GCC countries have supported and grown inbound tourism in the last 15-20 years. The GCC region continues to drive growth and investment opportunities and HVS remain confident that accommodated room night demand will grow despite the aggressive development pipeline.

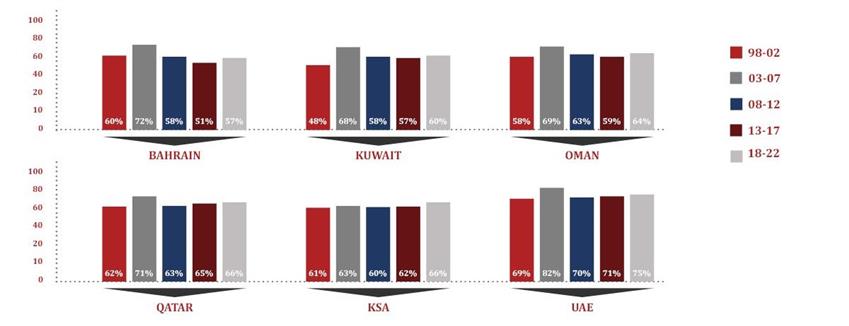

GCC Countrywide Occupancy

Historic (1998-2017) and Forecast – 5 Year Average

5 Year Average GCC Countrywide Occupancy with HVS Forecast

Source: HVS Research

Source: HVS Research

A number of demand generators will induce additional room nights in each of the GCC countries over the next 5 and 10 years. Specifically, we forecast occupancy in Qatar to average 66% on account of the ongoing developments and the 2022 World Cup. Major projects and government initiatives in KSA will allow the country to achieve 66% countrywide occupancy in the next couple of years. UAE specifically continues to introduce new projects and Expo 2020 will support growth in occupancy to average of 75% for the next five years. Bahrain, Oman and Kuwait will also register a rise in demand attributed to the government tourism initiatives and overall policy reforms to support international investments and tourism growth.

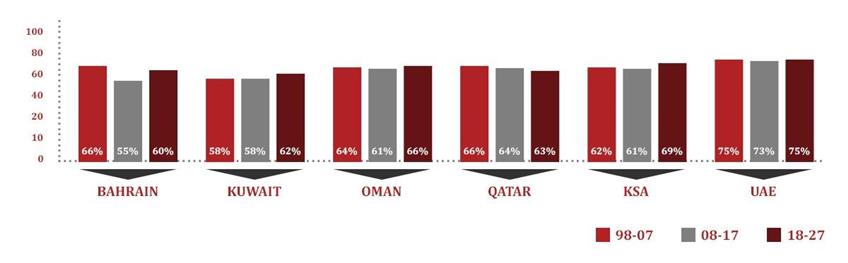

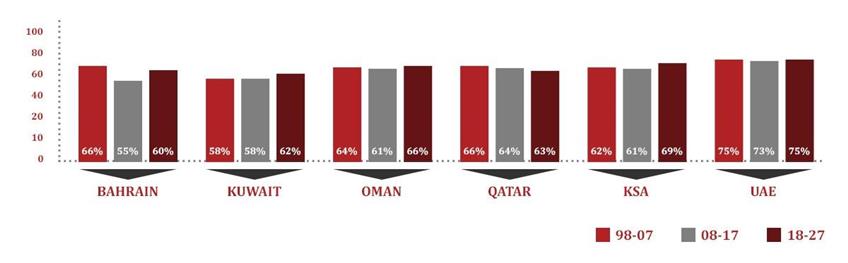

Historic (1998-2017) and Forecast – 10 Year Average

10 Year Average GCC Countrywide Occupancy with HVS Forecast

Source: HVS Research

Source: HVS Research

Marketwide Occupancy can be misleading when not considered in the context of supply and demand dynamics. All GCC countries have registered double digit growth in accommodated roomnight demand in the last 20 years, further illustrating the growth of the tourism sector in the region.

Historical occupancy in the GCC countries in the last 10 and 20 years averaged approximately 62% and 64% respectively, UAE consistently outperforming the GCC average hotel occupancy. HVS forecast hotel occupancy over the next 10 years: KSA is expected to register the largest growth in occupancy levels (8pp), followed by Oman and Bahrain (5pp). Despite the increase in visitation to the UAE, the strong supply pipeline will result in constrained occupancy of 75%.

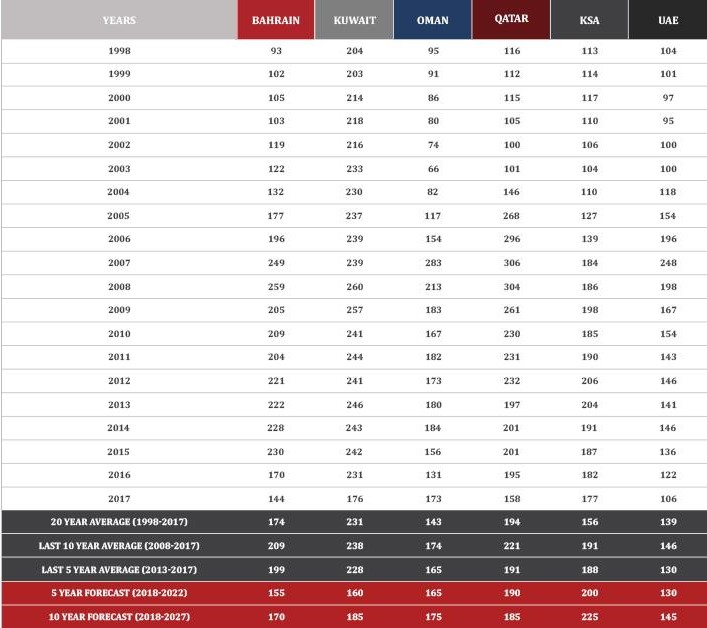

GCC Countrywide Average Daily Rate

Historic (1998-2017) and Forecast – 5 Year Average

5 Year Average GCC Countrywide Average Daily Rate USD – HVS Forecast

Source: HVS Research

Source: HVS Research

A review of yearly marketwide average rates across GCC countries since 1998 indicate a peak in the years 2006 to 2008, after which average rates have started to normalise and in certain cities decline.

The entrance of additional hotel rooms to the GCC market will continue to impact the achievable average daily rate, despite the potential demand induced by new developments and government initiatives. HVS forecast countrywide ADR in UAE, Oman and Qatar to remain stagnant.

KSA is likely to benefit from the recent changes in tourism government policies; average rates across KSA is forecasted to grow to USD200.

Bahrain and Kuwait will both register further drops in market wide average rate, as a result of increased competition and the phase out of the hotel rate cartel agreement effectuated by the hotel owners’ association.

Historic (1998-2017) and Forecast – 10 Year Average

10 Year Average GCC Countrywide Average Daily Rate USD – HVS Forecast

Source: HVS Research

Source: HVS Research

Historical average daily rates in the GCC countries in the last 10 years averaged approximately USD197, an increase of 32% over the period 1998-2007, with Bahrain, Kuwait and Qatar overpenetrating the GCC market wide average rate.

HVS forecast KSA to achieve an ADR of USD225 over the next ten years while all other GCC countries are likely to experience a stagnation or decline in average daily rates as a result of aggressive development pipeline and increased competition.

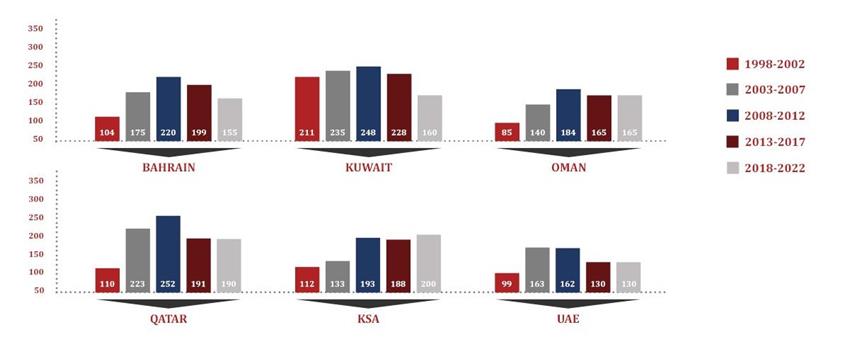

GCC Countrywide Revenue per Available Room

Historic (1998-2017) and Forecast – 5- and 10-Year Average

GCC Countrywide Revenue per Available Room USD – HVS Forecast

Source: HVS Research

Source: HVS Research

Marketwide Revenue per Available room in the GCC dropped by 15% in the recent five years, with the exception of KSA which has remained resilient at USD116. The declining RevPAR performance is expected to continue in Bahrain and Kuwait. HVS forecasts a RevPAR increase in KSA, UAE, Oman in the next five and ten years, attributable to increased occupancy and roomnights driven by new developments.

5 Year (2018-2022) and 10 Year (2018-2027), GCC Countrywide Revenue per Available Room USD – HVS Forecast

Source: HVS Research

Source: HVS Research

GCC Countrywide Performance Indicators in Summary

Occupancy

Historic GCC Countrywide Occupancy% 1998-2027 – HVS Forecast

Source: HVS Research

Source: HVS Research

Average Daily Rate

Historic GCC Countrywide Average Daily Rate USD 1998-2017 – HVS Forecast

Source: HVS Research

Source: HVS Research

Revenue per Available Room

Historic GCC Countrywide Revenue per Available Room USD 1998-2017 – HVS Forecast

Source: HVS Research

Source: HVS Research