By Amy|2020-01-29T12:34:44-05:00January 28th, 2020|

Suzanne Mellen | January 28, 2020

Supported by lower interest rates, transaction activity held up during a year of uncertainty. This article addresses recent trends in hotel sales and capitalization rates, the course of hotel values since the last downturn, and the outlook for 2020.

By Suzanne Mellen

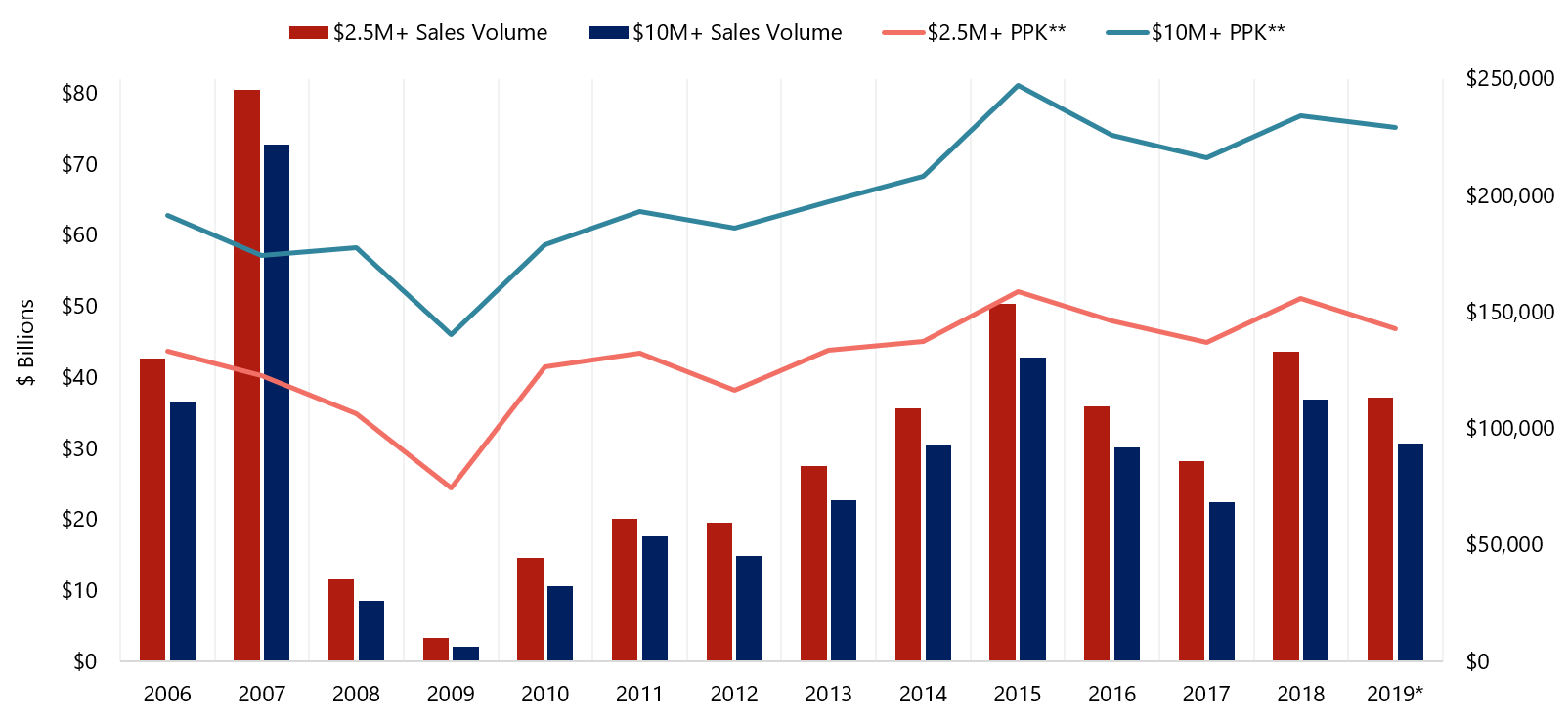

Despite increasing concerns about a global economic slowdown, the trade war, and geopolitical risks, the U.S. hotel transaction market remained healthy and active in 2019. According to preliminary data generated by Real Capital Analytics (RCA), total sales volume declined by 15%, from $43.6 billion in 2018 to $37.1 billion in 2019, though as will be illustrated, the decline was due primarily to lower portfolio sales activity.[1] Hotel owners took the pause in asset appreciation to winnow their portfolios, while buyers looking for higher yields pursued value-add opportunities. The lodging sector continued to attract interest from new investors looking for higher returns than those offered by other real estate sectors, and the availability of low-cost debt supported continued transaction activity.

The average price per key for all sales (price of $2.5 million and over) decreased by 8%, from $155,000 in 2018 to $142,000 in 2019, reflecting a smaller number of high-price per key deals. Total volume for hotels that sold for $10 million and over (major hotel sales) decreased by 17%, while the number of major hotels sold decreased by 11%, from 778 to 688, reflecting that sales of large, higher-priced deals slowed significantly. The major sales average price per key decreased by 2%, from $234,000 to $229,000. Sales volume for hotels that sold at a price of $2.5 million to $10 million remained steady at $6.8 billion, and the number of hotels sold and average price per key remained stable as well, at approximately 1,300 hotels and $57,000 per key, respectively. These metrics reflect the stronger activity sustained by the low end of the market. Owner-operators of smaller assets are typically less affected by global market concerns than investors of highly priced assets; these smaller deals are also easier to finance.

2019 U.S. Hotel Sales Transaction Volume and Average Price Paid Per Key

Source: RCA

Six hotels sold at a price of $1 million per room or greater, including the Montage Beverly Hills, which exceeded $2 million per room. Park Hotels & Resorts Inc. purchased Chesapeake Lodging Trust in a cash and stock transaction valued at approximately $2.5 billion, inclusive of closing costs. Blackstone acquired a 65% controlling interest in Great Wolf Resorts, also an entity transaction; approximately $2 billion of this acquisition was attributed to 17 whole or partial asset values by RCA. Other significant portfolios included Queensgate’s purchase of four Freehand hotels from the Sydell Group for $400 million, and Dune’s acquisition of 16 hotels from Starwood Capital for $332.2 million. Another major acquisition that was announced in 2019 was Mirae’s acquisition of 15 Strategic Capital hotels from Anbang, which acquired the portfolio in September 2016 for $6.5 billion. Mirae the winning bidder on the current deal at $5.8 billion, reflecting a 10.7% decline in value from the date of acquisition in the fall of 2016 (before any consideration of capital improvements during the ownership period)—an informative value trajectory.

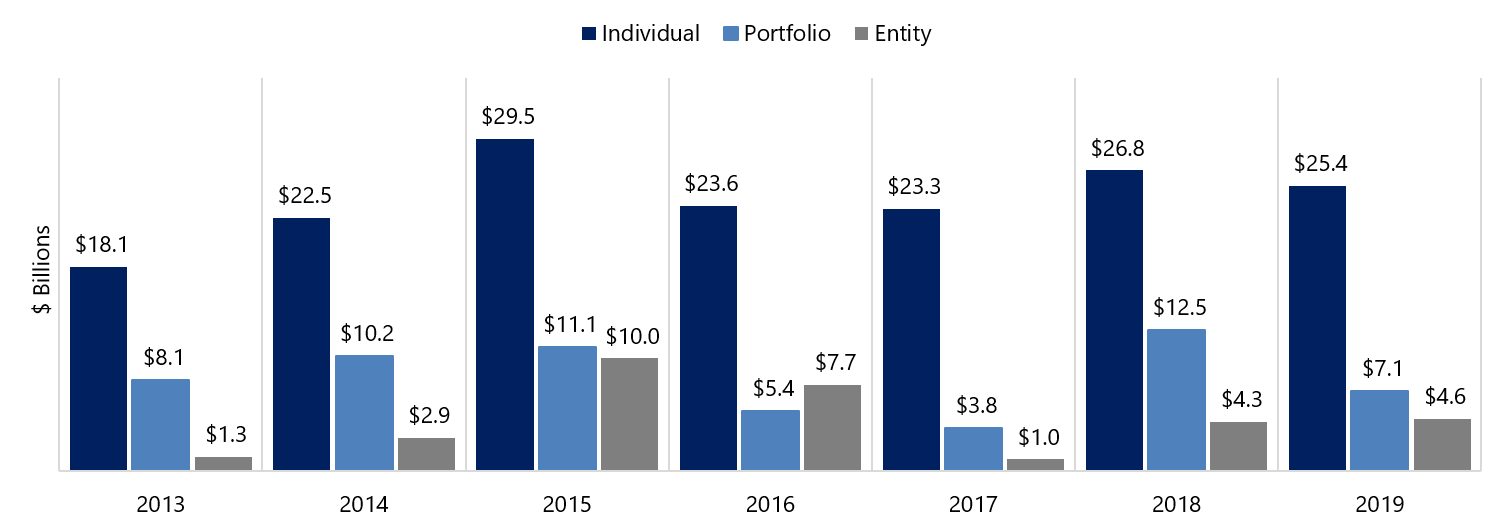

As illustrated below, single-asset property sales volume decreased by a moderate 5.0%, from $26.8 billion in 2018 to $25.4 billion in 2019, while entity sales volume increased by 6%. In contrast, portfolio sales volume decreased by 43%, from $12.5 billion to $7.1 billion. Had Mirae’s $5.8-billion purchase of the Strategic Capital hotel portfolio from Anbang closed in 2019, portfolio volume would have increased by 4%, and total transaction volume would have declined by only 2%. The Mirae deal is reportedly still on track to close in 2020 once some title issues are rectified.

2019 Sales Volume: Individual Asset, Portfolio, and Entity

Source: RCA

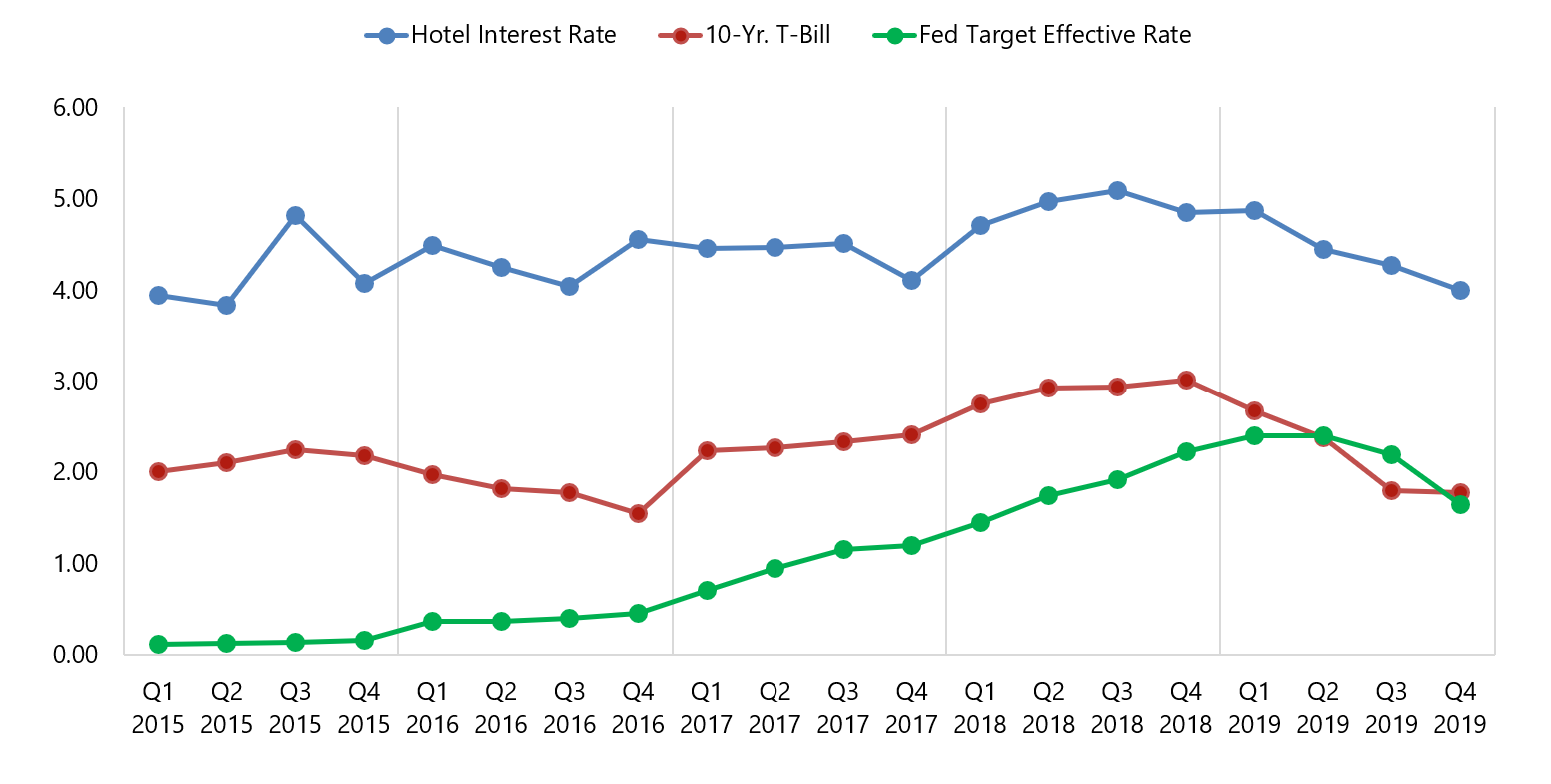

A favorable interest-rate environment helped to sustain transaction activity in a slowing market. After rising moderately in 2018, the ten-year T-bill yield and hotel mortgage interest rates started declining in Q1 2019. While the Federal Reserve’s target rate does not impact long-term mortgage rates, it does provide a more positive environment for economic growth. A year ago, in early 2019, we were facing rising interest rates; the Fed had raised the target rate four times, once in each quarter of 2018, from 1.25–1.5% in Q4 2017 to 2.25–2.5% in Q4 2018. The target rate was sustained at that level until Q3 and Q4 2019 when the Fed decreased the target rate three times in succession, from 2.25–2.5% to 1.50–1.75% as of October 31, 2019. Uncertainty over the U.S./China trade war and a sluggish economic outlook prompted the Fed’s interest-rate reduction in the fall of 2019, shedding some sunshine on the cloudy economic outlook. Hotel investors became more confident about their investment decisions, with both debt and equity capital readily available to fund their acquisitions, capital improvements, and new development. While major factors such as new supply, alternative accommodations, increasing challenges on the distribution front, rising operating costs, and flattening revenue continue to subdue optimism, players in our industry continue to conduct their business strategically. Given the low interest-rate environment and gap between buyer and seller expectations, more owners are likely to refinance in lieu of selling their assets.

Lower Interest Rates Are Helping to Sustain Hotel Investment Activity Source: ACLI and Federal Reserve

As reported by the American Council of Life Insurers (ACLI), hotel interest rates are maintaining an approximately 200 bps spread over the yield on the ten-year T-bill, while the T-bill yield has declined over 100 bps from late 2018; this trend is leading to one of the most favorable lending environments for hotel investors since 2017. Debt priced in the range of 190 to 230 bps over the T-bill yield is obtainable at 60% to 65% LTVs. A T-bill yield of 1.8% (as of the writing of this article) indicates interest rates in the upper 3% to low 4.0% range. Most prognosicators anticipate that the Fed will keep interest rates steady in 2020, and global economic factors indicate that we are more likely to see further declines as opposed to increases into 2021. This outlook provides a favorable environment for hotel investors who are continuing to buy, sell, refinance, and improve their hotel assets.

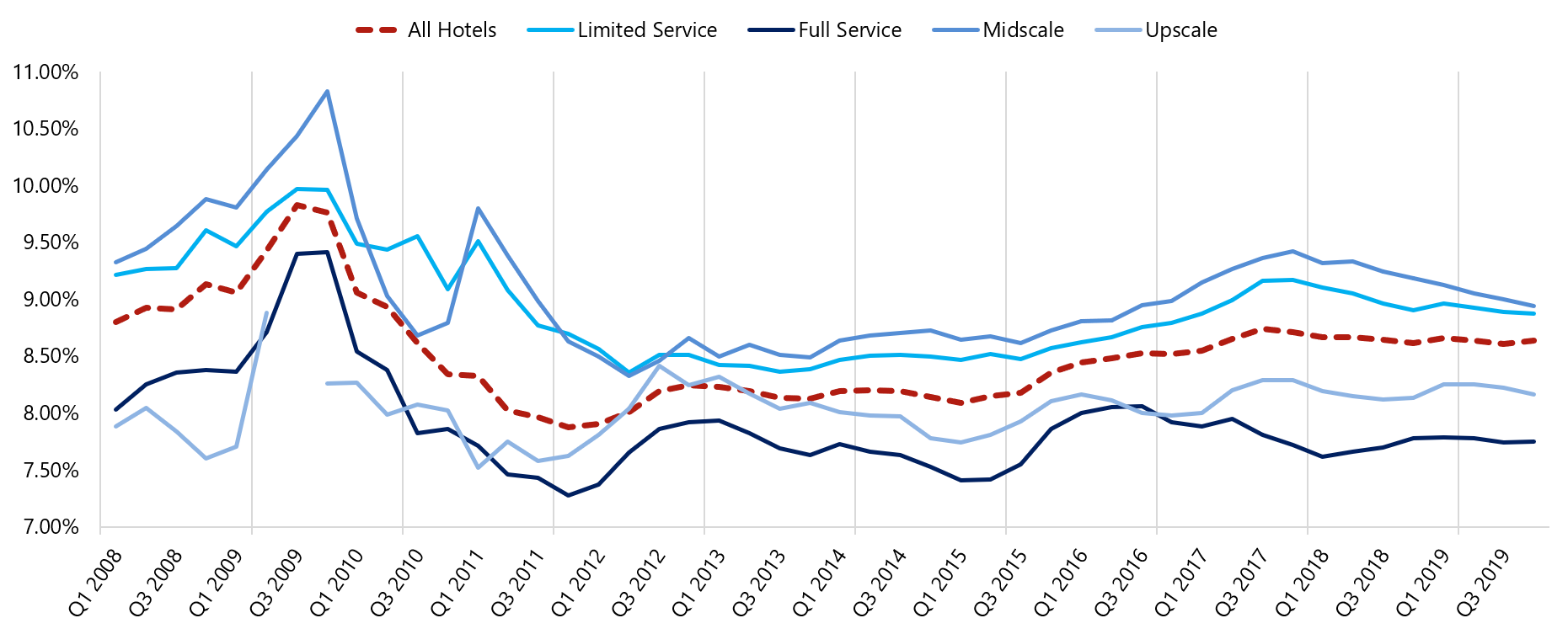

While interest rates have declined, capitalization rates have remained generally steady. After rising from 2016 to late 2017, the RCA data set forth below indicate that capitalization rates for all sales in aggregate remained generally constant through Q3 2019. Cap rates for limited-service, midscale, and upscale hotels appear to have trended modestly downward over the course of the year.

Capitalization Rates Derived from Sales Transactions

Source: RCA

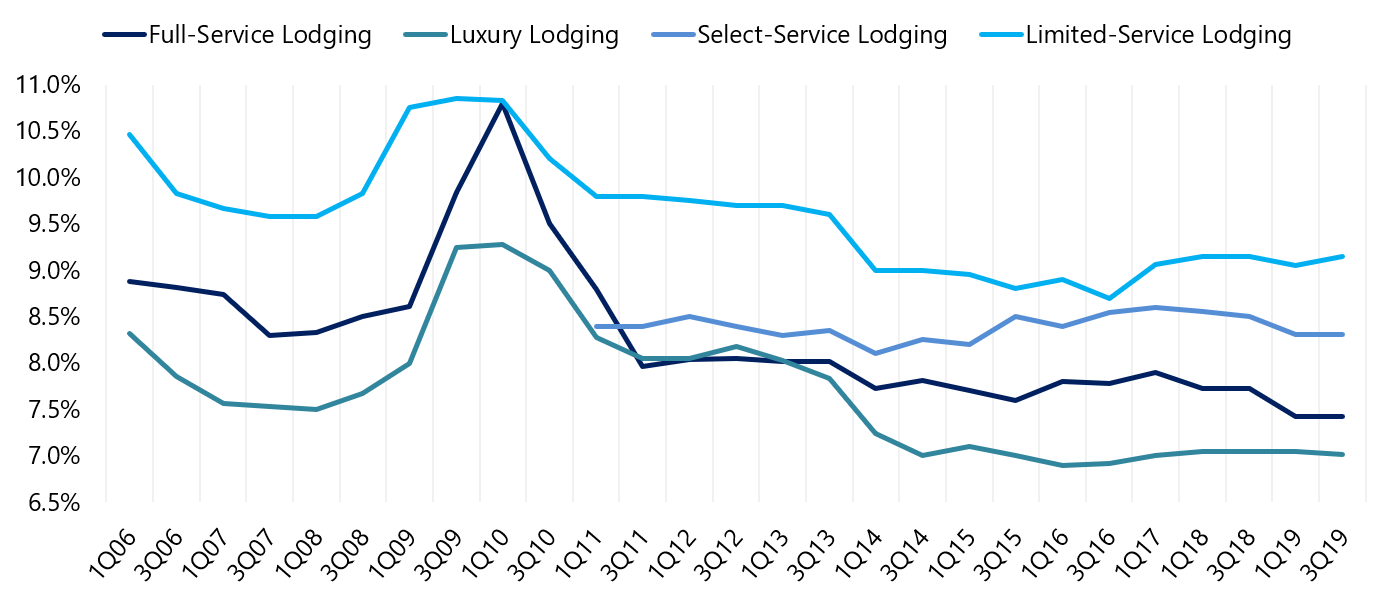

Hotel cap-rate trends reported by the PWC Real Estate Investor Survey, set forth in the following chart, reflect a decline in full-service hotel cap rates and a slight uptick in limited-service hotel cap rates, contrary to the RCA metrics. As the survey data reflect desired rates of return in contrast to rates derived from closed deals, a variance would be expected. With the reduction in interest rates, we would typically expect capitalization rates to decline, while lower future NOI growth would suggest a rise in cap rates; a clear picture of where the trend is headed has not yet emerged.

Capitalization Rate Trends: PWC Real Estate Investor Survey

Source: PWC

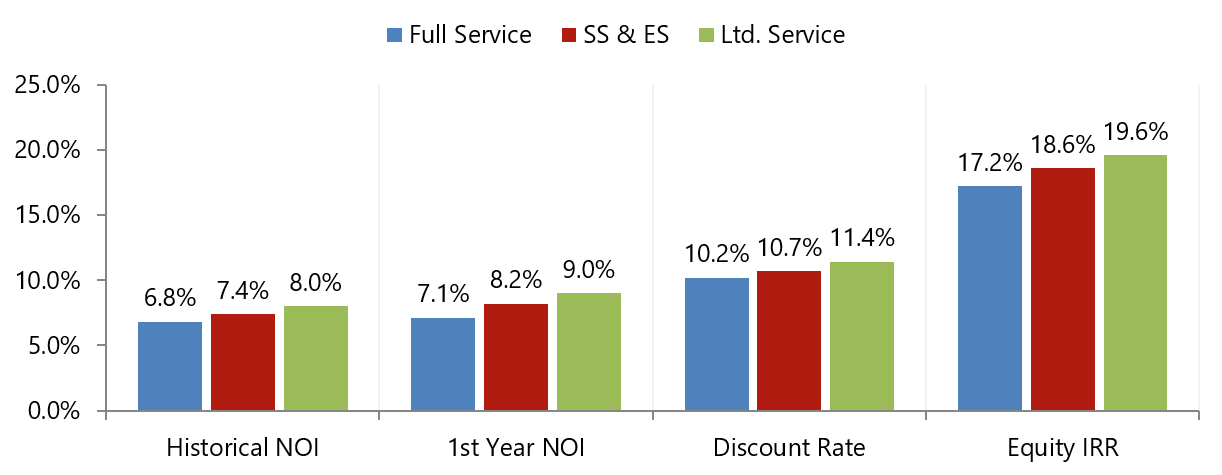

HVS derives capitalization metrics based on hotels appraised at the time of sale. Cap rates are derived based on TTM and projected Year-One NOI, while discount rates and equity internal rates of return (IRRs) are calculated based on the forward-looking projections and debt-service assumptions in the appraisal. The following data reflect the step-up in rates of return from full-service to select-service and limited-service lodging products. Discount rates and equity yield rates remained generally steady in 2019.

Average Rates of Return Derived from 2019 Sales Transactions Source: HVS

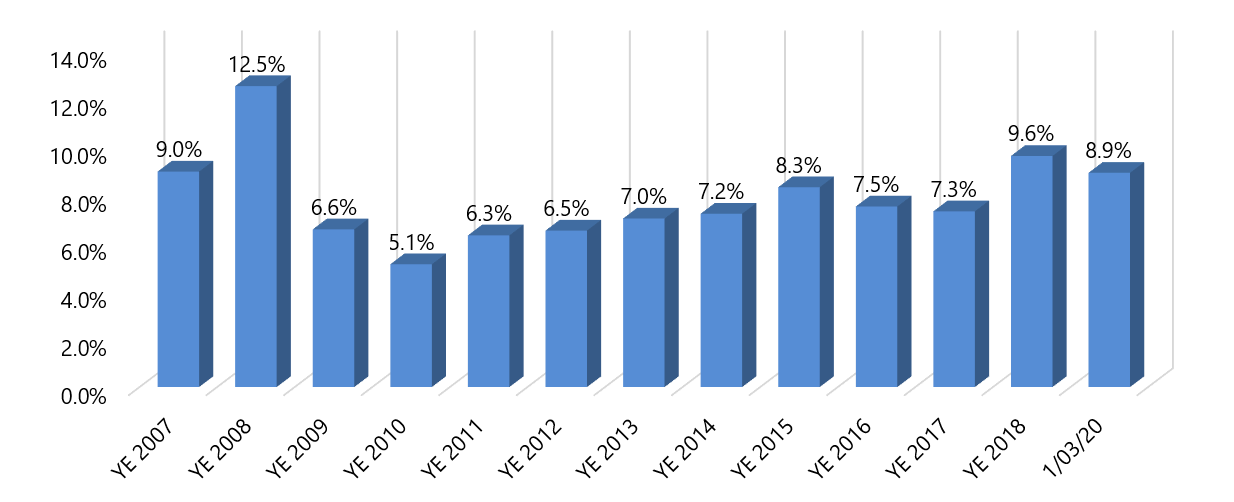

The stock market is a leading indicator and foretells changes in market conditions more quickly than asset sales. The following chart sets forth implied nominal capitalization rates based on the EBITDA generated by the REIT divided by the REIT’s total enterprise value (stock value plus liabilities). Note that EBITDA is reported prior to a reserve for replacement, which we estimate ranges from 80 to 130 bps; thus, the equivalent cap rate for hotel valuation purposes would be about 100 bps less, on average. The stock market performance in 2019 was exceptional; the Dow Jones index experienced a total return of 25.34% for the year, while NAREIT reports that the 18 lodging REITs lagged the overall market, experiencing a total return of 15.65%.

The public markets are continuing to factor in the weaker outlook for hotel performance. As of year-end 2019, publicly traded lodging REITs continued to trade at a 20% to 25% significant discount to underlying asset value, though implied lodging REIT cap rate have moderated slightly since a year ago. As of year-end 2019, they had dipped to 8.9%, but then rose modestly in January 2020.

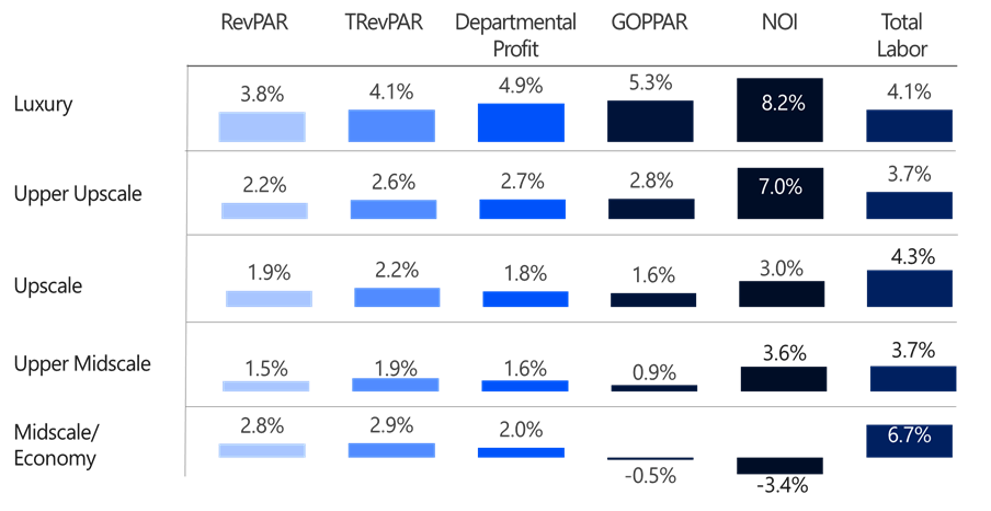

The last piece of the value puzzle is the outlook for hotel performance and income generation. According to STR, more than 40% of the hotels in the U.S. realized a decline in gross operating profit (GOP) in 2018; we note that 2019 data have yet to be reported. These declines reflect the impact of supply outpacing demand growth in some markets, and expenses outpacing revenue, but can also be due to renovation disruption and other temporary factors. The good news is that STR’s “same store” analysis, where the same hotel population is compared year-over-year, indicates that only the midscale/economy class experienced an EBITDA decline in 2018, which compares with declines in both the upscale and upper-midscale classes in 2017. Luxury, upper-upscale, and upscale hotels experienced 7.0%, 3.0%, and 3.6% EBITDA increases, respectively, a strong improvement over the 2.1% increase and 1.7% and 2.8% decreases, respectively, in 2017. Operators seem to be adjusting to the lower RevPAR growth environment through various initiatives, including evaluating their revenue mix, booking channels, staffing levels, property tax assessment, etc. The following chart sets forth a “same store” analysis of EBITDA taken from the STR HOST Almanac 2019 Report, based on 2018 financial performance.

The pressure on EBITDA is primarily being generated by rising labor costs, which are increasing at a rate exceeding revenue gains. Labor expense increases outpaced RevPAR increases in all five hotel categories in 2018. Given changes in labor policy, constraints on immigration, and demographics, this trend is expected to only accelerate in coming years. Hotel operators will be challenged to preserve operating margins. Only time will tell how the hotel industry will respond in an economic downturn when faced with competition from alternative lodging options run by non-professional hosts who can reduce rates without consideration of annual operating budgets, brand constraints, etc. The positive EBITDA gains indicate that operators are learning to live in a revenue-constrained environment.

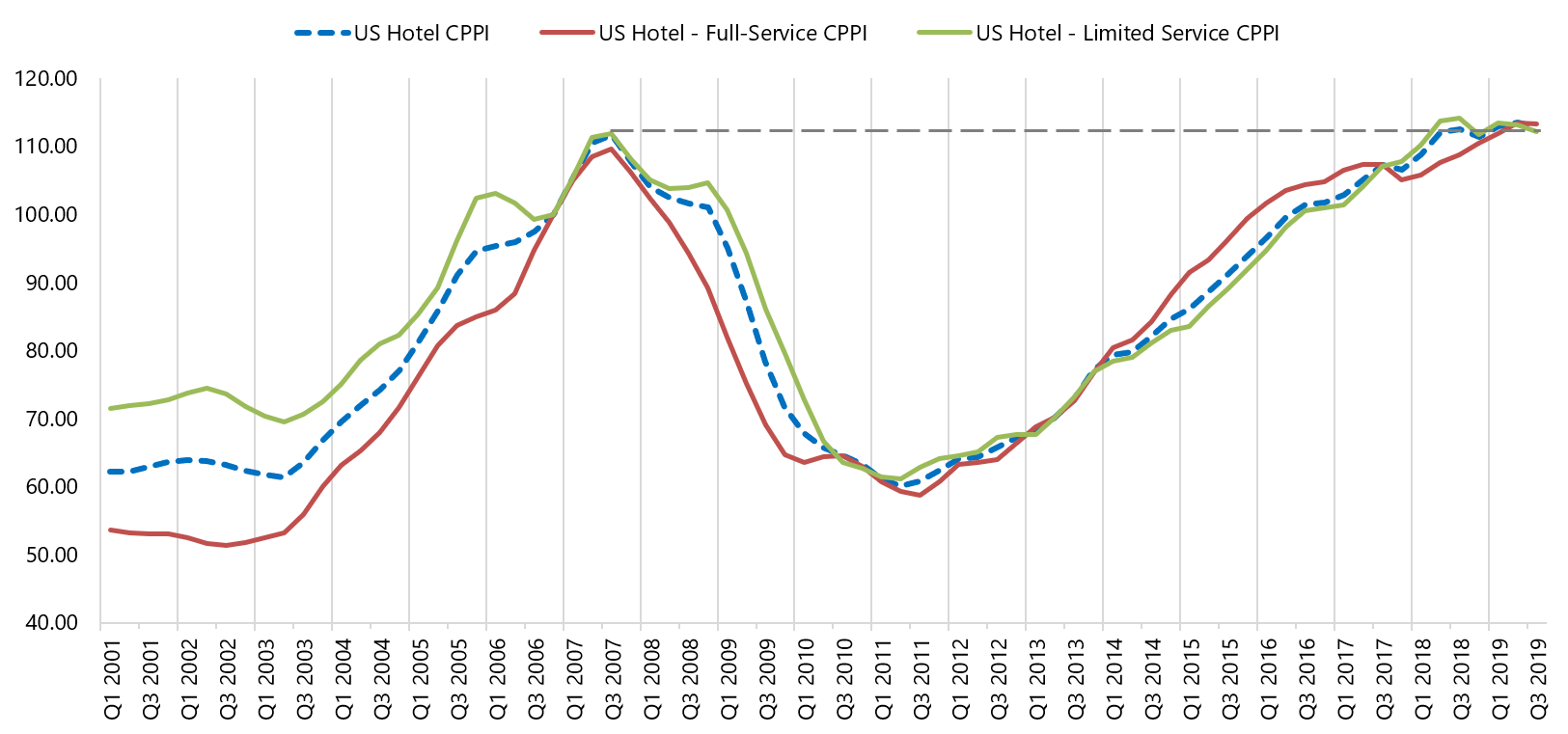

With steady cap rates and modestly increasing/decreasing NOI, the hotel sector is evidencing value stabilization. RCA’s Commercial Property Priced Indices (CPPI) provides insight into hotel value trends since 2002. The RCA CPPI is based on non-inflation adjusted, repeat sales (RS). The RCA CPPI is transaction based and accurately measures real estate price movements using RS regression methodology.

The CPPI for hotel assets over the 18-year period from 2002 through Q3 2019 is graphed below. Hotel values recovered rapidly from the early 2000’s dot.com downturn and then began to decline in early 2008 as we entered the Great Recession. Hotel values declined precipitously from their peak in mid-year 2007 to their trough in mid-year 2012. The value rise in this most recent recovery was at a slower pace than in the 2003–2007 period, and hotel values only reached pre-Great Recession levels in early 2018. The aggregate index masks value trends at the individual asset level. Hotels located in markets with strong economic growth over the last decade have experienced tremendous appreciation, well outperforming the CPPI, while in markets with low barriers to entry hotels constructed in the 1980s and 1990s, now 20 to 40 years old, never fully recovered their pre-recession value.

Since 2018 the index has flattened, reflecting the impact of the factors discussed in this article. Looking forward, we anticipate the index to remain flat or experience a slight decline in 2020, as buyers and sellers increasingly accept that NOI growth will be modest, at best, over the near term. Hotel investment returns are highly dependent on the timing of acquisition and eventual disposition. Whether a hotel’s value has increased or decreased is tied to the point in time when a baseline value was established. Indeed, we are seeing some hotels that sold or were appraised in the 2015–2017 period facing value declines, as NOI growth over the past few years and looking forward is more muted than anticipated at the time of the transaction/valuation. Alternatively, many assets continue to appreciate, driven by targeted operational strategies and capital improvements. However, value declines will continue to surface for some assets in annual financial reporting and in the sale and refinancing process.

RCA CPPIU – Hotel Value Trends

Source: RCA

Outlook for 2020

As we look forward, hotel performance and values will continue to be under pressure in 2020. With RevPAR projected to increase by just over 1% in 2020, many hotels will experience a moderation of NOI and value. While the transaction market is anticipated to remain active, overall volume is likely to decline from 2019 levels, as fewer owners bring their properties to market due to unmet pricing expectations and the looming national election later in the year. Given record low interest rates, refinancing is often the more attractive option. Both debt and equity capital will continue to be widely available for the lodging sector, though underwriting has become more stringent, lowering loan proceeds. While some hotels will experience value declines during this slower period of growth, others will continue to appreciate due to favorable asset/market characteristics and smart ownership and management investment decisions.

[1] The author publishes an article that focuses on hotel capitalization rates in January of each year, which may be accessed here. If you are looking to update any specific data from prior articles not found in this article, please email the author at [email protected].

[2] Implied cap rates based on EBITDA prior to a reserve for replacement; cap rate w/reserve approximately +/-100 bps lower.

1852

About Suzanne Mellen

Suzanne R. Mellen, MAI, CRE, FRICS, ISHC is the Senior Managing Director and Practice Leader of HVS Consulting and Valuation. She has been evaluating hotels and other hospitality real estate assets for 40 years, has authored numerous articles, and is a frequent lecturer and expert witness on the valuation of hotels and related issues. Ms. Mellen has a BS degree in Hotel Administration from Cornell University and holds the following designations: MAI (Appraisal Institute), CRE (Counselor of Real Estate), ISHC (International Society of Hospitality Consultants) and FRICS (Fellow of the Royal Institution of Chartered Surveyors). Contact Suzanne at +1 (415) 268-0351 or [email protected].

As the first news aggregate for the hotel industry, Hotel-Online is the industry’s must-read daily news source for everything hotel curated for busy professionals. Sign up today for industry news delivered to your inbox.