By Jamie Lane and Brett Edgerton

The human tragedy wrought by natural disasters, such as the recent damage done along the Atlantic coast by Hurricane Joaquin, can be tremendous. The death toll within the United States and the Caribbean related to this event is estimated to be in the double digits, and the remediation costs projected to be in the billions. Hotels, as any business in catastrophes, face threats related to such events. The hotel industry is exposed to the physical risk of its property being damaged as well as the economic risk of tourism suffering as people avoid areas disrupted by the disaster. Furthermore, areas most heavily affected face the danger of stigmatization by tourists for some period going forward. At the same time, however, hotels are uniquely positioned to potentially benefit disaster areas because they have the ability to provide shelter for those displaced by the emergency. In this report, we examine the effects of natural disasters looking back at past events to try to gain insight to the impacts catastrophes had on hotel performance to focus on what the hotel industry should expect in the aftermath of Joaquin.

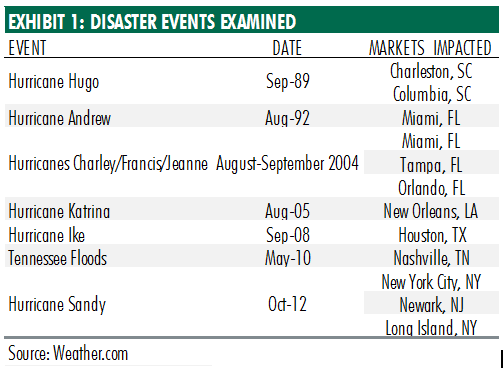

To gauge how natural disasters affect economic activity and hotel markets, we looked back at seven large-scale natural catastrophes that occurred since 1988 to measure the impacts in cities for which we have data.

Economic Impacts

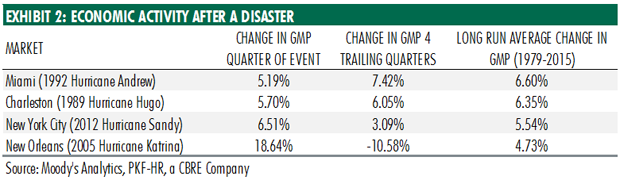

The economic ramifications of disaster events can be calculated by measuring the direct and indirect losses from the catastrophe. Direct physical losses, buildings and infrastructure, are easy to estimate. It is more problematic to estimate indirect losses, such as lost output or wages. Looking at the economic data, GMP (gross metro product), around large disasters reveals little change in the aggregate economic data for each market (see Exhibit 2). The exception is New Orleans where economic output collapsed following Katrina.

From these four events, it can be seen that the economic impacts of natural disasters are not clear cut. This uncertainty is due to the “broken window fallacy” that explains how rebuilding creates economic activity by replacing destroyed property, a suboptimal form of growth. The economic activity occurring to repair a broken window shows up in economic data as increased spending, given that if the window had not broken, no spending to restore it would have occurred. Similarly, rebuilding after a disaster does increase economic output, but can detract from things people might have preferred to buy otherwise, such as leisure travel. Additionally, rebuilding activity does produce the potential long-run benefit of creating enhancements to aging property and infrastructure that must be rebuilt to current standards. While it is not evident from the data examined here, newer more modern properties tend to perform better, serving as a long-term potential benefit of rebuilding efforts.

In general, the economic impact of reconstruction largely depends on two variables: the amount of damage done by a disaster and the amount of public and private expenditures contributed to restoring the economy. Quick and large investments in restoration and reconstruction projects will produce better economic performance. Before rebuilding can occur, however, hotels able to operate after a catastrophe often are the beneficiary of increased demand as displaced people need access to places to stay until they can return home.

Short-Term Impacts

Looking at hotel data from the seven identified historical disasters, we find that demand rose by an average of 3.4 percent in the quarter of an event. In the same quarters, hotel supply typically fell or did not grow in a meaningful way as a result of hotels closing for repairs and construction supplies becoming constrained which limits the feasibility of adding new supply. The markets impacted by the seven disasters in Exhibit 1 had an average decrease in capacity of 1.1 percent in the same quarter as the event. As a result, occupancy levels rise. Rates also tend to increase (on average by 4.8 percent) because of compression in availability. This implies that hotels able to operate after natural disasters are positioned to see boosts in Revenue per Available Room (RevPAR) during the immediate aftermath.

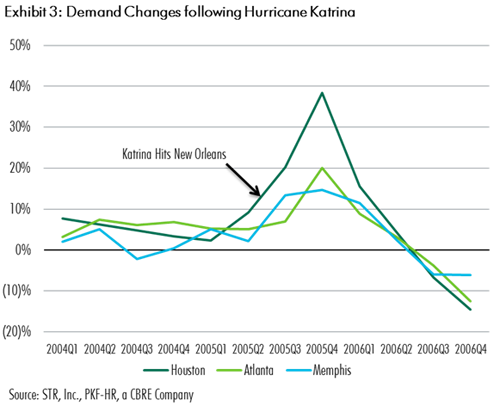

If hotels in the directly affected areas are not able to meet the surge in demand, there is the potential for demand to spill over into other hotel markets with capacity. One source of demand is potentially displaced people from the disaster in need of temporary housing. Another source is changes in tourism flows as people adjust their travel plans to unaffected areas. An extreme example of this behavior occurred in some markets near New Orleans following Hurricane Katrina where there was a year over year increase in demand during the quarters following the storm in certain regional markets such as Houston, Atlanta, and Memphis (see Exhibit 3). Major sources of these demand shifts between cities are meetings and conventions that are forced to move from the impacted city to a nearby location.

Long-Term Impacts

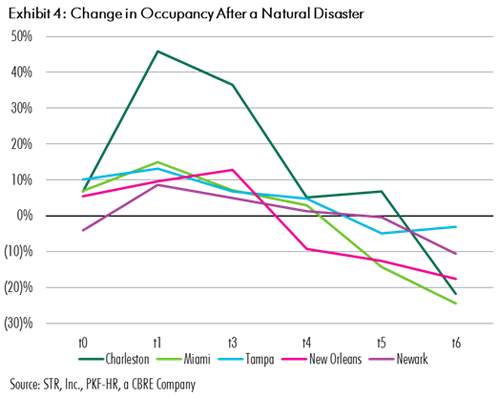

In the four quarters after a natural disaster, supply tends to drop year over year as the most damaged properties take time to repair before returning to the market. On average supply declined by .45 percent in the markets examined here. Demand growth tended to rise quickly following the event, but by the same quarter the subsequent year, demand typically declined as a result of lost tourism and the dissipation in emergency needs. For example, Miami hotels experienced a 14.96 percent jump in demand in the first quarter after Hurricane Andrew (1992 Q4). Miami hotels then experienced a 24.46 percent year over year drop in occupancy during 1993 Q4, despite capacity shrinking by .2 percent over the year. Exhibit 4 shows the general pattern of year over year occupancy changes beginning in the quarter the event occurred (t0) to six quarters after a disaster (t6).

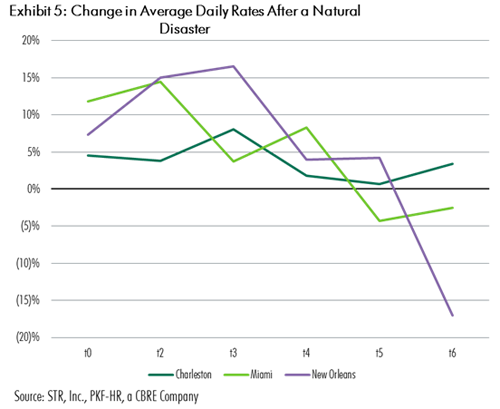

The severity of damage done by an event heavily influences how occupancy performs after a catastrophe. If a large number of hotels are unable to operate, occupancy can potentially surge as the increase in demand has fewer available rooms to occupy. This compression often causes year over year average daily rate (ADR) spikes as shown in Exhibit 5 looking at Charleston after Hurricane Hugo, in Miami after Hurricane Andrew, and in New Orleans after Katrina. ADR behavior displays similar patterns to occupancy. There is an immediate spike in the market as demand surges following the event and then normalizes roughly a year later as economic activity returns to the typical business cycle.

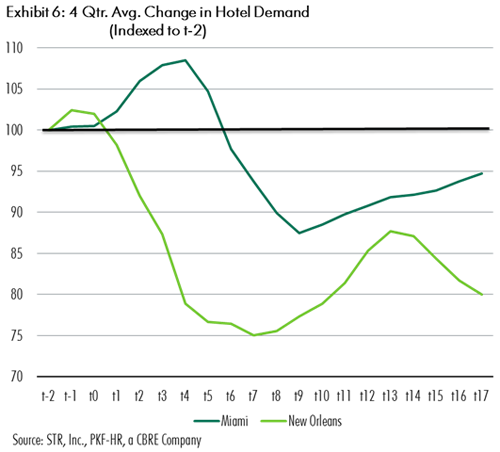

Finally, an important long-term risk to the hotel industry following disasters is stigma related to traveling to a disaster-ravaged area. Stigma means the reduction in lodging demand because of psychological and emotional barriers to travel. Markets may be stigmatized for only a short period, or stigma may impact traveler psyches’ for protracted periods of time. Exhibit 6 shows sustained lower levels of demand following two of the worst natural disasters, Hurricanes Andrew and Katrina. In both cases, demand fell below previous levels for extended periods following the hurricanes. While some of this effect may be a result of economics and/or reduced lodging capacity, it is also likely that stigma negatively impacted people’s choices to travel to both cities.

Impacts from Joaquin

Hurricane Joaquin has the potential to influence current and future demand, supply, and revenue in the coastal Carolinas. Regarding our Hotel Horizons® forecasts, the principal effects should be in Charleston and Columbia, South Carolina where the heaviest damage was seen. Based on our analysis of similar past events, we will adjust our econometric forecasts as required to capture any short-term changes and carefully monitor the long term potential risks associated with stigma.

As a business, what is frequently overlooked in the immediate turmoil is the need to secure important data and documents. This information is especially vital for those owners that wish to recover lost business income from insurance companies. While the actual filing of claims and negotiations may not occur until a year or two after the horrific event, several pieces of data and documents need to be gathered in the short term to achieve a favorable settlement later on.

After working with our clients to recoup business interruption benefits from insurance companies, we found certain data and documents to be extremely useful in our calculations of lost revenues and profits. In addition, using models relying on historic data and forecasts, estimates can be made for lost room nights, revenue, and net income.

Conclusion

The impact any natural disaster has on the hotel industry is difficult to predict precisely given the numerous dynamics that influence performance following such events. The severity of damage caused by the disaster is a crucial factor. Hurricane Katrina, for example, was so destructive that the New Orleans economy and hotel industry did not recover within six quarters of the storm. Furthermore, the economic conditions in an area also shape the impact. Houston hotels experienced drastic demand declines in the quarters after Hurricane Ivan because the storm hit just before the 2008 financial crisis and recession occurred. Finally, the amount of public and private reconstruction investment that occurs will also determine the long-term impacts of any disaster.

It is challenging to assume any catastrophic event will follow a set pattern because the events are all unique. In general however, hotels tend to benefit from a surge in demand following a disaster that boosts occupancy levels and rates for several quarters thereafter until the economy of the affected area returns to normal. Some disasters, however, have the potential to shift the underlying factors that drive the hotel economy by changing consumer’s desire to travel to a traumatized location. Ultimately, the impact hotels suffer as a result of Hurricane Joaquin will depend on the total amount of damage and rebuilding that occurs, the economic conditions in the Coastal Carolinas, as well as any long-term stigma that may develop regarding tourism in the area.

To learn more about CBRE Research, or to access additional research reports, please visit the Global Research Gateway at www.cbre.com/researchgateway. Additional U.S. research produced by CBRE Research can be found at www.cbre.us/research.