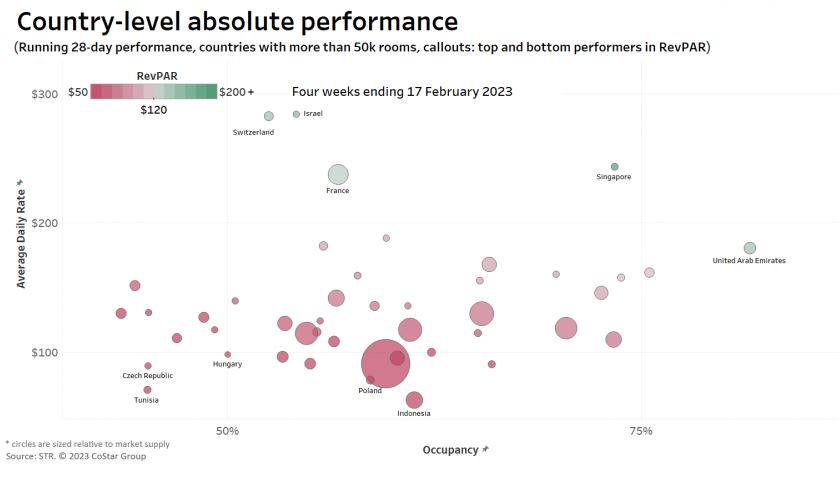

STR’s global “bubble chart” updated through 17 February 2023 showed generally strong performance to kickstart the year. Among all countries with room supply of more than 50,000 rooms, Israel, Switzerland, Singapore, France and the United Arab Emirates led in revenue per available room (RevPAR) on an actual basis. If you recall, Israel, Switzerland and Singapore were among the top five in RevPAR during 2022 and that strength has continued early 2023.

On the other hand, Tunisia, Hungary, Poland, Czech Republic, and Indonesia were among the bottom five performers in RevPAR. Of note, this was the first time in the last seven of these global updates in which countries from the Asia Pacific region were not the majority of the bottom performers.

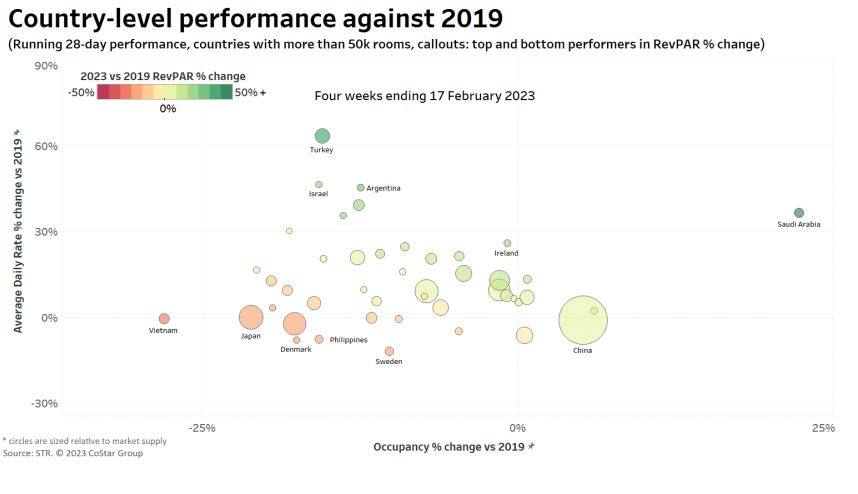

Overall, 29 of the 48 countries with hotel supply greater than 50,000 rooms recorded growth in RevPAR versus the matching 28-day period in 2019. The total was less than half during our end-of-year review for 2022, which again signals a strong start to 2023. The growth in RevPAR was still predominantly driven by room rates, with only seven countries exceeding 2019 occupancy versus 37 surpassing their pre-pandemic ADR. Saudi Arabia grew RevPAR by a staggering 67% as the country embraced pent-up demand from religious tourism where the authority permits more visitors to perform Umrah in the region. Also important, China was among the countries with gains in RevPAR for the first time since 2022, as the country celebrated its first restriction free Chinese New Year in the last three years.

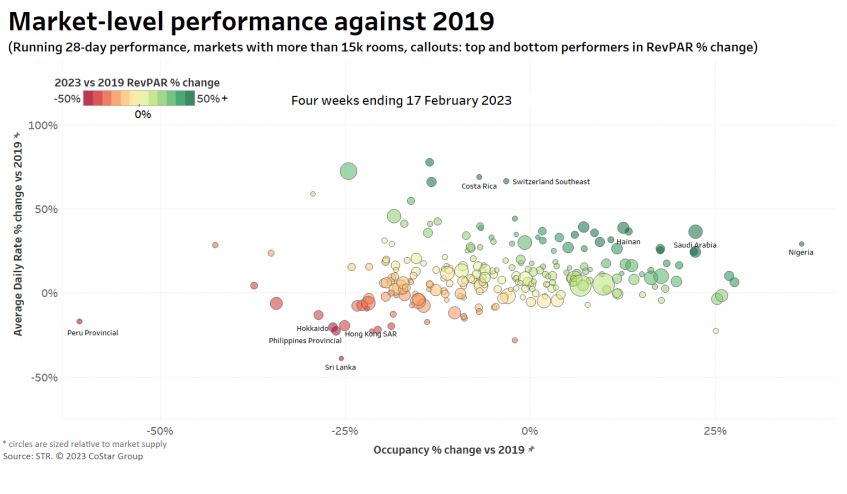

Nearly two-thirds of markets posted RevPAR higher than 2019 to begin the year of 2023. Nigeria is the first African market to be highlighted in this monthly analysis, which took a spot in the top five RevPAR growth markets. Hainan, a popular domestic beach resort destination in China, was also among the top five performers for the first time since July 2022.

The full return of Chinese tourists has yet to be seen around the region, however. Hong Kong, one of the most popular Chinese outbound tourist markets, saw its RevPAR remain down 40% versus the comparable in 2019. Hokkaido, a popular ski resort during the Chinese New Year holiday, reported RevPAR that was down roughly 42%.

Overall, global markets were able to carry the recovery momentum as only 8% of markets saw their occupancy level remain under 75% of 2019 comparables—that percentage was 18% at the end of year of 2022. More improvements are to be expected as the Asia Pacific region returns to normalcy.