Ministry of Tourism and Culture has set an ambitious target of 33.1 million arrivals for 2018, reflecting confidence for growth in arrivals in the near term. Contrary to international tourist arrivals, the domestically driven tourism market in Malaysia remains buoyant with total hotel guests increasing by 6.8% to 77.3 million.

The year also saw the introduction of 19 new hotels bringing 3,728 keys into the market. Notable additions include the first Element and first Sofitel hotel in Kuala Lumpur, and the 119-key luxury Ritz-Carlton Langkawi. Hotel performances across the nation demonstrated strong growth, with improved occupancy and average rate as compared to 2016 with RevPAR increasing by a significant 9.9% to MYR 245.

The strong growth and performance was reflected in the performance of both Kuala Lumpur and Langkawi as demand continues to outpace supply. However, in Langkawi, limited connectivity and the lack of infrastructural investments could curb the demand growth going forward.

Elsewhere, in Johor Bahru, hotel guests have increased significantly in 2017 and with exciting supply in the pipeline, the region is well primed to realise its potential as a regional hub. At the eclectic Penang, the hotel market has remained level for the past three years. However, the area will be revitalised with the improvement in accommodation supply and the mega infrastructural projects enhancing connectivity.

Going forth, the outlook for tourism industry remains optimistic. The market will likely benefit from the myriad of factors, including the abolishment of GST and improvement in flight accessibility to the country.